Rajabrata Banerjee, Tony Cavoli, Ron McIver, Shannon Meng, John K. Wilson

{"title":"Predicting long-run risk factors of stock returns: Evidence from Australia","authors":"Rajabrata Banerjee, Tony Cavoli, Ron McIver, Shannon Meng, John K. Wilson","doi":"10.1111/1467-8454.12298","DOIUrl":null,"url":null,"abstract":"<p>This study utilises the stock market data provided by the Australian Equity Database to analyse the long-run relationship between Australian stock returns and key macroeconomic variables over the period 1926–2017. To measure the diverse risk factors in the stock market, we examine the possible determinants in four main categories: real, financial, domestic and international. Our results reveal that historical stock returns are strongly connected to financial and international factors as compared to real and domestic factors. Both the 1973–1974 OPEC Oil Price Crisis and 2007–2008 Global Financial Crisis had dampening effects on stock returns. There is a positive association between the US and Australian stock markets in the long-run. These findings on stock market dynamics and their linkages with domestic and international macroeconomic policy changes in the long-run have important implications for traders and practitioners.</p>","PeriodicalId":46169,"journal":{"name":"Australian Economic Papers","volume":"62 3","pages":"377-395"},"PeriodicalIF":1.7000,"publicationDate":"2023-03-09","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8454.12298","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Economic Papers","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1467-8454.12298","RegionNum":4,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

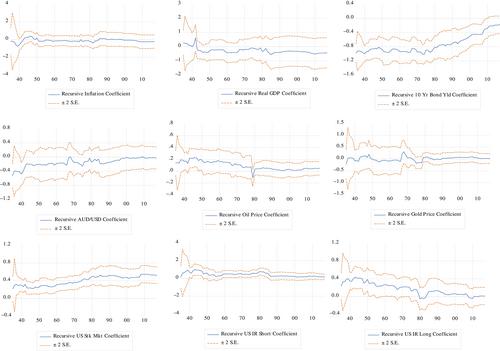

This study utilises the stock market data provided by the Australian Equity Database to analyse the long-run relationship between Australian stock returns and key macroeconomic variables over the period 1926–2017. To measure the diverse risk factors in the stock market, we examine the possible determinants in four main categories: real, financial, domestic and international. Our results reveal that historical stock returns are strongly connected to financial and international factors as compared to real and domestic factors. Both the 1973–1974 OPEC Oil Price Crisis and 2007–2008 Global Financial Crisis had dampening effects on stock returns. There is a positive association between the US and Australian stock markets in the long-run. These findings on stock market dynamics and their linkages with domestic and international macroeconomic policy changes in the long-run have important implications for traders and practitioners.

期刊介绍:

Australian Economic Papers publishes innovative and thought provoking contributions that extend the frontiers of the subject, written by leading international economists in theoretical, empirical and policy economics. Australian Economic Papers is a forum for debate between theorists, econometricians and policy analysts and covers an exceptionally wide range of topics on all the major fields of economics as well as: theoretical and empirical industrial organisation, theoretical and empirical labour economics and, macro and micro policy analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: