{"title":"新冠肺炎疫情与股市表现:基于澳大利亚的实证分析*","authors":"Markus Brueckner, Joaquin Vespignani","doi":"10.1111/1759-3441.12318","DOIUrl":null,"url":null,"abstract":"<p>Using daily data, we estimate a vector autoregression model to characterise the dynamic relationship between COVID-19 infections in Australia and the performance of the Australian stock market, specifically the ASX-200. Impulse response functions show that COVID-19 infections in Australia have a significant positive effect on the performance of the stock market: a one standard deviation increase in new registered cases of COVID-19 infections in Australia increases the daily growth rate of the ASX-200 by around half a percentage point. This result is robust to alternative lag selections of the VAR model as suggested by alternative information criteria, including in the model control variables for stock market volatility, that is the ASX-200 VIX; the USD-AUD exchange rate and the international oil price; news by the World Health Organization regarding a COVID-19 pandemic and public health emergency; and the government-imposed shutdown of parts of the Australian economy. We also present estimates of the dynamic relationship between the daily growth rate of the Dow Jones and daily new cases of COVID-19 infections in the United States. The US data show, similar to the Australian data, that there is a significant positive effect of COVID-19 infections on the performance of the stock market.</p>","PeriodicalId":45208,"journal":{"name":"Economic Papers","volume":"40 3","pages":"173-193"},"PeriodicalIF":0.9000,"publicationDate":"2021-06-03","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://sci-hub-pdf.com/10.1111/1759-3441.12318","citationCount":"21","resultStr":"{\"title\":\"COVID-19 Infections and the Performance of the Stock Market: An Empirical Analysis for Australia*\",\"authors\":\"Markus Brueckner, Joaquin Vespignani\",\"doi\":\"10.1111/1759-3441.12318\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Using daily data, we estimate a vector autoregression model to characterise the dynamic relationship between COVID-19 infections in Australia and the performance of the Australian stock market, specifically the ASX-200. Impulse response functions show that COVID-19 infections in Australia have a significant positive effect on the performance of the stock market: a one standard deviation increase in new registered cases of COVID-19 infections in Australia increases the daily growth rate of the ASX-200 by around half a percentage point. This result is robust to alternative lag selections of the VAR model as suggested by alternative information criteria, including in the model control variables for stock market volatility, that is the ASX-200 VIX; the USD-AUD exchange rate and the international oil price; news by the World Health Organization regarding a COVID-19 pandemic and public health emergency; and the government-imposed shutdown of parts of the Australian economy. We also present estimates of the dynamic relationship between the daily growth rate of the Dow Jones and daily new cases of COVID-19 infections in the United States. The US data show, similar to the Australian data, that there is a significant positive effect of COVID-19 infections on the performance of the stock market.</p>\",\"PeriodicalId\":45208,\"journal\":{\"name\":\"Economic Papers\",\"volume\":\"40 3\",\"pages\":\"173-193\"},\"PeriodicalIF\":0.9000,\"publicationDate\":\"2021-06-03\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://sci-hub-pdf.com/10.1111/1759-3441.12318\",\"citationCount\":\"21\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Economic Papers\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1759-3441.12318\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Economic Papers","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1759-3441.12318","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

COVID-19 Infections and the Performance of the Stock Market: An Empirical Analysis for Australia*

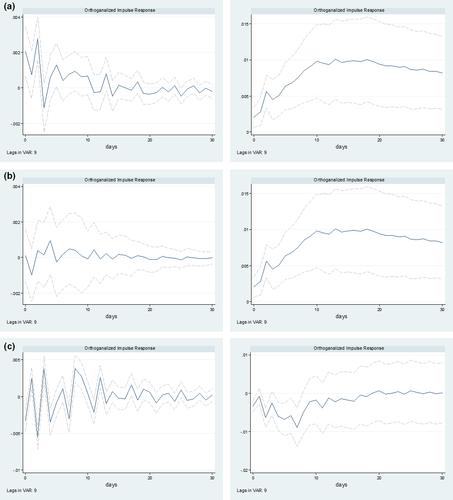

Using daily data, we estimate a vector autoregression model to characterise the dynamic relationship between COVID-19 infections in Australia and the performance of the Australian stock market, specifically the ASX-200. Impulse response functions show that COVID-19 infections in Australia have a significant positive effect on the performance of the stock market: a one standard deviation increase in new registered cases of COVID-19 infections in Australia increases the daily growth rate of the ASX-200 by around half a percentage point. This result is robust to alternative lag selections of the VAR model as suggested by alternative information criteria, including in the model control variables for stock market volatility, that is the ASX-200 VIX; the USD-AUD exchange rate and the international oil price; news by the World Health Organization regarding a COVID-19 pandemic and public health emergency; and the government-imposed shutdown of parts of the Australian economy. We also present estimates of the dynamic relationship between the daily growth rate of the Dow Jones and daily new cases of COVID-19 infections in the United States. The US data show, similar to the Australian data, that there is a significant positive effect of COVID-19 infections on the performance of the stock market.

期刊介绍:

Economic Papers is one of two journals published by the Economics Society of Australia. The journal features a balance of high quality research in applied economics and economic policy analysis which distinguishes it from other Australian journals. The intended audience is the broad range of economists working in business, government and academic communities within Australia and internationally who are interested in economic issues related to Australia and the Asia-Pacific region. Contributions are sought from economists working in these areas and should be written to be accessible to a wide section of our readership. All contributions are refereed.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: