{"title":"Removing Barriers to Whistleblowing at Nonprofit Organizations through Employee Empowerment*","authors":"Paulina Arroyo Pardo, Nadia Smaili, Souad Bensid","doi":"10.1111/1911-3838.12332","DOIUrl":null,"url":null,"abstract":"<p>This study explores how key organizational and governance actors perceive the effectiveness of whistleblowing at nonprofit organizations (NPOs) and how whistleblowing is interrelated with other anti-fraud mechanisms. Using a systems approach, we develop a conceptual framework of anti-fraud mechanisms consisting of a set of interrelated components: control-focused mechanisms and employee-focused mechanisms (whistleblowing) intended to prevent and detect fraud, influenced by the environment (regulation and stakeholders) and human factors (employees' attitudes and leaders' awareness of fraud). We conducted 14 semistructured interviews with key actors at Canadian NPOs and noted that diverse control mechanisms were in place at these groups, but seemingly no formal whistleblowing policy existed. The organizations were disinclined to formalize a whistleblowing system in the short term despite viewing such a system as effective. Whereas prior research has examined the role of control-focused mechanisms, NPOs' adoption of whistleblowing systems, and the benefits thereof, we contribute to the literature by stressing that employee empowerment is crucial to overcoming reluctance to blow the whistle. If the board of directors is aware of fraud risk and provides employees with the resources, motivation, and protection to speak up, whistleblowing could be implemented in these organizations. Whistleblowing should be interrelated with other mechanisms to form an effective anti-fraud system.</p>","PeriodicalId":43435,"journal":{"name":"Accounting Perspectives","volume":"23 2","pages":"267-300"},"PeriodicalIF":0.9000,"publicationDate":"2023-02-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1911-3838.12332","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Accounting Perspectives","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1911-3838.12332","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

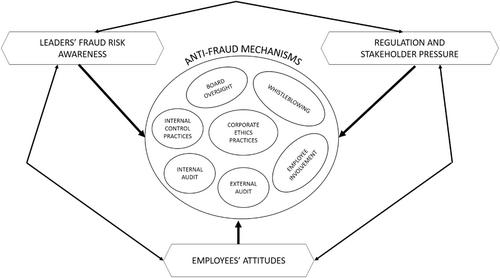

Abstract

This study explores how key organizational and governance actors perceive the effectiveness of whistleblowing at nonprofit organizations (NPOs) and how whistleblowing is interrelated with other anti-fraud mechanisms. Using a systems approach, we develop a conceptual framework of anti-fraud mechanisms consisting of a set of interrelated components: control-focused mechanisms and employee-focused mechanisms (whistleblowing) intended to prevent and detect fraud, influenced by the environment (regulation and stakeholders) and human factors (employees' attitudes and leaders' awareness of fraud). We conducted 14 semistructured interviews with key actors at Canadian NPOs and noted that diverse control mechanisms were in place at these groups, but seemingly no formal whistleblowing policy existed. The organizations were disinclined to formalize a whistleblowing system in the short term despite viewing such a system as effective. Whereas prior research has examined the role of control-focused mechanisms, NPOs' adoption of whistleblowing systems, and the benefits thereof, we contribute to the literature by stressing that employee empowerment is crucial to overcoming reluctance to blow the whistle. If the board of directors is aware of fraud risk and provides employees with the resources, motivation, and protection to speak up, whistleblowing could be implemented in these organizations. Whistleblowing should be interrelated with other mechanisms to form an effective anti-fraud system.

期刊介绍:

Accounting Perspectives provides a forum for peer-reviewed applied research, analysis, synthesis and commentary on issues of interest to academics, practitioners, financial analysts, financial executives, regulators, accounting policy makers and accounting students. Articles are sought from academics and practitioners that address relevant issues in any and all areas of accounting and related fields, including financial accounting and reporting, auditing and other assurance services, management accounting and performance measurement, information systems and related technologies, tax policy and practice, professional ethics, accounting education, and related topics. Without limiting the generality of the foregoing.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: