Laure Latruffe, Yann Desjeux, Geoffroy Enjolras, Philippe Jeanneaux

{"title":"Methods for Farm Valuation\n Les méthodes d’évaluation des exploitations agricoles\n Methoden zur Bewertung von landwirtschaftlichen Betrieben","authors":"Laure Latruffe, Yann Desjeux, Geoffroy Enjolras, Philippe Jeanneaux","doi":"10.1111/1746-692X.12392","DOIUrl":null,"url":null,"abstract":"<p>Valuation of a farm at current market value is a crucial part of the process of farm transfer, be it between family members through inheritance or on the open market between buyers and sellers. This article explains the methods available to and used by professionals in France to value farms, and presents results of an application of the methods on bookkeeping data for French representative commercial farms.</p><p>The literature is rich on business valuation methods but less so in the farming context. Some assets are often very specific (farm buildings, livestock, agricultural land) and the activities of farms are by nature diverse and risky, making it difficult to standardise their valuation. There are two broad categories of methods. Economic methods are based on cash flows and profitability generated by the assets and include the <b>fundamental</b> and <b>financial methods.</b> The fundamental (or discounted cash-flows or long-term returns or capitalisation) method consists of valuing the farm as an industrial project that will generate cash flows in the future, over a chosen time horizon, for example the duration of a long-term rental agreement (nine years in France). The farm value is thus the sum of the future net cash flows discounted at an appropriate rate. The financial (or profitability) method is based on the estimation of the farm investors’ potential remuneration, which can be approximated by the farm net profit (farm income from which the farm manager's labour remuneration has been subtracted).</p><p>The second category of methods relies on the separately-valued assets mainly with the <b>patrimonial method</b> (or liquidation and accounting valuation method). Each tangible asset is estimated separately, with the current market value or with the book value of assets available in the balance sheet. While the fundamental method is generally preferred by buyers (that is to say, future farmers) and banks, sellers favour the patrimonial method as it generates high values. In practice both sets of methods are often used in combination.</p><p>In 2021 an online survey was conducted of 67 land experts and farm accountants in France who regularly estimate farm values for farmers (both sellers or buyers) (Enjolras <i>et al</i>., <span>2023</span>). As shown in Figure 1, the highest share of experts (56 per cent) used the patrimonial method, although the fundamental and financial methods together account for a comparable share of experts (53 per cent). The survey also highlighted the difficult conciliation of perspectives between sellers and buyers and the need to consider intangible factors, as seen in Figure 2.</p><p>The different methods were applied to the 2017 and 2018 French Farm Accountancy Data Network (FADN) bookkeeping data (Jeanneaux <i>et al</i>., <span>2022</span>). Figure 3 shows that wine-growing farms have the highest values on average. Pig and beef cattle farms have high average patrimonial values, reflecting their high capital intensity. However, beef cattle farms have the lowest average values calculated with fundamental and financial methods, suggesting less favourable market conditions for these farms. Further research is needed to empirically assess the drivers of values, and in particular the part of the value that is due to intangible assets.</p>","PeriodicalId":44823,"journal":{"name":"EuroChoices","volume":"22 2","pages":"36-37"},"PeriodicalIF":3.1000,"publicationDate":"2023-06-15","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1746-692X.12392","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"EuroChoices","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1746-692X.12392","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"AGRICULTURAL ECONOMICS & POLICY","Score":null,"Total":0}

引用次数: 0

Abstract

Valuation of a farm at current market value is a crucial part of the process of farm transfer, be it between family members through inheritance or on the open market between buyers and sellers. This article explains the methods available to and used by professionals in France to value farms, and presents results of an application of the methods on bookkeeping data for French representative commercial farms.

The literature is rich on business valuation methods but less so in the farming context. Some assets are often very specific (farm buildings, livestock, agricultural land) and the activities of farms are by nature diverse and risky, making it difficult to standardise their valuation. There are two broad categories of methods. Economic methods are based on cash flows and profitability generated by the assets and include the fundamental and financial methods. The fundamental (or discounted cash-flows or long-term returns or capitalisation) method consists of valuing the farm as an industrial project that will generate cash flows in the future, over a chosen time horizon, for example the duration of a long-term rental agreement (nine years in France). The farm value is thus the sum of the future net cash flows discounted at an appropriate rate. The financial (or profitability) method is based on the estimation of the farm investors’ potential remuneration, which can be approximated by the farm net profit (farm income from which the farm manager's labour remuneration has been subtracted).

The second category of methods relies on the separately-valued assets mainly with the patrimonial method (or liquidation and accounting valuation method). Each tangible asset is estimated separately, with the current market value or with the book value of assets available in the balance sheet. While the fundamental method is generally preferred by buyers (that is to say, future farmers) and banks, sellers favour the patrimonial method as it generates high values. In practice both sets of methods are often used in combination.

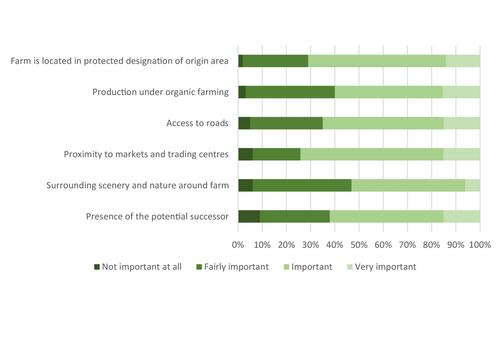

In 2021 an online survey was conducted of 67 land experts and farm accountants in France who regularly estimate farm values for farmers (both sellers or buyers) (Enjolras et al., 2023). As shown in Figure 1, the highest share of experts (56 per cent) used the patrimonial method, although the fundamental and financial methods together account for a comparable share of experts (53 per cent). The survey also highlighted the difficult conciliation of perspectives between sellers and buyers and the need to consider intangible factors, as seen in Figure 2.

The different methods were applied to the 2017 and 2018 French Farm Accountancy Data Network (FADN) bookkeeping data (Jeanneaux et al., 2022). Figure 3 shows that wine-growing farms have the highest values on average. Pig and beef cattle farms have high average patrimonial values, reflecting their high capital intensity. However, beef cattle farms have the lowest average values calculated with fundamental and financial methods, suggesting less favourable market conditions for these farms. Further research is needed to empirically assess the drivers of values, and in particular the part of the value that is due to intangible assets.

以当前市场价值对农场进行估价是农场转让过程中的一个关键部分,无论是通过继承在家庭成员之间进行,还是在买卖双方之间的公开市场上进行。本文解释了法国专业人员可使用和使用的农场估价方法,并介绍了这些方法在法国有代表性的商业农场记账数据中的应用结果。文献中有大量关于商业估价方法的内容,但在农业背景下则较少。一些资产通常非常具体(农场建筑、牲畜、农业用地),农场的活动本质上是多样的和有风险的,因此很难对其估价进行标准化。有两大类方法。经济方法以资产产生的现金流和盈利能力为基础,包括基本方法和财务方法。基本(或贴现现金流或长期回报或资本化)方法包括将农场作为一个工业项目进行估价,该项目将在选定的时间范围内,例如长期租赁协议的期限(在法国为九年),在未来产生现金流。因此,农场价值是以适当利率贴现的未来净现金流的总和。财务(或盈利)方法基于对农场投资者潜在薪酬的估计,可以用农场净利润(农场收入减去农场经理的劳动报酬)来近似。第二类方法依赖于主要采用继承法(或清算和会计估价法)单独估价的资产。每项有形资产都是单独估计的,采用当前市场价值或资产负债表中可用资产的账面价值。虽然买家(也就是说,未来的农民)和银行通常更喜欢基本方法,但卖家更喜欢继承方法,因为它能产生高价值。在实践中,这两套方法经常结合使用。2021年,对法国67名土地专家和农场会计师进行了一项在线调查,他们定期为农民(包括卖家或买家)估计农场价值(Enjollas et al.,2023)。如图1所示,使用世袭法的专家比例最高(56%),尽管基本方法和财务方法合计占专家比例相当(53%)。该调查还强调了卖家和买家之间难以调和的观点,以及考虑无形因素的必要性,如图2所示。2017年和2018年法国农场会计数据网络(FADN)的记账数据采用了不同的方法(Jeanneaux et al.,2022)。图3显示,葡萄酒种植农场的平均价值最高。养猪场和肉牛养殖场的平均遗产价值很高,反映出它们的高资本密集度。然而,用基本面和财务方法计算的肉牛养殖场平均值最低,这表明这些养殖场的市场条件不太有利。需要进一步的研究来实证评估价值的驱动因素,特别是无形资产的价值部分。

期刊介绍:

EuroChoices is a full colour, peer reviewed, outreach journal of topical European agri-food and rural resource issues, published three times a year in April, August and December. Its main aim is to bring current research and policy deliberations on agri-food and rural resource issues to a wide readership, both technical & non-technical. The need for this is clear - there are great changes afoot in the European and global agri-food industries and rural areas, which are of enormous impact and concern to society. The issues which underlie present deliberations in the policy and private sectors are complex and, until now, normally expressed in impenetrable technical language.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: