Joseph E. Aldy, Patrick Bolton, Marcin Kacperczyk, Zachery M. Halem

{"title":"Behind schedule: The corporate effort to fulfill climate obligations","authors":"Joseph E. Aldy, Patrick Bolton, Marcin Kacperczyk, Zachery M. Halem","doi":"10.1111/jacf.12560","DOIUrl":null,"url":null,"abstract":"<p>The 2015 Paris Agreement represented the first multilateral agreement to acknowledge and support efforts by so-called non-state actors, including corporations, to cut their greenhouse gas emissions. Moreover, the goals and structure of the Paris Agreement—focused on limiting warming to well below 2°C relative to pre-industrial levels and allowing for national governments to set voluntary emission goals—have informed the setting and adoption of voluntary corporate commitments. Some corporations have taken on “Paris-aligned” emission commitments, indicating that they would deliver emission reductions consistent with the temperature objective of the 2015 agreement. With the increasing adoption of mid-century net-zero emission goals by national governments, some corporates have likewise adopted their own net-zero emission commitments.</p><p>Before the Paris Agreement few companies had made commitments to reduce their carbon emissions. Most of them did so through the Carbon Disclosure Project (CDP), which benefited from the momentum generated by the Paris agreement to substantially expand the number of companies that would make decarbonization pledges and voluntarily disclose their carbon emissions. Later, CDP along with the United Nations Global Compact, the World Resources Institute (WRI), and the Worldwide Fund for Nature, founded the Science-Based Target initiative (SBTi) to engage with companies to implement carbon reduction commitments that are aligned with the Paris agreement and the goal of limiting global overheating to less than 2°C above pre-industrial levels. As Mark Carney had predicted in the run-up to the COP 26 in 2021, “More and more companies—and it will be a tsunami by Glasgow—will have net zero emissions plans.”1 As of this writing, SBTi can boast that “more than 4,000 businesses around the world are already working with the Science-Based Targets initiative.”2</p><p>Other major decarbonization drives in the wake of the Paris agreement have emerged in the financial sector, with the launch of the Task Force on Climate-Related Financial Disclosures in 2015, Climate Action 100+ in 2017, the inauguration of the Asset Owners Net-Zero Alliance in 2019 together with the Net Zero Asset Managers Initiative in 2020, and, the culmination of this wave of initiatives, the creation of the Glasgow Financial Alliance for Net Zero by Mark Carney at the COP 26 in April 2021. In parallel, the Network for Greening the Financial System (now comprising 121 central banks and financial supervisory authorities) was set up in 2017, providing guidance on net zero compatible decarbonization pathways. In short, the Paris agreement has ushered in a new era of decarbonization commitments.</p><p>An important aspect of emission reduction commitments is the extent to which they specify interim targets. Commitments are less credible when they specify distant targets and are vague about the pathway toward attaining the target. Businesses cannot decarbonize overnight. Eliminating GHG emissions is inevitably a gradual process, which involves replacing old operating facilities as they depreciate with new facilities powered by renewable energy. The cost of decarbonization can be reduced if this replacement of old with new plants and equipment is spread out over time—hence the net zero targets that are decades away. There is considerable uncertainty over such a long period, which could produce new technological breakthroughs, new green regulations, or new pandemics and wars that disrupt energy supplies. Thus, companies need flexibility and cannot tie themselves to a pathway that is too rigid. On the other hand, the risk of missing the ultimate target is greater if companies do not specify interim milestones.</p><p>Many companies that do make commitments to decarbonize do specify such milestones. For these companies we can determine whether they are on track or are falling behind. We also explore how the market reacts when a company falls behind or abandons its commitments mid-course. When we do so, we find little evidence of a backlash.</p><p>A case in point is the February 2023 announcement by BP that it would delay its near-term commitment to reduce oil and gas production, changing its 2030 target from a 40% to just a 25% reduction. Despite considerable criticism, BP has so far suffered no negative effects from this move. On the contrary, its stock price increased significantly following its announcement of the change in plans (though likely attributable to concurrently announced soaring oil profits).</p><p>To illustrate the implications of the Paris approach through voluntary corporate actions, we frame our analysis through three conceptual interrogations. First, in section “<i>Incentives for Corporations to Adopt Voluntary Commitments</i>” we examine what induces companies to make decarbonization pledges on a voluntary basis. We also study how corporate pledges take account of uncertainty and changing circumstances. In section “<i>What are corporations pledging to do, and how are they</i>”, we show how companies have managed to fulfill their pledges so far, and the extent to which their decarbonization trajectories are consistent with their ultimate targets. In section “<i>The broader commitments landscape: countries, universities</i>”, we look beyond corporate commitments and study the role of commitments by countries, universities, and asset managers. In section “<i>How to handle failing commitments?”</i>, we discuss various ways in which companies and regulators could adjust to the possibility of failing commitments.</p><p>The conventional wisdom about corporations and the environment has long reflected two major themes: (1) Milton Friedman's 1970 proclamation that the “the social responsibility of business is to increase profits”; and (2) the imposition by environmental regulations of significant costs on business.3 In recent years, however, corporations have pursued various forms of self-regulation, including the adoption of voluntary greenhouse gas emission commitments. In contrast to the conventional wisdom, corporate management may have a more nuanced take on the incentives and rationale for committing to emission-reduction goals. With growing attention to addressing the risks posed by a changing climate among consumers, investors, workers, and other stakeholders, corporate managements may find it in their interest to cut their greenhouse gas emissions.</p><p>With a growing interest among consumers in the environmental characteristics of the goods and services they purchase, a corporation may find that “signaling” its efforts to address climate change may facilitate product differentiation and increase market share and/or mark-ups. Especially in retail-facing environments, corporates have found value in enhancing their brand and image through public efforts to demonstrate their social responsibility.4 The challenge with such a strategy of drawing attention to emission-cutting efforts lies in the prospect that some stakeholders, both those in the investment community and civil society, may accuse the corporate of <i>greenwashing</i>—that is, misleading the public about the environmental impact of the corporation.</p><p>Corporations operate under a patchwork of energy, climate, and tax policies that may influence the adoption of an emission commitment. In some contexts, a corporation may already face significant regulatory requirements, such as those operating under the EU Emission Trading System or in California, associated with its own cap-and-trade program, as well as renewable and low-carbon requirements in its power and petroleum refining sectors. The incremental effort—and hence opportunity cost of investment—would be lower for such corporations covered by regulations to attain any given emission goal than for other corporations operating beyond the scope of regulatory mandates. To the extent that regulations have targeted relatively more expensive ways for a corporate to reduce emissions, there may be residual low-cost emission reductions that could easily enable the corporate to meet emission targets that are more ambitious than its regulatory requirements. Moreover, the experience and information gained from undertaking investment necessary to comply with regulatory mandates may facilitate actions to cut emissions by reducing the uncertainty associated with such future investment's returns.</p><p>In a similar manner, corporations operating in jurisdictions with generous subsidies for investing in clean energy technologies—such as tax credits for installing solar panels, loan guarantees for investing in novel emission capture equipment, and grants for improving the energy efficiency of its facilities—may find the incremental costs of cutting emissions to be low and, indeed, the marginal abatement cost function within the firm may be considerably flatter with public subsidies. For example, the Inflation Reduction Act of 2022 makes available an array of clean energy investment tax credits—in the power, transportation, manufacturing, and buildings sectors—that cover 30% of investment costs. In addition to subsidies for reducing emissions within the corporate footprint, some companies have focused on the potential for low-cost emission offset projects beyond the corporate footprint as a way to reduce their costs of meeting a net-emissions target.5</p><p>The interests and preferences of two sets of key stakeholders for corporate managers—the investors they answer to and the workers they recruit and manage—could also inform the decision-making calculus over the adoption of an emission target. Investors with green preferences as well as those focused on aligning long-term returns to long-term liabilities (such as pension plan asset managers) may have a strong interest in ensuring that the corporates they invest in have developed credible strategies for managing decarbonization transition risk. With growing shareholder activism and the use of shareholder resolutions to drive green changes in management practices, corporate managers may pursue voluntary emission targets as a means to address and manage such pressures.6 Moreover, with growing interest in climate change among younger generations, managers may find that a well-developed climate change program—perhaps as a part of a broader corporate social responsibility agenda—helps facilitate the recruitment and retention of high-quality, new workers in the workforce.</p><p>Finally, a corporate may adopt voluntary emission targets and an associated emission-reduction plan to influence future government policy and regulation. In some cases, aggressive and credible corporate emission cuts could preempt regulation. In other cases, such aggressive efforts could shape the future of regulation and provide a corporate with greater voice in designing the policy, which may enable it to acquire value or impose costs on laggard competitors from policy design. A corporate may also signal to regulators a feasible path for policy ambition through its own goals and its use of an internal carbon price. Recent scholarship illustrates how corporates headquartered in jurisdictions with carbon pricing are more likely to employ an internal carbon price in their operations and strategy development, and that such internal carbon prices are higher in those regions with higher carbon prices under the jurisdiction's climate policies.7</p><p>While these are possible explanations for why a corporate adopts a voluntary emission commitment, quantitative analysis can inform our understanding of whether doing so increases the value to the corporate. In an article by several of us in this journal in 2022, we presented the results from multivariate regression models we used to isolate the effect of commitments on price-to-earnings ratios, building on previous work that quantified the relationship between Scope 1 carbon emissions and price-to-earnings ratios (producing firm-level carbon valuation discount rates).8 Our analysis finds that participating in a CDP initiative can offset, on average, 15% of the firm's carbon valuation discount, though the lack of statistical significance suggests that this result is not robust (the same holds for SBTi pledges). Chosen parameters for pledges (length and targets) have no real impact on firm valuation either. Sector results also display insignificant valuation effects, with the one outlier being financials: Financial companies making pledges get a further valuation discount, possibly attributable to costs associated with the transition to net-zero financed emissions.</p><p>In theory, there are two opposing effects that underlie the financial decision-making associate with corporate pledges to meet emissions targets. Making such pledges could signal higher near-term financial costs, since decarbonizing operations or purchasing carbon offsets is likely to be costly. But to the extent such outlays work to limit the pledging companies’ exposure to transition risk, the announcement of such pledges could be seen by investors as increasing value, at least in the medium and longer run. The lack of any notable valuation changes from such commitments could be a consequence of these effects offsetting one other. More likely, our findings around the differential between actual decarbonization rates and pledged abatement rates, and given the increased public scrutiny of greenwashing, suggest investors’ skepticism about the genuineness of commitments to future emission reductions. Investors may interpret pledges, at the present, less as serious commitments and more as public relations moves. Thus, they may be waiting to view commitments as financially material until after greater progress in meeting pledges has been demonstrated.</p><p>A common step for companies before making a decarbonization pledge is to report carbon emissions. A remarkable first finding that emerges from our analysis is that a steadily growing fraction of Russell 3000 companies, which are responsible for the largest share of corporate carbon emissions, has chosen to report their GHG emissions from 2010 to 2020. By now around a quarter of large cap companies disclose their emissions. Along with a rising rate of carbon disclosures, corporations have increasingly made decarbonization pledges, with the number of CDP pledges—the earliest platform set up to encourage corporations to make decarbonization pledges—more than doubling over this period. CDP along with the UN Global Compact, the Worldwide Fund for Nature (WWF), and the WRI, later launched the SBTi, which provides further guidance to companies in aligning their pledges with net zero targets. SBTi pledges are more rigorous, and to date a much smaller fraction of companies have made SBTi commitments (4% compared to 15% for CDP pledges). Breaking carbon reduction pledges down by sector, we find that the highest fraction are companies in the utilities sector (46%), followed by those in consumer staples (35%), and materials (31%).</p><p>We find that most corporate pledges have a short horizon, with close to 50% of pledges specifying a target date less than five years away. To be sure, some pledges have a 2050 target, but these represent only 6% of the corporate pledges in our sample. As for the pledged rates of carbon reduction, we found that they are widely dispersed, with 70% of pledges committing to a total reduction of emissions that is less than 40% of base year emissions. Only 7% of companies in our sample have pledged to completely decarbonize.</p><p>It is perfectly possible, even plausible, that if all the companies that have made pledges completely realized their commitments, the total carbon emission reduction would fall short of what is necessary to avoid overheating by more than 1.5°C or 2°C, for the simple reason that many companies with very high levels of carbon emissions have as yet failed to make any pledges to decarbonize. Also, it is to be expected that when (short-run) economic incentives do not line up, even willing companies would not go the distance and make pledges that could prove to be very costly.</p><p>To assess the seriousness of corporate commitments to making good on their pledges, we compare the <i>effective</i> annual abatement rates consistent with their pledges (under a linear reduction rate) to their actual decarbonization rates after they have made their commitments public. We note that this is a conservative assumption given that energy-economic models of countries/regions for national emission goals (or more commonly, global temperature/atmospheric concentration stabilization goals) tend to show greater than linear reductions in the near term (for easier-to-abate emissions) and less than linear reductions in the longer term (for harder-to-abate emissions). Based on 10-year annual decarbonization averages, we observe that 72% of companies have been falling behind and will need to accelerate their emission reductions going forward to be able to meet their targets. This fraction of laggards is marginally lower when we look at decarbonization rates over a more recent (three-year average) time frame. Indeed, we find that 56% of pledging companies are underperforming over that span relative to a trajectory toward their stated decarbonization targets.</p><p>It is important to find out what causes companies to fall behind on their commitments. Is it largely because of an unexpected energy supply shock, such as the Russian invasion of Ukraine, or because companies have overpromised? One way to find out is to look at the distribution of commitment failures across the companies that have made commitments. If companies are falling behind because of an aggregate shock like the war on Ukraine, then we would expect to see similar commitment failures across all companies. But if a large number of companies are falling behind because they have overpromised, we would not expect to see a uniform commitment failure across all companies. As above, we define a commitment failure as the positive difference between the pledging companies’ percentage changes in Scope 1 emissions relative to annual abatement rates implied by CDP targets with longest horizon.</p><p>We begin with the tabulation of the unconditional values of this failure variable for the entire sample of firms making CDP commitments. Our findings, as summarized in Figure 1, show that the average firm in our sample is failing to meet its CDP commitment by 5.8 percentage points. The median shortfall is 3.1 percentage points, which is a consequence of the disproportionately large failures of a small number of companies (as reflected in the right skewness in the sample).</p><p><b>Why are Some Companies Failing on their Commitments?</b> These results do not tell us much about the underlying sources of failures, but they do suggest that for many companies making overly optimistic promises has been an issue. Do failures happen more in certain industries, companies with certain characteristics, or in certain time periods? These are the questions we aim to answer next.</p><p>First, we define “failing” commitments. Generally, a failing commitment could refer to a corporate missing a terminal target, missing an intermediary target, reneging on a pledge, or falling behind (over some time span) on a committed decarbonization trajectory. In our analytical treatment, we define the failure measure as the differential between pledged emissions reduction (under a linear reduction rate) and actual emissions reduction from 2010 to 2020. The sample is companies in the Russell 3000. Table 1 displays the summary statistics for pledging companies from the cross-section of 11 industrial sectors in our sample. We present mean, median, 25th and 75th percentiles, as well as standard deviations of the failure measures for each sector.</p><p>As reported in the table, we find, first of all, that the average pledging company fails to meet its CDP target across all industry sectors, with the largest deviations being observed in Communication Services, Materials, and Information Technology. The smallest failures are in the Utilities, Industrials, and Financials sectors. When we focus on median values of commitment failures, we note that the values are smaller, albeit still positive for 10 out of 11 sectors. The notable exception is the Utilities sector.</p><p>Second, we find significant dispersion in failures within sectors, as indicated by the large values of the standard deviations of the failure measure. Given that failures do not seem to cluster within individual sectors, it seems that the more likely reasons for failure can be traced to either broad macro shocks (like those associated with the Ukraine War) or differences in individual company circumstances within a sector. We attempt to provide more evidence on the former by looking at the distribution of failures over time.</p><p>As can be seen in Table 2, we observe a reasonably consistent distribution of failures over time, though with some interesting patterns. First, failures have been generally going down over time, with the notable exceptions of 2017 and 2018, when failure rates actually went up. This general downtrend could explain why more firms were joining CDP. On the other hand, some of the increases in failures could be partly explained by adverse selection, in the sense that companies that join later are less able to meet their commitments. Second, the global lockdown in 2020 clearly contributed to a reduction in the magnitude of failures, in turn attributable to the significant drop in emissions from the economic slowdown caused by COVID lockdowns. Third, within each year we observe a significant variation in failures, which suggests that at least some of the variation in failures is likely idiosyncratic in nature.</p><p>In the next set of results, we explore some of the firm-specific differences across companies. We consider a number of corporate characteristics: the maximum year for which companies make commitments, market capitalization, ROE, level of Scope 1 emissions, Scope 3 upstream emissions, sales growth, and book to market equity. In Table 3 we report means, medians, and standard deviations of failure variables for companies whose values of each characteristic are below median and above median for the given characteristic in our sample.</p><p>Among our most interesting observations, we start by noting that pledging companies with longer-horizon targets on average experience lower failure margins than companies with shorter target dates. This may seem counterintuitive since companies with longer-term pledges might be assumed to face greater uncertainty, and companies making more distant commitments may do so to delay their decarbonization. But this finding could also instead suggest that more gradual decarbonization pathways are more realistic to achieve. Second, we do not find significant differences across companies with different market capitalizations, profitability, and B/M ratios. What we do find, however, is that companies with higher emissions, especially Scope 3 upstream emissions, are more likely to fail by bigger margins. This result is consistent with our earlier finding that best-in-class companies are both more likely to commit and to set ambitious targets.9</p><p>Finally, we observe that the degree of commitment failure is a fairly direct function of sales growth. Companies with higher sales growth are more likely to fail their commitments. This result suggests that when companies experience an unexpectedly large sales growth they find it difficult to meet their decarbonization promises, or at the very least that companies that set targets without properly accounting for their future growth potential are likely to fail to deliver on their promises. But such considerations notwithstanding, it is notable that within each sorted group we observe significant differences among companies, as reflected in the large standard deviations—which in turn suggest that the reasons behind the failures are not simple and likely reflect the complexity of multi-dimensional business models.10</p><p>But if companies have been falling behind in carrying out their commitments, other non-corporate entities, nations, asset managers, and universities have also faced challenges in making adequate commitments and in implementing them. In this section, we provide a sketch of this broader context to make clear that the challenges that corporations have faced are by no means unique to them.</p><p>By the end of 2022, around 140 countries representing over 91% of global CO<sub>2</sub> emissions have made NZ pledges.11 The target year is most often 2050, but some countries like Sweden have a more ambitious target year (2045) and others like China a less ambitious target year (2060). A few countries like the United Kingdom have even enshrined their NZ commitment into law. Such ambitious goals require largescale, near-term emission-cutting programs, but few countries have undertaken action consistent with their net-zero goals. Under the Paris Agreement, countries have issued emission pledges for 2030. If all countries implemented these pledges, global emissions would fall by a mere 11% through the end of this decade.12 In its annual <i>Emissions Gap Report</i> of 2022, the UN Environment Programme finds that countries are falling behind on their 2030 goals, which they note are insufficient to keep the world on track to limiting warming to 2°C or less.13 The Environmental Performance Index (EPI) published every 2 years by scholars from Yale and Columbia, deems that only Denmark, Great Britain, Botswana, and Namibia are on track to achieving net-zero greenhouse gas (GHG) emissions by 2050.</p><p>Academic institutions, important voices that could drive climate change mitigation, have struggled in implementing their decarbonization pledges. Before the recent wave of corporates voluntarily adopting emission commitments, higher education institutions adopted ambitious carbon emission goals. With this head start, about a dozen institutions of higher learning have announced that they have reached net-zero emissions as of 2020.14 These efforts illustrate how such institutions framed their net-zero goals, especially in terms of the scope of emissions coverage, and what actions they undertook to deliver on these goals.</p><p>These forward-leaning higher education institutions set net-zero emission goals that covered the emissions within their institutional footprint (Scope 1), the carbon emissions associated with their purchase of electricity (Scope 2), and a limited accounting of their supply chain (Scope 3) emissions, primarily institution-funded airline travel and employee commuting. With increased interest in both upstream and downstream emissions associated with corporates, this narrow Scope 3 focus provides limited insights for current policy debates but does highlight what are fundamental data challenges in adopting an emissions commitment that includes emissions beyond the boundary of the firm.</p><p>A 2021 analysis by several Harvard Scholars shows that in practice, less than 20% of the emission reductions associated with reaching net-zero occurred in higher education institutions’ Scope 1, Scope 2, and Scope 3 emissions footprints.15 Several institutions relied extensively on biological sequestration on college-owned land, although doing so effectively assumes that, in the absence of the net-zero policy, the colleges would have clearcut all of their lands. More than 60% of the emission reductions necessary to attain net-zero occurred through the purchase of emission offsets and unbundled renewable energy credits. The offsets typically came from landfill methane and forestry projects, but the emission additionality of many of these types of projects have been challenged in recent years.16 The purchase of unbundled renewable energy credits likely do little to increase renewable power investment and generation, and instead simply represents a financial transfer to existing renewable power generators. In most cases, the improving carbon intensity of the local generation mix, reflecting decisions beyond those of university administrators, enabled the institutions to make progress on their Scope 2 emissions.</p><p>The Harvard scholars conclude that the considerable progress made by these institutions provides important lessons for the next steps in voluntary decarbonization.17 They note, with reservation, that the extensive reliance on offsets and unbundled renewable energy credits do not serve as a model that can be replicated more broadly and still deliver on economy-wide net-zero goals.</p><p>In addition to corporates and universities, an increasing number of investors have made pledges to reduce the emissions associated with their portfolios. The Net Zero Asset Management Alliance (NZAM), which was launched in 2020, is one of the most ambitious initiatives to promote net-zero goals. Despite its rapid growth in membership and economic significance, however, the initiative has also faced significant backlash recently from critics in the finance industry and from politicians, which has somewhat undermined its future success. An example of such a backlash is the recent decision by Vanguard to withdraw publicly from its commitment to NZAM.</p><p>In December 2022, Vanguard announced that it was withdrawing from the Net Zero Asset Managers initiative amid questions raised by the US Senate Committee on Banking, Housing and Urban Affairs over whether it is appropriate for passive investment managers to engage with issuers on “stewardship” issues such as climate change. The suggestion was made that passive index investors such as Vanguard may not have a mandate to engage with their portfolio companies toward a goal of achieving net zero emissions.</p><p>Given the significance of Vanguard as one of the leading asset managers, the concern is that such developments could call into question the long-term viability of the various asset management climate coalitions.</p><p>We first examine firms that have “failed” to make a commitment in the first place. According to the most recent evidence from MSCI this year, the proportion of listed companies that have self-declared net-zero targets is 17%.18 While ostensibly low, this proportion has actually risen from 10% in 2022 to 17% in 2023. But this still means that 83% of listed companies do not have any net-zero targets. Admittedly, the proportion of companies with some decarbonization targets has risen to 44% in 2023. Yet, this still means that over half of all listed companies have failed to make any commitment at all. And there is even less transparency about commitments and emission reduction efforts among privately held companies.</p><p>This broad-brush assessment may paint an excessively pessimistic picture, for some companies do not make any pledges because their emissions are low anyway. To gain more perspective on this apparent lack of corporate commitments, it is instructive to look at the breakdown by industry. The same report tells us that the proportion of self-declared net-zero targets is highest in the utilities sector, with 38% of companies, second highest in the energy sector, with 28%, and third highest in the consumer staples and materials industries, with 21%. This compares with only 6% of companies making such pledges in the health care sector.</p><p>Another instructive breakdown is between 1.5°C aligned and misaligned companies based on their self-declared commitments. Roughly 19% of companies are deemed to be 1.5°C aligned by MSCI in 2023, but the same proportion is deemed to be strongly misaligned, and 32% of companies are deemed to be 2°C aligned and 31% of companies are 2°C misaligned.</p><p>The other way in which commitments can fail—often the exclusive focus of greenwashing critics—is when implementation is falling behind. How can companies, which after all are declaring their concerns about climate change and are stepping up to the plate, avoid falling behind? How can they avoid missing intermediary targets, or worse, backtrack on their pledges at a later date? It is helpful to break down the answers to these questions into two broad categories of responses, <i>internal</i>, at least at the time when it decides to make a pledge, and <i>external</i>.</p><p>Regarding internal responses, one often hears that companies are facing a lot of uncertainty about their future ability to abide by their pledges, especially if their targets are far into the future. Firms do not have full control over their emissions. This is obviously the case for Scope 2 and 3 emissions, but also for Scope 1 emissions. Firms may have a plan to replace a fossil fuel energy source with a renewable one but may find unforeseen obstacles along the way, such as supply chain disruptions or delays in necessary overhauls of the electricity grid.</p><p>How should companies respond to these hazards? Many first-generation corporate pledges have essentially side-stepped these issues and, hoping for the best, have made commitments without a careful evaluation of their ability to meet their pledges in all circumstances. Given our findings above, a large fraction of companies that have made commitments clearly did not see their (in hindsight) optimistic scenarios materialize.</p><p>How can companies avoid ending up in a similar situation in the future? One possible answer is to <i>stress-test</i> their commitments before announcing them. Just as bank balance sheets are stress- tested to see if they can withstand an adverse non-performing loans shock, commitments could be stress-tested against shocks that could affect the company's future emissions. Would the company be able to still meet its targets in the event of an adverse shock? By stress-testing their planned commitments, companies can determine what cushion they have in adjusting their emissions following an adverse shock, to avoid falling behind.</p><p>Another response, of course, could be to accept that the company may fail to meet its pledges under adverse circumstances. Such a response, however, may call for a new generation of pledges that are <i>state-contingent</i>. The company could gain more credibility if it were more upfront about the circumstances in which it can and cannot meet its pledges. Or, if it is difficult to anticipate and describe these circumstances, the company could include <i>force majeure</i> clauses in its pledges that clearly state that it may not always be able to meet its pledges and that describe what the company will do with respect to its decarbonization commitments under such circumstances.</p><p>Most companies set <i>net</i> carbon emission targets that combine gross emission reduction targets with the purchase of carbon offsets. One way in which companies can make up for an unexpected increase in their emissions is to purchase more offsets to be able to meet their targets. Indeed, many companies making commitments approach the implementation of their commitments in this way. They see the purchase of offsets as a last resort for meeting their targets. But what if the offsets themselves fail? What if carbon credits are based on a nature-based carbon sink and that sink disappears following a wildfire? How should companies respond? To be credible, companies should at the very least replace the credits that have vanished in this way. This is far from happening now. Another step towards greater credibility that companies could take is to announce both gross and net emission targets, as proposed by as proposed by some of us in a 2021 <i>Management and Business Review</i> article.19 This way analysts can more easily assess the fragility of pledges and the extent to which they excessively rely on offsets.</p><p>Current “science-based” methodologies that are used to determine net-zero targets are tailored to the specific production technologies of each industry and are based on best current estimates of future technical innovations. However, they do not always sufficiently take into account variations in firm characteristics within an industry. Also, they do not reflect potential unexpected changes in operations and different technological choices and innovations that firms might take. Some energy companies may make a bet on hydrogen, others on biofuel, or on carbon capture and sequestration. The prospects of each of these technologies are different. Some of these may deliver on their promise, others not. Accordingly, pledges must be able to reflect this fundamental technological uncertainty.</p><p>Faced with such wide technological uncertainty companies may prefer to keep their options open and delay committing to a particular decarbonization solution. But companies that choose this approach risk being lumped together with companies that are unwilling to do anything and are “strongly misaligned” with the goals of the Paris agreement. How can they avoid that? One approach could be to commit to a decarbonization process by introducing governance changes that facilitate and accelerate future decarbonization when technological uncertainty is sufficiently resolved. If companies are not ready to commit to a hard quantitative key performance indicator (KPI), they can commit to greater green governance by not only appointing chief sustainability officers but giving them greater authority in the organization, including direct communication with the board of directors, or even board representation.</p><p>Turning to external responses, corporate pledges can also be strengthened through greater incentives to meet the declared targets. A first step in providing incentives is to set clear interim targets that can be measured and observed. Commitments with far-away targets may be seen by the current management of the company as something that can be left to future management teams to deal with. However, if management must meet an interim target before its tenure is over, and if the management team's compensation is tied to whether the company has met the target or not, the team is more likely to avoid falling behind.</p><p>There are multiple ways of tying compensation to meeting decarbonization targets. Responding to calls from investors to connect pay to ESG, a growing number of companies have explicitly linked executive compensation to meeting carbon targets. However, a recent study by PwC of ESG-linked pay at top European companies has found that most of these compensation packages fall short on multiple dimensions.20 The component of pay that is sensitive to meeting carbon KPIs is either too small to set up a meaningful financial incentive to perform, or the targets are not sufficiently clear or in line with long-term carbon reduction targets. The study concludes that “this link often exists but is rarely drawn out in a way that enables investors to compare the consistency of pay goals with stated medium to long-term commitments.” Second-generation ESG-linked pay packages should thus provide more “skin in the game” for management in meeting declared decarbonization targets.</p><p>Financial markets may also play a more important disciplining role by pricing in a greater carbon P/E discount for companies that miss their decarbonization target. In a study published in this journal a year ago,22 three of us presented new evidence that companies with higher carbon emissions trade at lower P/E ratios, other things equal. And in a more recent study,23 we further showed that companies that voluntarily disclose their carbon emissions trade at higher P/E ratios than comparable companies that do not disclose. However, as we noted above, there tends to be no significant impact on companies’ P/E ratio associated with either pledges to decarbonize or falling behind on pledged commitments. This lack of market response could reflect the inherent uncertainty around first-generation commitments and companies’ ability (or determination) to implement their pledges. In the case of second-generation commitments, financial markets may prove less forgiving of companies that are falling behind.</p><p>As decarbonization becomes more urgent and the remaining carbon budget consistent with a 1.5°C or 2°C limit dwindles, analysts may increasingly look at decarbonization targets the same way they scrutinize earnings targets, and financial markets may punish companies for failing to meet their decarbonization targets the way they punish companies for failing to meet earnings targets. Another capital market response that is beginning to emerge is the use of ESG exclusionary filters that are based on decarbonization pledges. As investors increasingly pay attention to corporate decarbonization pledges, they may respond more swiftly and exclude companies that are significantly falling behind on their commitments.</p><p>In May 2022, the SEC proposed new rules on <i>The Enhancement and Standardization of Climate-Related Disclosures for Investors</i>.24 Under the regulatory proposal, companies could be required to disclose not only their direct emissions in a given year but also future decarbonization pledges, even those tied to Scope 3 emissions if the company “has set a GHG emissions reduction target or goal that includes its Scope 3 emissions.”25 It is far from certain how and whether these rules will be implemented, but if they are, carbon pledges are likely to become more material and to receive greater scrutiny from investors. This greater scrutiny is also likely to elicit a more significant market response to news about missing a decarbonization target. Another possible response, of course, is that companies may become more reluctant to make pledges that are more constraining under these new rules.</p><p>The increasing number of major companies signing up with CDP and SBTi recently signals a burgeoning interest among corporate management in voluntary corporate emission goals. As more and more companies are making pledges to decarbonize their operations, however, there have been rising warnings that not all these commitments are likely to be made good on. Recent cases of companies trimming down their carbon reduction commitments have exacerbated these concerns.</p><p>Our analysis of corporate carbon commitments suggests that what we have witnessed over the past few years is the birth of a first generation of commitments, where the emphasis has been more on signaling than on mapping out detailed plans on how to decarbonize. To be sure, there is still little detail on concrete steps and not much contingency planning. In some respects, this first generation of carbon pledges is similar to the early phases of the creation of the green bond market. As this market has grown, more rigorous standards have been introduced and greater attention has been put on incentives, which has led Enel and other pioneering companies to switch from green bond issuance to sustainability-linked bond issuance that have better aligned incentives to meet stated decarbonization goals.</p>","PeriodicalId":46789,"journal":{"name":"Journal of Applied Corporate Finance","volume":"35 2","pages":"26-34"},"PeriodicalIF":1.4000,"publicationDate":"2023-06-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12560","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Corporate Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12560","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

The 2015 Paris Agreement represented the first multilateral agreement to acknowledge and support efforts by so-called non-state actors, including corporations, to cut their greenhouse gas emissions. Moreover, the goals and structure of the Paris Agreement—focused on limiting warming to well below 2°C relative to pre-industrial levels and allowing for national governments to set voluntary emission goals—have informed the setting and adoption of voluntary corporate commitments. Some corporations have taken on “Paris-aligned” emission commitments, indicating that they would deliver emission reductions consistent with the temperature objective of the 2015 agreement. With the increasing adoption of mid-century net-zero emission goals by national governments, some corporates have likewise adopted their own net-zero emission commitments.

Before the Paris Agreement few companies had made commitments to reduce their carbon emissions. Most of them did so through the Carbon Disclosure Project (CDP), which benefited from the momentum generated by the Paris agreement to substantially expand the number of companies that would make decarbonization pledges and voluntarily disclose their carbon emissions. Later, CDP along with the United Nations Global Compact, the World Resources Institute (WRI), and the Worldwide Fund for Nature, founded the Science-Based Target initiative (SBTi) to engage with companies to implement carbon reduction commitments that are aligned with the Paris agreement and the goal of limiting global overheating to less than 2°C above pre-industrial levels. As Mark Carney had predicted in the run-up to the COP 26 in 2021, “More and more companies—and it will be a tsunami by Glasgow—will have net zero emissions plans.”1 As of this writing, SBTi can boast that “more than 4,000 businesses around the world are already working with the Science-Based Targets initiative.”2

Other major decarbonization drives in the wake of the Paris agreement have emerged in the financial sector, with the launch of the Task Force on Climate-Related Financial Disclosures in 2015, Climate Action 100+ in 2017, the inauguration of the Asset Owners Net-Zero Alliance in 2019 together with the Net Zero Asset Managers Initiative in 2020, and, the culmination of this wave of initiatives, the creation of the Glasgow Financial Alliance for Net Zero by Mark Carney at the COP 26 in April 2021. In parallel, the Network for Greening the Financial System (now comprising 121 central banks and financial supervisory authorities) was set up in 2017, providing guidance on net zero compatible decarbonization pathways. In short, the Paris agreement has ushered in a new era of decarbonization commitments.

An important aspect of emission reduction commitments is the extent to which they specify interim targets. Commitments are less credible when they specify distant targets and are vague about the pathway toward attaining the target. Businesses cannot decarbonize overnight. Eliminating GHG emissions is inevitably a gradual process, which involves replacing old operating facilities as they depreciate with new facilities powered by renewable energy. The cost of decarbonization can be reduced if this replacement of old with new plants and equipment is spread out over time—hence the net zero targets that are decades away. There is considerable uncertainty over such a long period, which could produce new technological breakthroughs, new green regulations, or new pandemics and wars that disrupt energy supplies. Thus, companies need flexibility and cannot tie themselves to a pathway that is too rigid. On the other hand, the risk of missing the ultimate target is greater if companies do not specify interim milestones.

Many companies that do make commitments to decarbonize do specify such milestones. For these companies we can determine whether they are on track or are falling behind. We also explore how the market reacts when a company falls behind or abandons its commitments mid-course. When we do so, we find little evidence of a backlash.

A case in point is the February 2023 announcement by BP that it would delay its near-term commitment to reduce oil and gas production, changing its 2030 target from a 40% to just a 25% reduction. Despite considerable criticism, BP has so far suffered no negative effects from this move. On the contrary, its stock price increased significantly following its announcement of the change in plans (though likely attributable to concurrently announced soaring oil profits).

To illustrate the implications of the Paris approach through voluntary corporate actions, we frame our analysis through three conceptual interrogations. First, in section “Incentives for Corporations to Adopt Voluntary Commitments” we examine what induces companies to make decarbonization pledges on a voluntary basis. We also study how corporate pledges take account of uncertainty and changing circumstances. In section “What are corporations pledging to do, and how are they”, we show how companies have managed to fulfill their pledges so far, and the extent to which their decarbonization trajectories are consistent with their ultimate targets. In section “The broader commitments landscape: countries, universities”, we look beyond corporate commitments and study the role of commitments by countries, universities, and asset managers. In section “How to handle failing commitments?”, we discuss various ways in which companies and regulators could adjust to the possibility of failing commitments.

The conventional wisdom about corporations and the environment has long reflected two major themes: (1) Milton Friedman's 1970 proclamation that the “the social responsibility of business is to increase profits”; and (2) the imposition by environmental regulations of significant costs on business.3 In recent years, however, corporations have pursued various forms of self-regulation, including the adoption of voluntary greenhouse gas emission commitments. In contrast to the conventional wisdom, corporate management may have a more nuanced take on the incentives and rationale for committing to emission-reduction goals. With growing attention to addressing the risks posed by a changing climate among consumers, investors, workers, and other stakeholders, corporate managements may find it in their interest to cut their greenhouse gas emissions.

With a growing interest among consumers in the environmental characteristics of the goods and services they purchase, a corporation may find that “signaling” its efforts to address climate change may facilitate product differentiation and increase market share and/or mark-ups. Especially in retail-facing environments, corporates have found value in enhancing their brand and image through public efforts to demonstrate their social responsibility.4 The challenge with such a strategy of drawing attention to emission-cutting efforts lies in the prospect that some stakeholders, both those in the investment community and civil society, may accuse the corporate of greenwashing—that is, misleading the public about the environmental impact of the corporation.

Corporations operate under a patchwork of energy, climate, and tax policies that may influence the adoption of an emission commitment. In some contexts, a corporation may already face significant regulatory requirements, such as those operating under the EU Emission Trading System or in California, associated with its own cap-and-trade program, as well as renewable and low-carbon requirements in its power and petroleum refining sectors. The incremental effort—and hence opportunity cost of investment—would be lower for such corporations covered by regulations to attain any given emission goal than for other corporations operating beyond the scope of regulatory mandates. To the extent that regulations have targeted relatively more expensive ways for a corporate to reduce emissions, there may be residual low-cost emission reductions that could easily enable the corporate to meet emission targets that are more ambitious than its regulatory requirements. Moreover, the experience and information gained from undertaking investment necessary to comply with regulatory mandates may facilitate actions to cut emissions by reducing the uncertainty associated with such future investment's returns.

In a similar manner, corporations operating in jurisdictions with generous subsidies for investing in clean energy technologies—such as tax credits for installing solar panels, loan guarantees for investing in novel emission capture equipment, and grants for improving the energy efficiency of its facilities—may find the incremental costs of cutting emissions to be low and, indeed, the marginal abatement cost function within the firm may be considerably flatter with public subsidies. For example, the Inflation Reduction Act of 2022 makes available an array of clean energy investment tax credits—in the power, transportation, manufacturing, and buildings sectors—that cover 30% of investment costs. In addition to subsidies for reducing emissions within the corporate footprint, some companies have focused on the potential for low-cost emission offset projects beyond the corporate footprint as a way to reduce their costs of meeting a net-emissions target.5

The interests and preferences of two sets of key stakeholders for corporate managers—the investors they answer to and the workers they recruit and manage—could also inform the decision-making calculus over the adoption of an emission target. Investors with green preferences as well as those focused on aligning long-term returns to long-term liabilities (such as pension plan asset managers) may have a strong interest in ensuring that the corporates they invest in have developed credible strategies for managing decarbonization transition risk. With growing shareholder activism and the use of shareholder resolutions to drive green changes in management practices, corporate managers may pursue voluntary emission targets as a means to address and manage such pressures.6 Moreover, with growing interest in climate change among younger generations, managers may find that a well-developed climate change program—perhaps as a part of a broader corporate social responsibility agenda—helps facilitate the recruitment and retention of high-quality, new workers in the workforce.

Finally, a corporate may adopt voluntary emission targets and an associated emission-reduction plan to influence future government policy and regulation. In some cases, aggressive and credible corporate emission cuts could preempt regulation. In other cases, such aggressive efforts could shape the future of regulation and provide a corporate with greater voice in designing the policy, which may enable it to acquire value or impose costs on laggard competitors from policy design. A corporate may also signal to regulators a feasible path for policy ambition through its own goals and its use of an internal carbon price. Recent scholarship illustrates how corporates headquartered in jurisdictions with carbon pricing are more likely to employ an internal carbon price in their operations and strategy development, and that such internal carbon prices are higher in those regions with higher carbon prices under the jurisdiction's climate policies.7

While these are possible explanations for why a corporate adopts a voluntary emission commitment, quantitative analysis can inform our understanding of whether doing so increases the value to the corporate. In an article by several of us in this journal in 2022, we presented the results from multivariate regression models we used to isolate the effect of commitments on price-to-earnings ratios, building on previous work that quantified the relationship between Scope 1 carbon emissions and price-to-earnings ratios (producing firm-level carbon valuation discount rates).8 Our analysis finds that participating in a CDP initiative can offset, on average, 15% of the firm's carbon valuation discount, though the lack of statistical significance suggests that this result is not robust (the same holds for SBTi pledges). Chosen parameters for pledges (length and targets) have no real impact on firm valuation either. Sector results also display insignificant valuation effects, with the one outlier being financials: Financial companies making pledges get a further valuation discount, possibly attributable to costs associated with the transition to net-zero financed emissions.

In theory, there are two opposing effects that underlie the financial decision-making associate with corporate pledges to meet emissions targets. Making such pledges could signal higher near-term financial costs, since decarbonizing operations or purchasing carbon offsets is likely to be costly. But to the extent such outlays work to limit the pledging companies’ exposure to transition risk, the announcement of such pledges could be seen by investors as increasing value, at least in the medium and longer run. The lack of any notable valuation changes from such commitments could be a consequence of these effects offsetting one other. More likely, our findings around the differential between actual decarbonization rates and pledged abatement rates, and given the increased public scrutiny of greenwashing, suggest investors’ skepticism about the genuineness of commitments to future emission reductions. Investors may interpret pledges, at the present, less as serious commitments and more as public relations moves. Thus, they may be waiting to view commitments as financially material until after greater progress in meeting pledges has been demonstrated.

A common step for companies before making a decarbonization pledge is to report carbon emissions. A remarkable first finding that emerges from our analysis is that a steadily growing fraction of Russell 3000 companies, which are responsible for the largest share of corporate carbon emissions, has chosen to report their GHG emissions from 2010 to 2020. By now around a quarter of large cap companies disclose their emissions. Along with a rising rate of carbon disclosures, corporations have increasingly made decarbonization pledges, with the number of CDP pledges—the earliest platform set up to encourage corporations to make decarbonization pledges—more than doubling over this period. CDP along with the UN Global Compact, the Worldwide Fund for Nature (WWF), and the WRI, later launched the SBTi, which provides further guidance to companies in aligning their pledges with net zero targets. SBTi pledges are more rigorous, and to date a much smaller fraction of companies have made SBTi commitments (4% compared to 15% for CDP pledges). Breaking carbon reduction pledges down by sector, we find that the highest fraction are companies in the utilities sector (46%), followed by those in consumer staples (35%), and materials (31%).

We find that most corporate pledges have a short horizon, with close to 50% of pledges specifying a target date less than five years away. To be sure, some pledges have a 2050 target, but these represent only 6% of the corporate pledges in our sample. As for the pledged rates of carbon reduction, we found that they are widely dispersed, with 70% of pledges committing to a total reduction of emissions that is less than 40% of base year emissions. Only 7% of companies in our sample have pledged to completely decarbonize.

It is perfectly possible, even plausible, that if all the companies that have made pledges completely realized their commitments, the total carbon emission reduction would fall short of what is necessary to avoid overheating by more than 1.5°C or 2°C, for the simple reason that many companies with very high levels of carbon emissions have as yet failed to make any pledges to decarbonize. Also, it is to be expected that when (short-run) economic incentives do not line up, even willing companies would not go the distance and make pledges that could prove to be very costly.

To assess the seriousness of corporate commitments to making good on their pledges, we compare the effective annual abatement rates consistent with their pledges (under a linear reduction rate) to their actual decarbonization rates after they have made their commitments public. We note that this is a conservative assumption given that energy-economic models of countries/regions for national emission goals (or more commonly, global temperature/atmospheric concentration stabilization goals) tend to show greater than linear reductions in the near term (for easier-to-abate emissions) and less than linear reductions in the longer term (for harder-to-abate emissions). Based on 10-year annual decarbonization averages, we observe that 72% of companies have been falling behind and will need to accelerate their emission reductions going forward to be able to meet their targets. This fraction of laggards is marginally lower when we look at decarbonization rates over a more recent (three-year average) time frame. Indeed, we find that 56% of pledging companies are underperforming over that span relative to a trajectory toward their stated decarbonization targets.

It is important to find out what causes companies to fall behind on their commitments. Is it largely because of an unexpected energy supply shock, such as the Russian invasion of Ukraine, or because companies have overpromised? One way to find out is to look at the distribution of commitment failures across the companies that have made commitments. If companies are falling behind because of an aggregate shock like the war on Ukraine, then we would expect to see similar commitment failures across all companies. But if a large number of companies are falling behind because they have overpromised, we would not expect to see a uniform commitment failure across all companies. As above, we define a commitment failure as the positive difference between the pledging companies’ percentage changes in Scope 1 emissions relative to annual abatement rates implied by CDP targets with longest horizon.

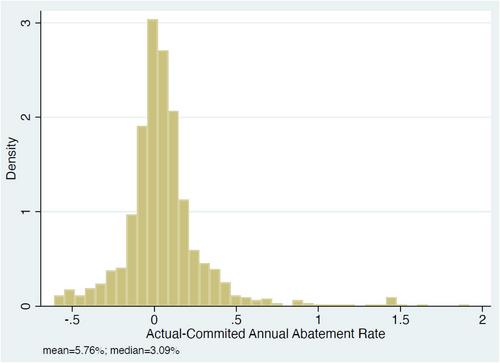

We begin with the tabulation of the unconditional values of this failure variable for the entire sample of firms making CDP commitments. Our findings, as summarized in Figure 1, show that the average firm in our sample is failing to meet its CDP commitment by 5.8 percentage points. The median shortfall is 3.1 percentage points, which is a consequence of the disproportionately large failures of a small number of companies (as reflected in the right skewness in the sample).

Why are Some Companies Failing on their Commitments? These results do not tell us much about the underlying sources of failures, but they do suggest that for many companies making overly optimistic promises has been an issue. Do failures happen more in certain industries, companies with certain characteristics, or in certain time periods? These are the questions we aim to answer next.

First, we define “failing” commitments. Generally, a failing commitment could refer to a corporate missing a terminal target, missing an intermediary target, reneging on a pledge, or falling behind (over some time span) on a committed decarbonization trajectory. In our analytical treatment, we define the failure measure as the differential between pledged emissions reduction (under a linear reduction rate) and actual emissions reduction from 2010 to 2020. The sample is companies in the Russell 3000. Table 1 displays the summary statistics for pledging companies from the cross-section of 11 industrial sectors in our sample. We present mean, median, 25th and 75th percentiles, as well as standard deviations of the failure measures for each sector.

As reported in the table, we find, first of all, that the average pledging company fails to meet its CDP target across all industry sectors, with the largest deviations being observed in Communication Services, Materials, and Information Technology. The smallest failures are in the Utilities, Industrials, and Financials sectors. When we focus on median values of commitment failures, we note that the values are smaller, albeit still positive for 10 out of 11 sectors. The notable exception is the Utilities sector.

Second, we find significant dispersion in failures within sectors, as indicated by the large values of the standard deviations of the failure measure. Given that failures do not seem to cluster within individual sectors, it seems that the more likely reasons for failure can be traced to either broad macro shocks (like those associated with the Ukraine War) or differences in individual company circumstances within a sector. We attempt to provide more evidence on the former by looking at the distribution of failures over time.

As can be seen in Table 2, we observe a reasonably consistent distribution of failures over time, though with some interesting patterns. First, failures have been generally going down over time, with the notable exceptions of 2017 and 2018, when failure rates actually went up. This general downtrend could explain why more firms were joining CDP. On the other hand, some of the increases in failures could be partly explained by adverse selection, in the sense that companies that join later are less able to meet their commitments. Second, the global lockdown in 2020 clearly contributed to a reduction in the magnitude of failures, in turn attributable to the significant drop in emissions from the economic slowdown caused by COVID lockdowns. Third, within each year we observe a significant variation in failures, which suggests that at least some of the variation in failures is likely idiosyncratic in nature.

In the next set of results, we explore some of the firm-specific differences across companies. We consider a number of corporate characteristics: the maximum year for which companies make commitments, market capitalization, ROE, level of Scope 1 emissions, Scope 3 upstream emissions, sales growth, and book to market equity. In Table 3 we report means, medians, and standard deviations of failure variables for companies whose values of each characteristic are below median and above median for the given characteristic in our sample.

Among our most interesting observations, we start by noting that pledging companies with longer-horizon targets on average experience lower failure margins than companies with shorter target dates. This may seem counterintuitive since companies with longer-term pledges might be assumed to face greater uncertainty, and companies making more distant commitments may do so to delay their decarbonization. But this finding could also instead suggest that more gradual decarbonization pathways are more realistic to achieve. Second, we do not find significant differences across companies with different market capitalizations, profitability, and B/M ratios. What we do find, however, is that companies with higher emissions, especially Scope 3 upstream emissions, are more likely to fail by bigger margins. This result is consistent with our earlier finding that best-in-class companies are both more likely to commit and to set ambitious targets.9

Finally, we observe that the degree of commitment failure is a fairly direct function of sales growth. Companies with higher sales growth are more likely to fail their commitments. This result suggests that when companies experience an unexpectedly large sales growth they find it difficult to meet their decarbonization promises, or at the very least that companies that set targets without properly accounting for their future growth potential are likely to fail to deliver on their promises. But such considerations notwithstanding, it is notable that within each sorted group we observe significant differences among companies, as reflected in the large standard deviations—which in turn suggest that the reasons behind the failures are not simple and likely reflect the complexity of multi-dimensional business models.10

But if companies have been falling behind in carrying out their commitments, other non-corporate entities, nations, asset managers, and universities have also faced challenges in making adequate commitments and in implementing them. In this section, we provide a sketch of this broader context to make clear that the challenges that corporations have faced are by no means unique to them.

By the end of 2022, around 140 countries representing over 91% of global CO2 emissions have made NZ pledges.11 The target year is most often 2050, but some countries like Sweden have a more ambitious target year (2045) and others like China a less ambitious target year (2060). A few countries like the United Kingdom have even enshrined their NZ commitment into law. Such ambitious goals require largescale, near-term emission-cutting programs, but few countries have undertaken action consistent with their net-zero goals. Under the Paris Agreement, countries have issued emission pledges for 2030. If all countries implemented these pledges, global emissions would fall by a mere 11% through the end of this decade.12 In its annual Emissions Gap Report of 2022, the UN Environment Programme finds that countries are falling behind on their 2030 goals, which they note are insufficient to keep the world on track to limiting warming to 2°C or less.13 The Environmental Performance Index (EPI) published every 2 years by scholars from Yale and Columbia, deems that only Denmark, Great Britain, Botswana, and Namibia are on track to achieving net-zero greenhouse gas (GHG) emissions by 2050.

Academic institutions, important voices that could drive climate change mitigation, have struggled in implementing their decarbonization pledges. Before the recent wave of corporates voluntarily adopting emission commitments, higher education institutions adopted ambitious carbon emission goals. With this head start, about a dozen institutions of higher learning have announced that they have reached net-zero emissions as of 2020.14 These efforts illustrate how such institutions framed their net-zero goals, especially in terms of the scope of emissions coverage, and what actions they undertook to deliver on these goals.

These forward-leaning higher education institutions set net-zero emission goals that covered the emissions within their institutional footprint (Scope 1), the carbon emissions associated with their purchase of electricity (Scope 2), and a limited accounting of their supply chain (Scope 3) emissions, primarily institution-funded airline travel and employee commuting. With increased interest in both upstream and downstream emissions associated with corporates, this narrow Scope 3 focus provides limited insights for current policy debates but does highlight what are fundamental data challenges in adopting an emissions commitment that includes emissions beyond the boundary of the firm.

A 2021 analysis by several Harvard Scholars shows that in practice, less than 20% of the emission reductions associated with reaching net-zero occurred in higher education institutions’ Scope 1, Scope 2, and Scope 3 emissions footprints.15 Several institutions relied extensively on biological sequestration on college-owned land, although doing so effectively assumes that, in the absence of the net-zero policy, the colleges would have clearcut all of their lands. More than 60% of the emission reductions necessary to attain net-zero occurred through the purchase of emission offsets and unbundled renewable energy credits. The offsets typically came from landfill methane and forestry projects, but the emission additionality of many of these types of projects have been challenged in recent years.16 The purchase of unbundled renewable energy credits likely do little to increase renewable power investment and generation, and instead simply represents a financial transfer to existing renewable power generators. In most cases, the improving carbon intensity of the local generation mix, reflecting decisions beyond those of university administrators, enabled the institutions to make progress on their Scope 2 emissions.

The Harvard scholars conclude that the considerable progress made by these institutions provides important lessons for the next steps in voluntary decarbonization.17 They note, with reservation, that the extensive reliance on offsets and unbundled renewable energy credits do not serve as a model that can be replicated more broadly and still deliver on economy-wide net-zero goals.

In addition to corporates and universities, an increasing number of investors have made pledges to reduce the emissions associated with their portfolios. The Net Zero Asset Management Alliance (NZAM), which was launched in 2020, is one of the most ambitious initiatives to promote net-zero goals. Despite its rapid growth in membership and economic significance, however, the initiative has also faced significant backlash recently from critics in the finance industry and from politicians, which has somewhat undermined its future success. An example of such a backlash is the recent decision by Vanguard to withdraw publicly from its commitment to NZAM.

In December 2022, Vanguard announced that it was withdrawing from the Net Zero Asset Managers initiative amid questions raised by the US Senate Committee on Banking, Housing and Urban Affairs over whether it is appropriate for passive investment managers to engage with issuers on “stewardship” issues such as climate change. The suggestion was made that passive index investors such as Vanguard may not have a mandate to engage with their portfolio companies toward a goal of achieving net zero emissions.

Given the significance of Vanguard as one of the leading asset managers, the concern is that such developments could call into question the long-term viability of the various asset management climate coalitions.

We first examine firms that have “failed” to make a commitment in the first place. According to the most recent evidence from MSCI this year, the proportion of listed companies that have self-declared net-zero targets is 17%.18 While ostensibly low, this proportion has actually risen from 10% in 2022 to 17% in 2023. But this still means that 83% of listed companies do not have any net-zero targets. Admittedly, the proportion of companies with some decarbonization targets has risen to 44% in 2023. Yet, this still means that over half of all listed companies have failed to make any commitment at all. And there is even less transparency about commitments and emission reduction efforts among privately held companies.

This broad-brush assessment may paint an excessively pessimistic picture, for some companies do not make any pledges because their emissions are low anyway. To gain more perspective on this apparent lack of corporate commitments, it is instructive to look at the breakdown by industry. The same report tells us that the proportion of self-declared net-zero targets is highest in the utilities sector, with 38% of companies, second highest in the energy sector, with 28%, and third highest in the consumer staples and materials industries, with 21%. This compares with only 6% of companies making such pledges in the health care sector.

Another instructive breakdown is between 1.5°C aligned and misaligned companies based on their self-declared commitments. Roughly 19% of companies are deemed to be 1.5°C aligned by MSCI in 2023, but the same proportion is deemed to be strongly misaligned, and 32% of companies are deemed to be 2°C aligned and 31% of companies are 2°C misaligned.

The other way in which commitments can fail—often the exclusive focus of greenwashing critics—is when implementation is falling behind. How can companies, which after all are declaring their concerns about climate change and are stepping up to the plate, avoid falling behind? How can they avoid missing intermediary targets, or worse, backtrack on their pledges at a later date? It is helpful to break down the answers to these questions into two broad categories of responses, internal, at least at the time when it decides to make a pledge, and external.

Regarding internal responses, one often hears that companies are facing a lot of uncertainty about their future ability to abide by their pledges, especially if their targets are far into the future. Firms do not have full control over their emissions. This is obviously the case for Scope 2 and 3 emissions, but also for Scope 1 emissions. Firms may have a plan to replace a fossil fuel energy source with a renewable one but may find unforeseen obstacles along the way, such as supply chain disruptions or delays in necessary overhauls of the electricity grid.

How should companies respond to these hazards? Many first-generation corporate pledges have essentially side-stepped these issues and, hoping for the best, have made commitments without a careful evaluation of their ability to meet their pledges in all circumstances. Given our findings above, a large fraction of companies that have made commitments clearly did not see their (in hindsight) optimistic scenarios materialize.

How can companies avoid ending up in a similar situation in the future? One possible answer is to stress-test their commitments before announcing them. Just as bank balance sheets are stress- tested to see if they can withstand an adverse non-performing loans shock, commitments could be stress-tested against shocks that could affect the company's future emissions. Would the company be able to still meet its targets in the event of an adverse shock? By stress-testing their planned commitments, companies can determine what cushion they have in adjusting their emissions following an adverse shock, to avoid falling behind.

Another response, of course, could be to accept that the company may fail to meet its pledges under adverse circumstances. Such a response, however, may call for a new generation of pledges that are state-contingent. The company could gain more credibility if it were more upfront about the circumstances in which it can and cannot meet its pledges. Or, if it is difficult to anticipate and describe these circumstances, the company could include force majeure clauses in its pledges that clearly state that it may not always be able to meet its pledges and that describe what the company will do with respect to its decarbonization commitments under such circumstances.