{"title":"ResNLS:改进的股票价格预测模型","authors":"Yuanzhe Jia, Ali Anaissi, Basem Suleiman","doi":"10.1111/coin.12608","DOIUrl":null,"url":null,"abstract":"<p>Stock prices forecasting has always been a challenging task. Although many research projects adopt machine learning and deep learning algorithms to address the problem, few of them pay attention to the varying degrees of dependencies between stock prices. In this paper we introduce a hybrid model that improves stock price prediction by emphasizing the dependencies between adjacent stock prices. The proposed model, ResNLS, is mainly composed of two neural architectures, ResNet and LSTM. ResNet serves as a feature extractor to identify dependencies between stock prices across time windows, while LSTM analyses the initial time-series data with the combination of dependencies which considered as residuals. In predicting the SSE Composite Index, our experiment reveals that when the closing price data for the previous five consecutive trading days is used as the input, the performance of the model (ResNLS-5) is optimal compared to those with other inputs. Furthermore, ResNLS-5 outperforms vanilla CNN, RNN, LSTM, and BiLSTM models in terms of prediction accuracy. It also demonstrates at least a 20% improvement over the current state-of-the-art baselines. To verify whether ResNLS-5 can help clients effectively avoid risks and earn profits in the stock market, we construct a quantitative trading framework for back testing. The experimental results show that the trading strategy based on predictions from ResNLS-5 can successfully mitigate losses during declining stock prices and generate profits in the periods of rising stock prices.</p>","PeriodicalId":55228,"journal":{"name":"Computational Intelligence","volume":null,"pages":null},"PeriodicalIF":1.8000,"publicationDate":"2023-11-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/coin.12608","citationCount":"0","resultStr":"{\"title\":\"ResNLS: An improved model for stock price forecasting\",\"authors\":\"Yuanzhe Jia, Ali Anaissi, Basem Suleiman\",\"doi\":\"10.1111/coin.12608\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Stock prices forecasting has always been a challenging task. Although many research projects adopt machine learning and deep learning algorithms to address the problem, few of them pay attention to the varying degrees of dependencies between stock prices. In this paper we introduce a hybrid model that improves stock price prediction by emphasizing the dependencies between adjacent stock prices. The proposed model, ResNLS, is mainly composed of two neural architectures, ResNet and LSTM. ResNet serves as a feature extractor to identify dependencies between stock prices across time windows, while LSTM analyses the initial time-series data with the combination of dependencies which considered as residuals. In predicting the SSE Composite Index, our experiment reveals that when the closing price data for the previous five consecutive trading days is used as the input, the performance of the model (ResNLS-5) is optimal compared to those with other inputs. Furthermore, ResNLS-5 outperforms vanilla CNN, RNN, LSTM, and BiLSTM models in terms of prediction accuracy. It also demonstrates at least a 20% improvement over the current state-of-the-art baselines. To verify whether ResNLS-5 can help clients effectively avoid risks and earn profits in the stock market, we construct a quantitative trading framework for back testing. The experimental results show that the trading strategy based on predictions from ResNLS-5 can successfully mitigate losses during declining stock prices and generate profits in the periods of rising stock prices.</p>\",\"PeriodicalId\":55228,\"journal\":{\"name\":\"Computational Intelligence\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-11-12\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/coin.12608\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Computational Intelligence\",\"FirstCategoryId\":\"94\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/coin.12608\",\"RegionNum\":4,\"RegionCategory\":\"计算机科学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Computational Intelligence","FirstCategoryId":"94","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/coin.12608","RegionNum":4,"RegionCategory":"计算机科学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"COMPUTER SCIENCE, ARTIFICIAL INTELLIGENCE","Score":null,"Total":0}

ResNLS: An improved model for stock price forecasting

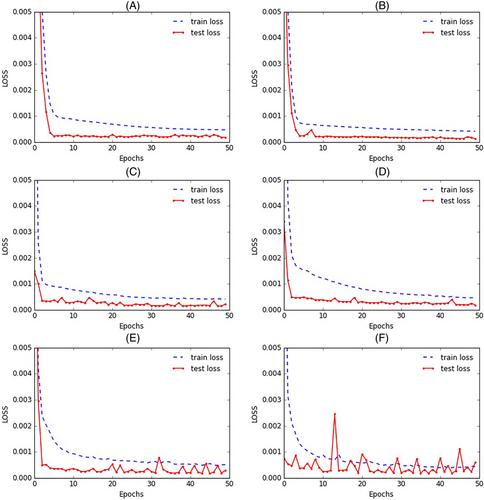

Stock prices forecasting has always been a challenging task. Although many research projects adopt machine learning and deep learning algorithms to address the problem, few of them pay attention to the varying degrees of dependencies between stock prices. In this paper we introduce a hybrid model that improves stock price prediction by emphasizing the dependencies between adjacent stock prices. The proposed model, ResNLS, is mainly composed of two neural architectures, ResNet and LSTM. ResNet serves as a feature extractor to identify dependencies between stock prices across time windows, while LSTM analyses the initial time-series data with the combination of dependencies which considered as residuals. In predicting the SSE Composite Index, our experiment reveals that when the closing price data for the previous five consecutive trading days is used as the input, the performance of the model (ResNLS-5) is optimal compared to those with other inputs. Furthermore, ResNLS-5 outperforms vanilla CNN, RNN, LSTM, and BiLSTM models in terms of prediction accuracy. It also demonstrates at least a 20% improvement over the current state-of-the-art baselines. To verify whether ResNLS-5 can help clients effectively avoid risks and earn profits in the stock market, we construct a quantitative trading framework for back testing. The experimental results show that the trading strategy based on predictions from ResNLS-5 can successfully mitigate losses during declining stock prices and generate profits in the periods of rising stock prices.

期刊介绍:

This leading international journal promotes and stimulates research in the field of artificial intelligence (AI). Covering a wide range of issues - from the tools and languages of AI to its philosophical implications - Computational Intelligence provides a vigorous forum for the publication of both experimental and theoretical research, as well as surveys and impact studies. The journal is designed to meet the needs of a wide range of AI workers in academic and industrial research.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: