{"title":"The impact of yield curve control under different regimes on Japanese Government bonds and swap markets in the super long term","authors":"Takayasu Ito","doi":"10.1002/jcaf.22739","DOIUrl":null,"url":null,"abstract":"<p>Japanese Government Bonds (JGBs) and swap markets in the maturities of 10, 15, 20, and 30 years increased in volatility volatilities after the Bank of Japan (BOJ) expanded the upper limit of yield curve control (YCC) from .2% to .25% on March 19, 2021. The entire sample period is divided in half. Market segmentation is observed between JGB and swap markets in the first half of the YCC. They are integrated except for the maturity of 10 years in the second half of the YCC. In other words, arbitrage works between two markets. After the BOJ expanded the upper limit of the YCC to .25%, structural change occurred in the super long term in relation to JGB and swap markets. The decision by the BOJ has contributed to the normalization of the market function because there has been more room for the benchmark JGB yield of 10 years to move more actively.</p>","PeriodicalId":44561,"journal":{"name":"Journal of Corporate Accounting and Finance","volume":"36 1","pages":"55-60"},"PeriodicalIF":1.2000,"publicationDate":"2024-06-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/jcaf.22739","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Corporate Accounting and Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/jcaf.22739","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

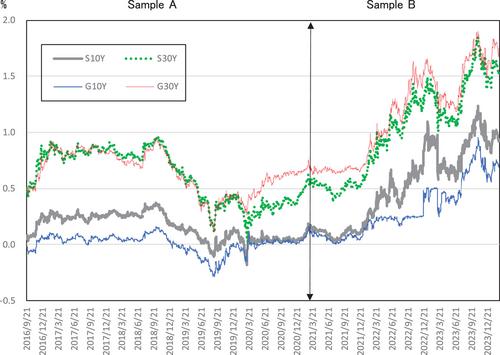

Abstract

Japanese Government Bonds (JGBs) and swap markets in the maturities of 10, 15, 20, and 30 years increased in volatility volatilities after the Bank of Japan (BOJ) expanded the upper limit of yield curve control (YCC) from .2% to .25% on March 19, 2021. The entire sample period is divided in half. Market segmentation is observed between JGB and swap markets in the first half of the YCC. They are integrated except for the maturity of 10 years in the second half of the YCC. In other words, arbitrage works between two markets. After the BOJ expanded the upper limit of the YCC to .25%, structural change occurred in the super long term in relation to JGB and swap markets. The decision by the BOJ has contributed to the normalization of the market function because there has been more room for the benchmark JGB yield of 10 years to move more actively.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: