{"title":"Progressive taxation in the face of inflation and instability: lessons from Argentina","authors":"Roberto Arias, Vedanth Nair","doi":"10.1111/1475-5890.12344","DOIUrl":null,"url":null,"abstract":"<p>Gabriel Zucman's article in this symposium sets out an agenda for how international cooperation can overcome barriers to progressive taxation and barriers to the taxation of wealth. Argentina has been at the forefront of developments in international tax cooperation. It has been one of the global minimum tax's strongest proponents, and has pushed for it to go even further by increasing the minimum rate to 21 per cent or 25 per cent. Argentina has also made use of automatic exchange of information (AEOI) to detect offshore tax evasion, signing AEOI agreements with almost 100 countries. AEOI has had modest results for Argentina. Zucman's article notes that offshore real estate is exempted under AEOI, but offshore currency holdings – which are an important asset class for wealthy Argentinians – are also poorly reported.</p><p>Whilst international cooperation is important, it is not the only barrier that needs to be overcome to tax the wealthy. Argentina presents a case study in how a progressive tax system can unravel in the face of high and volatile inflation, and how large swings in the tax rate due to political polarisation can limit the effectiveness of tax policy. This case study will be important for other developing and developed countries which are also often experiencing the high levels of inflation and political polarisation that Argentina has struggled with for decades.</p><p>Argentina is one of the few countries to already have a comprehensive wealth tax as advocated for by Zucman.1 The wealth tax is intended to be highly progressive, but high and volatile inflation, ranging from 20 to 40 per cent in the last 15 years, has at times brought many more people into the purview of the tax than initially intended. Figure 1 shows that the threshold to start paying wealth tax fell from 15 times GDP per capita in 2007 to 2 times GDP per capita in 2015, leading to the share of wealth tax payers increasing from 0.5 per cent to 1.9 per cent of the total population. Between 2016 and 2020, the wealth tax threshold was periodically updated, and from 2021 it was indexed to the consumer price index (CPI). This has not entirely fixed the problem, as official estimates of property values, which are a major component of the wealth tax base, are not regularly updated in Argentina. As property price growth tends to be higher than the CPI rate of inflation, a lack of revaluation means that the wealth tax falls on an ever-decreasing share of true wealth.</p><p>The story is similar for personal income taxation. As Figure 2 shows, the fraction of employees who were liable for the personal income tax grew from 10 per cent to 30 per cent in just four years between 2009 and 2013, as the tax-free allowance was fixed in nominal terms despite inflation of 20–40 per cent. This was corrected in 2014, and from 2016 the personal allowance threshold was indexed to nominal wages. However, indexation failed to stop the rise in the share of employees paying personal income tax, possibly because nominal wage growth for workers just under the threshold was faster than growth in the nominal wage index used.2</p><p>This highlights a deeper question: what is the goal of indexation for personal income taxes? One potential goal is to maintain consistency in the tax system in real terms, so an individual with a constant real wage does not experience fluctuating tax rates year-on-year due to inflation. Indexation of thresholds to the CPI is a simple way to try to achieve this. Another potential goal could be to keep the share of workers within each tax bracket constant, irrespective of the inflation rate or real wage growth, which approximately preserves the progressivity of the tax system. In that case, nominal wage indexation would be more natural. However, Argentina's experience between 2016 and 2020 shows that even nominal wage indexation may not always keep the share of workers paying personal income tax constant, if nominal wage growth varies across the wage distribution or if the measure of earnings used for indexation is partial or outdated. Since 2021, Argentina has set the threshold so that the share of workers paying personal income tax remains around 10 per cent. Although this type of ad-hoc rule may not be desirable from an optimal taxation point of view, some stability after a decade of substantial fluctuation is welcome.</p><p>Political polarisation has further complicated tax stability. Prior to 2015, the wealth tax rate was 1.25 per cent. It was reduced to 0.25 per cent by the centre-right Macri administration, only to be increased to 1.75 per cent (for domestic assets) and 2.25 per cent (for offshore assets) by the left-wing Fernández administration when it came to power in 2019. Corporate income tax followed a similar trajectory. The Macri administration reduced the corporate income tax rate from 35 per cent to 30 per cent in 2017, and had planned to reduce it further to 25 per cent, but the Fernández administration restored the rate to 35 per cent. Such drastic swings in tax policies can distort the behaviour of individuals and firms, further complicating tax design. For example, firms may not increase investment in response to a corporate tax cut, if they believe that tax rates will be higher after the next election. On the other hand, revenue from a corporate tax rate increase may fall short of expectations, if firms try to delay realising profits until the next election.</p><p>Unlike high inflation, it is harder for economists to make tax systems robust to political polarisation. However, global tax floors, such as the OECD's 15 per cent minimum corporate tax rate, may at least put some constraint on tax rates being tied to the political cycle.</p>","PeriodicalId":51602,"journal":{"name":"Fiscal Studies","volume":"44 3","pages":"247-249"},"PeriodicalIF":1.3000,"publicationDate":"2023-09-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1475-5890.12344","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Fiscal Studies","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1475-5890.12344","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

Gabriel Zucman's article in this symposium sets out an agenda for how international cooperation can overcome barriers to progressive taxation and barriers to the taxation of wealth. Argentina has been at the forefront of developments in international tax cooperation. It has been one of the global minimum tax's strongest proponents, and has pushed for it to go even further by increasing the minimum rate to 21 per cent or 25 per cent. Argentina has also made use of automatic exchange of information (AEOI) to detect offshore tax evasion, signing AEOI agreements with almost 100 countries. AEOI has had modest results for Argentina. Zucman's article notes that offshore real estate is exempted under AEOI, but offshore currency holdings – which are an important asset class for wealthy Argentinians – are also poorly reported.

Whilst international cooperation is important, it is not the only barrier that needs to be overcome to tax the wealthy. Argentina presents a case study in how a progressive tax system can unravel in the face of high and volatile inflation, and how large swings in the tax rate due to political polarisation can limit the effectiveness of tax policy. This case study will be important for other developing and developed countries which are also often experiencing the high levels of inflation and political polarisation that Argentina has struggled with for decades.

Argentina is one of the few countries to already have a comprehensive wealth tax as advocated for by Zucman.1 The wealth tax is intended to be highly progressive, but high and volatile inflation, ranging from 20 to 40 per cent in the last 15 years, has at times brought many more people into the purview of the tax than initially intended. Figure 1 shows that the threshold to start paying wealth tax fell from 15 times GDP per capita in 2007 to 2 times GDP per capita in 2015, leading to the share of wealth tax payers increasing from 0.5 per cent to 1.9 per cent of the total population. Between 2016 and 2020, the wealth tax threshold was periodically updated, and from 2021 it was indexed to the consumer price index (CPI). This has not entirely fixed the problem, as official estimates of property values, which are a major component of the wealth tax base, are not regularly updated in Argentina. As property price growth tends to be higher than the CPI rate of inflation, a lack of revaluation means that the wealth tax falls on an ever-decreasing share of true wealth.

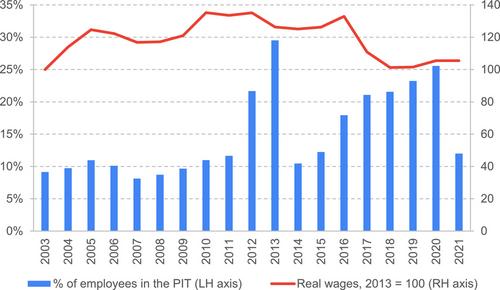

The story is similar for personal income taxation. As Figure 2 shows, the fraction of employees who were liable for the personal income tax grew from 10 per cent to 30 per cent in just four years between 2009 and 2013, as the tax-free allowance was fixed in nominal terms despite inflation of 20–40 per cent. This was corrected in 2014, and from 2016 the personal allowance threshold was indexed to nominal wages. However, indexation failed to stop the rise in the share of employees paying personal income tax, possibly because nominal wage growth for workers just under the threshold was faster than growth in the nominal wage index used.2

This highlights a deeper question: what is the goal of indexation for personal income taxes? One potential goal is to maintain consistency in the tax system in real terms, so an individual with a constant real wage does not experience fluctuating tax rates year-on-year due to inflation. Indexation of thresholds to the CPI is a simple way to try to achieve this. Another potential goal could be to keep the share of workers within each tax bracket constant, irrespective of the inflation rate or real wage growth, which approximately preserves the progressivity of the tax system. In that case, nominal wage indexation would be more natural. However, Argentina's experience between 2016 and 2020 shows that even nominal wage indexation may not always keep the share of workers paying personal income tax constant, if nominal wage growth varies across the wage distribution or if the measure of earnings used for indexation is partial or outdated. Since 2021, Argentina has set the threshold so that the share of workers paying personal income tax remains around 10 per cent. Although this type of ad-hoc rule may not be desirable from an optimal taxation point of view, some stability after a decade of substantial fluctuation is welcome.

Political polarisation has further complicated tax stability. Prior to 2015, the wealth tax rate was 1.25 per cent. It was reduced to 0.25 per cent by the centre-right Macri administration, only to be increased to 1.75 per cent (for domestic assets) and 2.25 per cent (for offshore assets) by the left-wing Fernández administration when it came to power in 2019. Corporate income tax followed a similar trajectory. The Macri administration reduced the corporate income tax rate from 35 per cent to 30 per cent in 2017, and had planned to reduce it further to 25 per cent, but the Fernández administration restored the rate to 35 per cent. Such drastic swings in tax policies can distort the behaviour of individuals and firms, further complicating tax design. For example, firms may not increase investment in response to a corporate tax cut, if they believe that tax rates will be higher after the next election. On the other hand, revenue from a corporate tax rate increase may fall short of expectations, if firms try to delay realising profits until the next election.

Unlike high inflation, it is harder for economists to make tax systems robust to political polarisation. However, global tax floors, such as the OECD's 15 per cent minimum corporate tax rate, may at least put some constraint on tax rates being tied to the political cycle.

期刊介绍:

The Institute for Fiscal Studies publishes the journal Fiscal Studies, which serves as a bridge between academic research and policy. This esteemed journal, established in 1979, has gained global recognition for its publication of high-quality and original research papers. The articles, authored by prominent academics, policymakers, and practitioners, are presented in an accessible format, ensuring a broad international readership.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: