{"title":"Random sources correlations and carbon futures pricing","authors":"Ling Feng, Jieyu Wang","doi":"10.1016/j.irfa.2023.102529","DOIUrl":null,"url":null,"abstract":"<div><p><span>For a long time, the correlation between random sources has never been considered in carbon futures pricing, which virtually exists. We document the presence of high correlation between variations in convenience yields of carbon futures with different maturities, whose essence is correlation between random sources. Correlation of random sources arises from the long coverage of convenience yield of </span>carbon emission spot and the complementarity in expiration between carbon futures with different maturities. Since if random sources are correlated will significantly affect the dynamics of convenience yield and finally affect futures prices, we introduce quantum field method to account for the impact of this correlation on futures prices, and proposes the correlation between random sources extended HJM convenience yield model (CRS-HJM-CYM). Empirical results indicate CRS-HJM-CYM performs better than traditional model owing to the role of correlation, which means the correlation between random sources is a pivotal factor in carbon futures pricing.</p></div>","PeriodicalId":48226,"journal":{"name":"International Review of Financial Analysis","volume":"86 ","pages":"Article 102529"},"PeriodicalIF":9.8000,"publicationDate":"2023-03-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Review of Financial Analysis","FirstCategoryId":"96","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S1057521923000455","RegionNum":1,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 1

Abstract

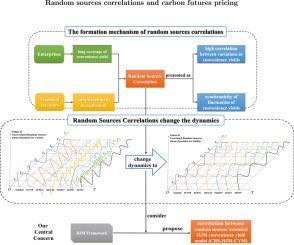

For a long time, the correlation between random sources has never been considered in carbon futures pricing, which virtually exists. We document the presence of high correlation between variations in convenience yields of carbon futures with different maturities, whose essence is correlation between random sources. Correlation of random sources arises from the long coverage of convenience yield of carbon emission spot and the complementarity in expiration between carbon futures with different maturities. Since if random sources are correlated will significantly affect the dynamics of convenience yield and finally affect futures prices, we introduce quantum field method to account for the impact of this correlation on futures prices, and proposes the correlation between random sources extended HJM convenience yield model (CRS-HJM-CYM). Empirical results indicate CRS-HJM-CYM performs better than traditional model owing to the role of correlation, which means the correlation between random sources is a pivotal factor in carbon futures pricing.

期刊介绍:

The International Review of Financial Analysis (IRFA) is an impartial refereed journal designed to serve as a platform for high-quality financial research. It welcomes a diverse range of financial research topics and maintains an unbiased selection process. While not limited to U.S.-centric subjects, IRFA, as its title suggests, is open to valuable research contributions from around the world.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: