Empirical evidence on the global minimum tax: what is a critical mass and how large is the substance-based income exclusion?

IF 1.3

3区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

Abstract

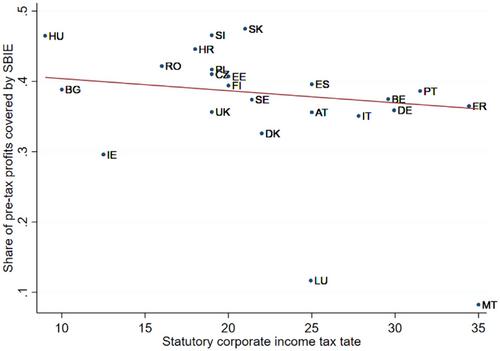

This paper presents empirical evidence on the proposed global minimum tax (GMT) of the OECD's Pillar 2. First, it addresses how many, and which, countries or country groups can be seen as constituting a ‘critical mass’ for its successful implementation; given such a critical mass, remaining jurisdictions worldwide will have an incentive to implement the GMT as well. Second, it assesses the generosity of the substance-based income exclusion (SBIE), which is informative for the revenue collected under the GMT.

关于全球最低税的经验证据:什么是临界质量,基于物质的收入排斥有多大?

本文提供了关于经合组织支柱2拟议的全球最低税(GMT)的经验证据。首先,它阐述了有多少国家或国家集团以及哪些国家或国家团体可以被视为构成其成功实施的“关键群体”;鉴于如此关键的数量,全球其他司法管辖区也将有动力实施GMT。其次,它评估了基于物质的收入排除(SBIE)的慷慨程度,这对GMT下的收入有信息性。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Fiscal Studies

Multiple-

CiteScore

13.50

自引率

1.40%

发文量

18

期刊介绍:

The Institute for Fiscal Studies publishes the journal Fiscal Studies, which serves as a bridge between academic research and policy. This esteemed journal, established in 1979, has gained global recognition for its publication of high-quality and original research papers. The articles, authored by prominent academics, policymakers, and practitioners, are presented in an accessible format, ensuring a broad international readership.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: