Short interest and the stock market relation with news sentiment from traditional and social media sources

IF 1.7

4区 经济学

Q3 ECONOMICS

引用次数: 2

Abstract

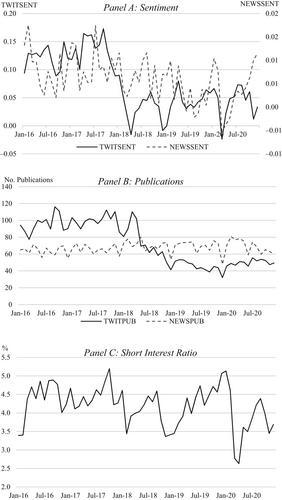

We examine how the stock market relation to news sentiment—from traditional and social media (Twitter) sources—interacts with short selling of stocks. Our sample includes the S&P500 constituents for the period January 2016 to December 2020, providing 704,452 firm-day observations. We find evidence that both news sources are positively related to returns. The relationship is stronger for firms with a high short interest ratio, for small firms, and particularly for firms that are both small and highly shorted. This is consistent with short sellers targeting firms that are most responsive to (negative) news releases and so more likely to compensate for the additional costs encountered in shorting.

空头兴趣和股市与传统和社交媒体来源的新闻情绪的关系

我们研究了股票市场与来自传统和社交媒体(Twitter)来源的新闻情绪的关系如何与股票卖空相互作用。我们的样本包括2016年1月至2020年12月期间的标准普尔500指数成分股,提供了704,452个固定日观察结果。我们发现证据表明,这两种新闻来源都与收益呈正相关。这种关系对于拥有高空头利率比率的公司、小公司,尤其是那些既小又高度做空的公司来说更强。这与卖空者瞄准对(负面)新闻发布最敏感的公司是一致的,因此更有可能补偿卖空所遇到的额外成本。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Australian Economic Papers

ECONOMICS-

CiteScore

3.20

自引率

5.30%

发文量

36

期刊介绍:

Australian Economic Papers publishes innovative and thought provoking contributions that extend the frontiers of the subject, written by leading international economists in theoretical, empirical and policy economics. Australian Economic Papers is a forum for debate between theorists, econometricians and policy analysts and covers an exceptionally wide range of topics on all the major fields of economics as well as: theoretical and empirical industrial organisation, theoretical and empirical labour economics and, macro and micro policy analysis.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: