{"title":"The Tax Incidence and Tax Pass-Through of Smokeless Tobacco in the US.","authors":"Yanyun He, Qian Yang, Ce Shang","doi":"10.3390/ijerph21111465","DOIUrl":null,"url":null,"abstract":"<p><strong>Background: </strong>States adopt different tax bases for smokeless tobacco (SLT), making tax incidence on SLT not directly comparable across states. In addition, how taxes are passed through to SLT prices among states that impose specific taxes, and whether the pass-through rates for SLT are affected by the uptake and evolution of e-cigarettes, is unknown.</p><p><strong>Objective: </strong>This study will calculate the tax incidence on SLT and investigate how SLT taxes are passed to prices at the 25th, 50th, and 75th percentile levels, as well as whether these pass-through rates vary by e-cigarette uptake and evolution.</p><p><strong>Methods: </strong>We regressed SLT prices on specific taxes using ordinary least square regressions while controlling for state-, year-, and quarter-fixed effects. We then tested the difference in tax pass-through rates by different periods.</p><p><strong>Findings: </strong>The average tax incidence on chewing tobacco, moist snuff, dry snuff, and snus was 22%, 22%, 23%, and 20%, respectively. For moist snuff, taxes were fully passed to prices at the 25th and 50th percentiles (rate = 1.01, <i>p</i> < 0.001) and overly passed to prices at the 75th percentile (rate = 1.25, <i>p</i> < 0.001). The e-cigarette uptake and evolution significantly raised taxes by 13 cents and 14 cents per ounce, respectively, for moist snuff at the 75th percentile prices (<i>p</i> < 0.05).</p><p><strong>Conclusions: </strong>If harm is considered a criterion for taxing tobacco products, the tax incidence on SLT could be further increased. Considering that lower-priced SLT have lower tax pass-through rates, price promotion restrictions and minimum pricing laws may be needed to increase the cost of lower-priced products. Additionally, we observed that tobacco companies tended to increase tax pass-through for premium SLT products as e-cigarettes gained popularity, which may indicate a strategic response to shifting consumer preferences.</p>","PeriodicalId":49056,"journal":{"name":"International Journal of Environmental Research and Public Health","volume":"21 11","pages":""},"PeriodicalIF":0.0000,"publicationDate":"2024-11-02","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC11593845/pdf/","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Environmental Research and Public Health","FirstCategoryId":"103","ListUrlMain":"https://doi.org/10.3390/ijerph21111465","RegionNum":3,"RegionCategory":"综合性期刊","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

Background: States adopt different tax bases for smokeless tobacco (SLT), making tax incidence on SLT not directly comparable across states. In addition, how taxes are passed through to SLT prices among states that impose specific taxes, and whether the pass-through rates for SLT are affected by the uptake and evolution of e-cigarettes, is unknown.

Objective: This study will calculate the tax incidence on SLT and investigate how SLT taxes are passed to prices at the 25th, 50th, and 75th percentile levels, as well as whether these pass-through rates vary by e-cigarette uptake and evolution.

Methods: We regressed SLT prices on specific taxes using ordinary least square regressions while controlling for state-, year-, and quarter-fixed effects. We then tested the difference in tax pass-through rates by different periods.

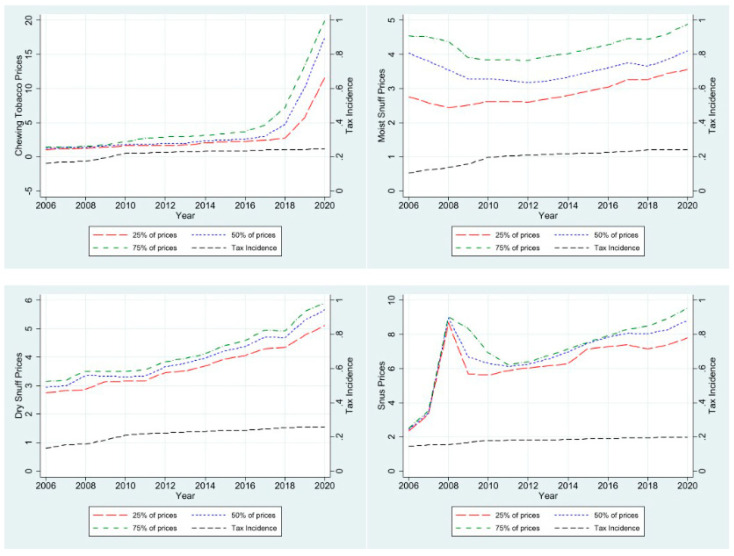

Findings: The average tax incidence on chewing tobacco, moist snuff, dry snuff, and snus was 22%, 22%, 23%, and 20%, respectively. For moist snuff, taxes were fully passed to prices at the 25th and 50th percentiles (rate = 1.01, p < 0.001) and overly passed to prices at the 75th percentile (rate = 1.25, p < 0.001). The e-cigarette uptake and evolution significantly raised taxes by 13 cents and 14 cents per ounce, respectively, for moist snuff at the 75th percentile prices (p < 0.05).

Conclusions: If harm is considered a criterion for taxing tobacco products, the tax incidence on SLT could be further increased. Considering that lower-priced SLT have lower tax pass-through rates, price promotion restrictions and minimum pricing laws may be needed to increase the cost of lower-priced products. Additionally, we observed that tobacco companies tended to increase tax pass-through for premium SLT products as e-cigarettes gained popularity, which may indicate a strategic response to shifting consumer preferences.

期刊介绍:

International Journal of Environmental Research and Public Health (IJERPH) (ISSN 1660-4601) is a peer-reviewed scientific journal that publishes original articles, critical reviews, research notes, and short communications in the interdisciplinary area of environmental health sciences and public health. It links several scientific disciplines including biology, biochemistry, biotechnology, cellular and molecular biology, chemistry, computer science, ecology, engineering, epidemiology, genetics, immunology, microbiology, oncology, pathology, pharmacology, and toxicology, in an integrated fashion, to address critical issues related to environmental quality and public health. Therefore, IJERPH focuses on the publication of scientific and technical information on the impacts of natural phenomena and anthropogenic factors on the quality of our environment, the interrelationships between environmental health and the quality of life, as well as the socio-cultural, political, economic, and legal considerations related to environmental stewardship and public health.

The 2018 IJERPH Outstanding Reviewer Award has been launched! This award acknowledge those who have generously dedicated their time to review manuscripts submitted to IJERPH. See full details at http://www.mdpi.com/journal/ijerph/awards.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: