John L. Campbell, Sean Shun Cao, Hye Sun Chang, Raluca Chiorean

{"title":"The implications of firms' derivative usage on the frequency and usefulness of management earnings forecasts","authors":"John L. Campbell, Sean Shun Cao, Hye Sun Chang, Raluca Chiorean","doi":"10.1111/1911-3846.12883","DOIUrl":null,"url":null,"abstract":"<p>We investigate how firms' use of derivatives impacts voluntary disclosure and offer four main findings. First, we find that when firms begin using derivative instruments, they increase the frequency of management earnings forecasts. Second, using path analysis, we find a direct link between derivative usage and forecast frequency, as well as an indirect link through reduced earnings volatility. Third, we find that CEOs with more pronounced career concerns increase forecast frequency <i>only</i> when derivatives make earnings easier to forecast and find no evidence that investor demand drives the decision to provide a forecast. These results suggest that the primary mechanism for the association between derivative usage and forecast frequency is a reduction in the manager's costs of providing the forecasts. Finally, we find that the majority of derivative-induced forecasts are uninformative to capital market participants, especially after FAS 161 provided the necessary underlying data to understand how firms use derivatives. Overall, we provide the first empirical evidence that firms that use derivatives issue more management forecasts, but we also find that these incremental forecasts are largely uninformative and appear driven by managerial career concerns.</p>","PeriodicalId":10595,"journal":{"name":"Contemporary Accounting Research","volume":"40 4","pages":"2409-2445"},"PeriodicalIF":3.8000,"publicationDate":"2023-06-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3846.12883","citationCount":"2","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Contemporary Accounting Research","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3846.12883","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 2

Abstract

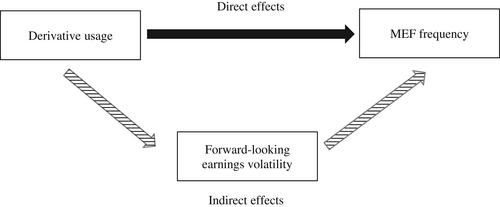

We investigate how firms' use of derivatives impacts voluntary disclosure and offer four main findings. First, we find that when firms begin using derivative instruments, they increase the frequency of management earnings forecasts. Second, using path analysis, we find a direct link between derivative usage and forecast frequency, as well as an indirect link through reduced earnings volatility. Third, we find that CEOs with more pronounced career concerns increase forecast frequency only when derivatives make earnings easier to forecast and find no evidence that investor demand drives the decision to provide a forecast. These results suggest that the primary mechanism for the association between derivative usage and forecast frequency is a reduction in the manager's costs of providing the forecasts. Finally, we find that the majority of derivative-induced forecasts are uninformative to capital market participants, especially after FAS 161 provided the necessary underlying data to understand how firms use derivatives. Overall, we provide the first empirical evidence that firms that use derivatives issue more management forecasts, but we also find that these incremental forecasts are largely uninformative and appear driven by managerial career concerns.

期刊介绍:

Contemporary Accounting Research (CAR) is the premiere research journal of the Canadian Academic Accounting Association, which publishes leading- edge research that contributes to our understanding of all aspects of accounting"s role within organizations, markets or society. Canadian based, increasingly global in scope, CAR seeks to reflect the geographical and intellectual diversity in accounting research. To accomplish this, CAR will continue to publish in its traditional areas of excellence, while seeking to more fully represent other research streams in its pages, so as to continue and expand its tradition of excellence.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: