Jesús Fernández-Villaverde, Samuel Hurtado, Galo Nuño

{"title":"Corrigendum: Financial Frictions and the Wealth Distribution","authors":"Jesús Fernández-Villaverde, Samuel Hurtado, Galo Nuño","doi":"10.3982/ECTA22259","DOIUrl":null,"url":null,"abstract":"<p><span>Part of the focus</span> of our paper “Financial Frictions and the Wealth Distribution” was the discussion of the presence of two stochastic steady states (SSSs): a high-leverage (HL-SSS) and a low-leverage one (LL-SSS).</p><p>We have found that if the number of points in the grid of aggregate debt <i>B</i> increases, the HL-SSS disappears for a range of calibrations close to the baseline parameterization. We have not found any evidence regarding the presence of the HL-SSS for other parameterizations. Furthermore, the degree of state dependency on households' impulse response functions (IRFs) is smaller. We must emphasize that this is a purely numerical issue: the neural network algorithm that we propose is correct and the code that we posted online is bug-free. Unfortunately, we did not select enough grid points for <i>B</i> (a numerical hyperparameter that controls the accuracy of the results) to yield stable numerical results. Nonetheless, what we see as the two main contributions of our paper, namely, the introduction of a new neural network algorithm to solve heterogeneous agent models with aggregate shocks and the nonlinear estimation of continuous-time models, remain unchanged.</p><p>Furthermore, the model of financial frictions with heterogeneity is still quite nonlinear, since:</p><p>Figure 1 shows, in the phase diagram, the impact of increasing the number of grid points in the dimension of aggregate debt <i>B</i>. The top left panel replicates Figure 5 in our original paper, where we used four grid points and a forward scheme. In the top right panel, we switch from a forward scheme to an upwind scheme to ensure the stability of our procedure (otherwise, it is numerically difficult to get the algorithm to converge with more than four grid points). In both top panels, we see two SSSs: the HL-SSS and the LL-SSS. In particular, the right top panel shows that switching to an upwind scheme is not central to our argument.</p><p>In the left bottom panel, we increase the number of grid points to eight (now with the upwind scheme). We can see now that the HL-SSS disappears, and only the LL-SSS remains. The bottom right panel checks the case with 16 grid points for completeness. We have tried alternative calibrations around the baseline one, and this result seems to hold for eight and 16 grid points.</p><p>Notice how the PLM for debt displays a nonlinear shape, with a change in concavity happening in the region between the LL-SSS and the DSS. Consequently, despite only crossing once at the LL-SSS, the PLMs for constant equity and debt run almost parallel and very close, as in the version with three crosses in our paper. This explains why the ergodic distribution will occupy a similar region of the state space.</p><p>To illustrate this point, Figure 2 displays the ergodic distribution generated with 16 grid points. It covers a region similar to the one plotted in Figure 9 in the paper. The main difference is that, instead of peaking around the HL-SSS, it now peaks around the LL-SSS. This reinforces the nonlinearity of the model, as the LL-SSS is further away from the DSS.</p><p>Figure 3 shows that the wealth distributions in the DSS and SSS are similar to those in the paper, displaying more wealth inequality in the region around the DSS (and the HL-SSS) than around the LL-SSS. Figure 4 displays the IRFs: they are still state-dependent for reasons similar to those stated in the paper.</p><p>Finally, Figure 5 shows the histogram of forecasting errors at a one-month horizon (the time step in the simulation), with a solid line representing the errors from our algorithm and the dashed line the errors from a Krusell–Smith algorithm. The forecasting errors in our model are clustered around zero, with a mode roughly equal to zero. The Krusell–Smith algorithm produces forecasting errors that are more volatile, skewed to the right, and without a mode at zero. We also tried alternative specifications for the Krusell–Smith algorithm, which all produce worse forecasting errors. This result is the consequence of the nonlinear PLM, better captured by the neural network than by (log-)linear specifications.</p>","PeriodicalId":50556,"journal":{"name":"Econometrica","volume":"93 4","pages":"1491-1496"},"PeriodicalIF":7.1000,"publicationDate":"2025-07-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.3982/ECTA22259","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Econometrica","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.3982/ECTA22259","RegionNum":1,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

Part of the focus of our paper “Financial Frictions and the Wealth Distribution” was the discussion of the presence of two stochastic steady states (SSSs): a high-leverage (HL-SSS) and a low-leverage one (LL-SSS).

We have found that if the number of points in the grid of aggregate debt B increases, the HL-SSS disappears for a range of calibrations close to the baseline parameterization. We have not found any evidence regarding the presence of the HL-SSS for other parameterizations. Furthermore, the degree of state dependency on households' impulse response functions (IRFs) is smaller. We must emphasize that this is a purely numerical issue: the neural network algorithm that we propose is correct and the code that we posted online is bug-free. Unfortunately, we did not select enough grid points for B (a numerical hyperparameter that controls the accuracy of the results) to yield stable numerical results. Nonetheless, what we see as the two main contributions of our paper, namely, the introduction of a new neural network algorithm to solve heterogeneous agent models with aggregate shocks and the nonlinear estimation of continuous-time models, remain unchanged.

Furthermore, the model of financial frictions with heterogeneity is still quite nonlinear, since:

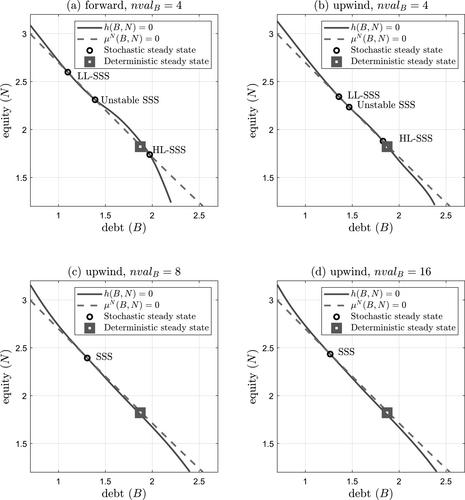

Figure 1 shows, in the phase diagram, the impact of increasing the number of grid points in the dimension of aggregate debt B. The top left panel replicates Figure 5 in our original paper, where we used four grid points and a forward scheme. In the top right panel, we switch from a forward scheme to an upwind scheme to ensure the stability of our procedure (otherwise, it is numerically difficult to get the algorithm to converge with more than four grid points). In both top panels, we see two SSSs: the HL-SSS and the LL-SSS. In particular, the right top panel shows that switching to an upwind scheme is not central to our argument.

In the left bottom panel, we increase the number of grid points to eight (now with the upwind scheme). We can see now that the HL-SSS disappears, and only the LL-SSS remains. The bottom right panel checks the case with 16 grid points for completeness. We have tried alternative calibrations around the baseline one, and this result seems to hold for eight and 16 grid points.

Notice how the PLM for debt displays a nonlinear shape, with a change in concavity happening in the region between the LL-SSS and the DSS. Consequently, despite only crossing once at the LL-SSS, the PLMs for constant equity and debt run almost parallel and very close, as in the version with three crosses in our paper. This explains why the ergodic distribution will occupy a similar region of the state space.

To illustrate this point, Figure 2 displays the ergodic distribution generated with 16 grid points. It covers a region similar to the one plotted in Figure 9 in the paper. The main difference is that, instead of peaking around the HL-SSS, it now peaks around the LL-SSS. This reinforces the nonlinearity of the model, as the LL-SSS is further away from the DSS.

Figure 3 shows that the wealth distributions in the DSS and SSS are similar to those in the paper, displaying more wealth inequality in the region around the DSS (and the HL-SSS) than around the LL-SSS. Figure 4 displays the IRFs: they are still state-dependent for reasons similar to those stated in the paper.

Finally, Figure 5 shows the histogram of forecasting errors at a one-month horizon (the time step in the simulation), with a solid line representing the errors from our algorithm and the dashed line the errors from a Krusell–Smith algorithm. The forecasting errors in our model are clustered around zero, with a mode roughly equal to zero. The Krusell–Smith algorithm produces forecasting errors that are more volatile, skewed to the right, and without a mode at zero. We also tried alternative specifications for the Krusell–Smith algorithm, which all produce worse forecasting errors. This result is the consequence of the nonlinear PLM, better captured by the neural network than by (log-)linear specifications.

期刊介绍:

Econometrica publishes original articles in all branches of economics - theoretical and empirical, abstract and applied, providing wide-ranging coverage across the subject area. It promotes studies that aim at the unification of the theoretical-quantitative and the empirical-quantitative approach to economic problems and that are penetrated by constructive and rigorous thinking. It explores a unique range of topics each year - from the frontier of theoretical developments in many new and important areas, to research on current and applied economic problems, to methodologically innovative, theoretical and applied studies in econometrics.

Econometrica maintains a long tradition that submitted articles are refereed carefully and that detailed and thoughtful referee reports are provided to the author as an aid to scientific research, thus ensuring the high calibre of papers found in Econometrica. An international board of editors, together with the referees it has selected, has succeeded in substantially reducing editorial turnaround time, thereby encouraging submissions of the highest quality.

We strongly encourage recent Ph. D. graduates to submit their work to Econometrica. Our policy is to take into account the fact that recent graduates are less experienced in the process of writing and submitting papers.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: