The valuation of corporations: a derivative pricing perspective

Abstract

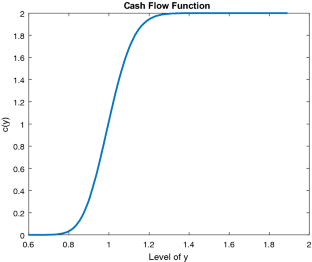

Corporations are modeled as owning a perpetual derivative security that has a claim on future cash flows. The cash flows are defined by deterministic functions of state variables. In a time homogeneous and Markovian context the value of a corporation is then given by a deterministic function of the state variables termed the corporate valuation function. This valuation function solves an integro differential equation with a boundary condition of zero at infinity. Solutions are illustrated in dimensions one, two and ten. It is observed that for positive and bounded cash flow functions the valuation functions cannot be linear. The attitude of a corporation to risk then depends on the nonlinearity. In higher dimensions the corporation will be a risk taker in some directions and simultaneously a risk avoider in others. The valuation theory also leads to new asset pricing equations inferring asset variations from risk neutral covariations. The shift from mean returns and covariances is necessitated by the focus on instantaneous risk exposures represented by measures replacing probabilities.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: