{"title":"CEO bonus plans—And how to fix them","authors":"Kevin J. Murphy, Michael C. Jensen","doi":"10.1111/jacf.12629","DOIUrl":null,"url":null,"abstract":"<p>Our research and consulting experience leads us to conclude that almost all CEO and executive bonus plans are deeply flawed and contribute to highly counterproductive incentives and actions that end up reducing the long-run value of most companies.</p><p>Ultimately, however, the advantages of bonus-based reward plans are only going to be as good and as effective as the designers of those plans make them. While bonus plans can be structured to provide incentives focused on specific operational objectives that will lead to value creation, poorly designed plans can provide strong incentives to destroy rather than create value. For example, annual bonus plans can destroy value by providing incentives to withhold effort, shift earnings and cash flow unproductively from one period to another, and to manipulate earnings counterproductively in other ways. Bonus plans also often create incentives for the organization to destroy information critical to the effective coordination of disparate parts of large complex firms. More importantly, bonus plans too often reward participants for misrepresenting—or “lying about”—the profit potential of their business units. All of these diminish the opportunity for performance in an organization, thereby leading to the destruction of firm value.</p><p>In this paper, we describe many of the problems associated with traditional executive bonus plans and offer our suggestions for how these plans can be vastly improved. We proceed as follows. In the section “How Executive Bonus Plans Cause Problems: Overview,” we describe typical bonus plans and provide an overview of the potential problems. In the next three sections, we then discuss problems (and solutions) associated with “Using the Wrong Pay-Performance Relations,” “Using the Wrong Targets, Benchmarks, or Standards,” and “Using the Wrong Performance Measures.” In the section “Failure to Make Ex Post Adjustments to Performance Measures and Compensation,” we discuss ex post adjustments to bonuses (including subjective assessments and claw backs). In the section “Bankers' Bonuses and the Financial Crisis,” we discuss the role of banking bonuses and the 2007-2008 financial crisis. The Conclusion section summarizes our recommendations.</p><p>Figure 1 illustrates these basic components of a “typical” annual bonus plan. Under the typical plan, no bonus is paid until a lower performance threshold or hurdle is achieved, and a “hurdle bonus” is paid at this lower performance threshold. The bonus is usually capped at an upper performance threshold; after this point increased performance is not associated with an increase in the bonus. The thresholds are routinely determined by the firm's annual budgeting process. The range between the lower and upper-performance thresholds (labeled the “incentive zone” in the figure), is drawn as linear but could be convex (bowl-shaped) or concave (upside-down bowl-shaped). The “pay-performance relation” (denoted by the heavy line) is the function that shows how the bonus varies throughout the entire range of possible performance outcomes.</p><p>The bonus plan illustrated in Figure 1 is replete with incentive problems that destroy value. We talked with a CEO who participated in a bonus plan similar to that depicted in Figure 1. His performance measure was returned on equity (ROE), the upper-performance threshold was set at 15%, and he discovered that his firm could easily surpass this upper threshold. He told us, half seriously: “I'd have to be the stupidest CEO in the world to report an ROE of 18%. First, I wouldn't get any bonus for any results above the cap. Second, I could have saved some of our earnings for next year. And third, [the board of directors] would increase my target performance for next year.” This CEO's comments reflect not only his frustration with his bonus plan but also reveal that he well understands how to game the compensation system to get higher bonuses.</p><p>Improving executive bonus plans requires not only choosing the right performance measure, but also determining how performance thresholds, targets, and benchmarks are set, how the pay-performance relation is defined, and how the relation changes over time. Our discussion and recommendations will focus on details, wherein lies the devil.</p><p>In the aftermath of the 2008–2009 financial crisis, attention focused on whether bonus plans (especially those on Wall Street) create incentives to engage in excessive risk-taking. There are two ways that bonuses—or incentive compensation more broadly—can create incentives for risk-taking. The first way (to which we will return in the sections “Using the Wrong Performance Measures” and “Bankers’ Bonuses and the Financial Crisis”) is rewarding people using performance metrics that implicitly (or explicitly) reward risky behavior, such as paying mortgage brokers based on the number of loans they write, rather than for writing loans that borrowers might actually pay back. The second way is through non-linear pay-performance plans: in particular, asymmetries in rewards for good performance and penalties for failure. When CEOs (or traders or brokers, etc.) receive rewards for upside risk, but are not penalized for downside risk, they will naturally take greater risks than if they faced symmetric consequences in both directions.</p><p>Consider, for example, an investment opportunity with a 50% chance of making $100 million in profit, and a 50% chance of losing $200 million. This investment opportunity has an expected value of −$50 million and should be rejected. However, suppose that the CEO (or trader or broker, etc.) has an incentive plan that gives him a share of any positive profit, but is set at zero if profit is negative. From the perspective of this CEO (or trader or broker, etc.) with the asymmetric bonus plan, the investment opportunity has a positive expected value.</p><p>More generally, all “non-linearities” in the pay-performance relation affect incentives to take risks. When the pay-performance relation is convex (or bowl-shaped) executives can increase their total bonus payouts by increasing the variability of their performance. On the other hand, in situations where the pay-performance relation is concave (or upside-down bowl-shaped) in the relevant range, the opposite is true — CEOs have incentives to smooth the variability in performance over time by withholding high performance this period and saving as much of it as possible for next period.</p><p>The problems associated with non-linear pay-performance relations can be partially solved by making the relation linear. First, the upper performance threshold (and bonus cap) can be eliminated, so that superior performance continues to be rewarded by higher bonuses. Second, the lower performance threshold can be dropped, thus eliminating the problematic discontinuous “jump” in the pay-performance relation. Finally, the plan can be made linear by ensuring that the slope of the pay-performance relation (that is, the incremental bonus associated with a given increase in performance) is constant regardless of the level of performance.</p><p>Successfully implemented (in conjunction with recommendations on performance measures and standards discussed later in this paper), linearity takes “timing” out of the equation.2 For example, a CEO paid 5% of profit year after year will have no incentives to play accounting or other “games” with profit in the fourth quarter, since any increase in fourth quarter bonuses will be met with an equal but opposite decrease in bonuses in the following quarter. The CEO paid under a linear pay-performance plan also has no incentive to engage in excess risk-taking, since the rewards for positive profits are the same as the penalties for losses. Finally, another advantage of linear plans is that they are simple: non-linear bonus plans are typically needlessly complicated to implement (and often difficult to communicate to the participants). The simpler the plan, the more likely the incentive outcome.</p><p>Truncating otherwise-negative bonuses at zero seems like a practical solution to the messy problem of imposing or enforcing negative bonuses on CEOs. However, protecting the CEO from negative bonuses (through “upside-only bonuses” set to zero when profit is negative) puts a non-linearity or “kink” or in the pay-performance relation at zero profit, which creates many of the problems discussed above. In particular, CEOs paid under this plan will have no incentives to improve profit this year when they see no way to generate positive profit. In addition, they will predictably attempt to shift profit from the current year to next year in this situation so that they can more be profitable next year. Finally, truncating bonuses at zero can also lead to excessive risk-taking, since such plans reward CEOs for positive profit but do not penalize them for losses.</p><p>Solving the problems with upside-only bonuses involves designing (and enforcing) plans with negative bonuses. It is our experience (and perhaps common sense) that executives are loathe to write end-of-the-year “negative bonus” checks back to the company for sub-par performance. Fortunately, there are alternative and palatable ways to introduce effective negative bonuses into executive bonus contracts that do not involve writing checks back to the company.</p><p>Bonuses are typically based on performance compared to something the company might call a performance standard, bogey, target, hurdle, or benchmark. Henceforth, we use the term “benchmark” to refer to any or all of these commonly used terms. Examples include net income measured against budgeted net income, earnings-per-share (EPS) versus last year's EPS, sales growth (i.e., this year's sales vs. last year's sales), cash flow versus a charge for capital, performance measured relative to peer-group performance, or performance measured against financial or nonfinancial strategic “milestones.” It is useful to think of these benchmark alternatives as determining how the pay-performance relation depicted in Figure 1 is initially set, and how it shifts to the right or the leftover time.</p><p>First let us recognize that when performance in a bonus plan is measured relative to a benchmark, there are two ways to achieve higher bonuses: increase the performance measure, or decrease the benchmark. Suppose that the performance measure is X and that the benchmark is B and bonuses are based on the difference between them (X—B). The benchmark B might be budgeted performance, prior-year performance, strategic milestones, or the performance of other executives or an industry peer group. Because bonuses are increased either by increasing X or by decreasing B, the integrity of the plan is reduced whenever the people eligible to receive bonuses under the plan (“plan participants”) can take actions that reduce B. And in most bonus systems plan participants in one way or another can and do influence the benchmark B.</p><p>Business history is littered with companies that “got what they paid for.” Paying salespeople commissions based on revenues, for example, provides incentives to increase revenues regardless of the costs or relative margins of different products. Likewise, paying rank-and-file workers “piece rates” based on units produced provides incentives to maximize quantity irrespective of quality, and paying a division head based solely on divisional profit leads the division head to ignore the effects of his decisions on the profits of other divisions. Similarly, paying CEOs based on short-run accounting profits provides incentives to increase short-run profits (by, e.g., cutting R&D) even if doing so reduces value in the long run. In each of these cases, employees will predictably take actions to increase their compensation, even if these actions are at the expense of long-run firm value. Indeed, many examples of dysfunctional compensation and incentive systems can be traced to inappropriate performance measures.</p><p>The problem of inappropriate performance measures is illustrated succinctly by the title of Steven Kerr's famous 1975 article, “On the folly of rewarding A, while hoping for B.”5 For CEOs, well-intentioned compensation committees hope to increase firm value (“B”) by rewarding the executive on a variety of performance measures (“A”) that induce actions not perfectly correlated (or even inversely correlated) with the actions that increase firm value. Conceptually, the “perfect” performance measure for a CEO is the CEO's personal contribution to the value of the firm. This contribution includes the effect that the CEO has on the performance of others in the organization, and also the effects that the CEO's actions this year have on performance in future periods. Unfortunately, the CEO's contribution to firm value is never directly measurable; the available measures will inevitably fail to capture ways that the CEO creates value and will capture the effects of factors not due to the efforts of the CEO or fail to capture ways that the CEO destroys value. The challenge in designing incentive plans is to select performance measures that capture important aspects of the CEO's contributions to firm value, while recognizing that all performance measures are imperfect and therefore create unintended side effects.</p><p>We start this discussion by considering the counterproductive effects associated with using accounting performance measures, and the even worse problems that are created when these measures are expressed as ratios or rates of return (such as EPS or ROE). We then move on to discuss the advantages and challenges associated with incorporating charges for the cost of capital into incentive plans and conclude by outlining simple steps that can dramatically improve almost any existing bonus plan.</p><p>It is generally impossible to create fool-proof objective and accurate measures of the contribution to firm value by an individual, department, or division. And this also applies to the performance measurement and compensation of the CEO. Therefore, every bonus system should allow for denial or adjustment of a bonus that is not earned by the CEO or is earned from actions that do not benefit the firm or even damage the firm. In addition, it is important to include contributions of the CEO that do not show up in his or her objective performance measure. While explicitly allowing for such <i>ex post</i> adjustments creates its own problems and challenges we believe failing to confront these subjective issues results in greater mistakes than dealing with them directly.</p><p>Thus, we believe it is important for compensation committees to make after-the-fact ex post adjustments to both the measure of CEO performance and the compensation actually paid to the CEO. The three most important and common failings in this domain are: (a) failing to make subjective assessments of CEO performance, (b) protecting CEOs too much from factors beyond their control, and (c) failing to claw back inappropriate rewards to the CEO.</p><p>No discussion of executive bonus plans is complete without an analysis of the Wall Street “bonus culture” that has routinely been blamed for causing the 2007–2009 financial crisis and the continuing problems in the economy. Public anger over banking bonuses surfaced in January 2009 amid reports that Wall Street bankers were set to receive nearly $20 billion in bonuses for 2008 performance,13 and heightened with revelations that bailout-recipient Merrill Lynch paid nearly $4 billion in year-end bonuses just prior to the completion of its acquisition by Bank of America.14 Outrage further intensified following the March 2009 revelation that American International Group (AIG) was in the process of paying $168 million in “retention bonuses” to its executives. These revelations—coupled with suspicions that the bonus culture facilitated excessive risk-taking—led to an effective prohibition on cash bonuses for participants in the government's Troubled Asset Relief Program (TARP) and to more sweeping regulation of executive compensation as part of the July 2010 Dodd-Frank Wall Street Reform Act. While most of the regulations focus on senior executive officers, the banking-specific provisions in Dodd-Frank were applicable to any employee that could expose the institution to substantial losses.</p><p>In this section, we analyze the bonus culture as it applies to three groups of banking employees: top-level executives, mortgage brokers, and traders. Ultimately, we find little evidence that the bonus culture provided incentives for excessive risk-taking for top-level executives; indeed, the general structure of low base salaries and high bonus opportunities paid in a combination of cash, stock, and options not only mitigates risk-taking but fulfills many of the “guiding principles” for bonus design espoused in this paper. However, we also identify design flaws in the performance measures used for mortgage brokers and loan officers, who were too often paid to write loans with little regard for the borrowers’ ability to repay.</p>","PeriodicalId":46789,"journal":{"name":"Journal of Applied Corporate Finance","volume":"36 3","pages":"95-110"},"PeriodicalIF":1.4000,"publicationDate":"2024-11-21","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12629","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Corporate Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12629","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

Our research and consulting experience leads us to conclude that almost all CEO and executive bonus plans are deeply flawed and contribute to highly counterproductive incentives and actions that end up reducing the long-run value of most companies.

Ultimately, however, the advantages of bonus-based reward plans are only going to be as good and as effective as the designers of those plans make them. While bonus plans can be structured to provide incentives focused on specific operational objectives that will lead to value creation, poorly designed plans can provide strong incentives to destroy rather than create value. For example, annual bonus plans can destroy value by providing incentives to withhold effort, shift earnings and cash flow unproductively from one period to another, and to manipulate earnings counterproductively in other ways. Bonus plans also often create incentives for the organization to destroy information critical to the effective coordination of disparate parts of large complex firms. More importantly, bonus plans too often reward participants for misrepresenting—or “lying about”—the profit potential of their business units. All of these diminish the opportunity for performance in an organization, thereby leading to the destruction of firm value.

In this paper, we describe many of the problems associated with traditional executive bonus plans and offer our suggestions for how these plans can be vastly improved. We proceed as follows. In the section “How Executive Bonus Plans Cause Problems: Overview,” we describe typical bonus plans and provide an overview of the potential problems. In the next three sections, we then discuss problems (and solutions) associated with “Using the Wrong Pay-Performance Relations,” “Using the Wrong Targets, Benchmarks, or Standards,” and “Using the Wrong Performance Measures.” In the section “Failure to Make Ex Post Adjustments to Performance Measures and Compensation,” we discuss ex post adjustments to bonuses (including subjective assessments and claw backs). In the section “Bankers' Bonuses and the Financial Crisis,” we discuss the role of banking bonuses and the 2007-2008 financial crisis. The Conclusion section summarizes our recommendations.

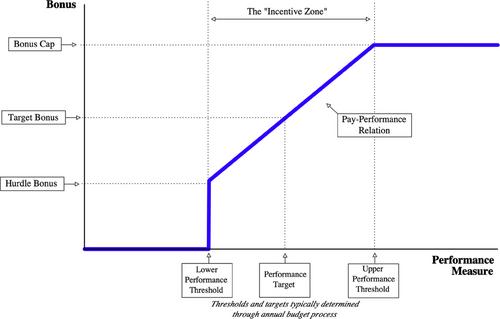

Figure 1 illustrates these basic components of a “typical” annual bonus plan. Under the typical plan, no bonus is paid until a lower performance threshold or hurdle is achieved, and a “hurdle bonus” is paid at this lower performance threshold. The bonus is usually capped at an upper performance threshold; after this point increased performance is not associated with an increase in the bonus. The thresholds are routinely determined by the firm's annual budgeting process. The range between the lower and upper-performance thresholds (labeled the “incentive zone” in the figure), is drawn as linear but could be convex (bowl-shaped) or concave (upside-down bowl-shaped). The “pay-performance relation” (denoted by the heavy line) is the function that shows how the bonus varies throughout the entire range of possible performance outcomes.

The bonus plan illustrated in Figure 1 is replete with incentive problems that destroy value. We talked with a CEO who participated in a bonus plan similar to that depicted in Figure 1. His performance measure was returned on equity (ROE), the upper-performance threshold was set at 15%, and he discovered that his firm could easily surpass this upper threshold. He told us, half seriously: “I'd have to be the stupidest CEO in the world to report an ROE of 18%. First, I wouldn't get any bonus for any results above the cap. Second, I could have saved some of our earnings for next year. And third, [the board of directors] would increase my target performance for next year.” This CEO's comments reflect not only his frustration with his bonus plan but also reveal that he well understands how to game the compensation system to get higher bonuses.

Improving executive bonus plans requires not only choosing the right performance measure, but also determining how performance thresholds, targets, and benchmarks are set, how the pay-performance relation is defined, and how the relation changes over time. Our discussion and recommendations will focus on details, wherein lies the devil.

In the aftermath of the 2008–2009 financial crisis, attention focused on whether bonus plans (especially those on Wall Street) create incentives to engage in excessive risk-taking. There are two ways that bonuses—or incentive compensation more broadly—can create incentives for risk-taking. The first way (to which we will return in the sections “Using the Wrong Performance Measures” and “Bankers’ Bonuses and the Financial Crisis”) is rewarding people using performance metrics that implicitly (or explicitly) reward risky behavior, such as paying mortgage brokers based on the number of loans they write, rather than for writing loans that borrowers might actually pay back. The second way is through non-linear pay-performance plans: in particular, asymmetries in rewards for good performance and penalties for failure. When CEOs (or traders or brokers, etc.) receive rewards for upside risk, but are not penalized for downside risk, they will naturally take greater risks than if they faced symmetric consequences in both directions.

Consider, for example, an investment opportunity with a 50% chance of making $100 million in profit, and a 50% chance of losing $200 million. This investment opportunity has an expected value of −$50 million and should be rejected. However, suppose that the CEO (or trader or broker, etc.) has an incentive plan that gives him a share of any positive profit, but is set at zero if profit is negative. From the perspective of this CEO (or trader or broker, etc.) with the asymmetric bonus plan, the investment opportunity has a positive expected value.

More generally, all “non-linearities” in the pay-performance relation affect incentives to take risks. When the pay-performance relation is convex (or bowl-shaped) executives can increase their total bonus payouts by increasing the variability of their performance. On the other hand, in situations where the pay-performance relation is concave (or upside-down bowl-shaped) in the relevant range, the opposite is true — CEOs have incentives to smooth the variability in performance over time by withholding high performance this period and saving as much of it as possible for next period.

The problems associated with non-linear pay-performance relations can be partially solved by making the relation linear. First, the upper performance threshold (and bonus cap) can be eliminated, so that superior performance continues to be rewarded by higher bonuses. Second, the lower performance threshold can be dropped, thus eliminating the problematic discontinuous “jump” in the pay-performance relation. Finally, the plan can be made linear by ensuring that the slope of the pay-performance relation (that is, the incremental bonus associated with a given increase in performance) is constant regardless of the level of performance.

Successfully implemented (in conjunction with recommendations on performance measures and standards discussed later in this paper), linearity takes “timing” out of the equation.2 For example, a CEO paid 5% of profit year after year will have no incentives to play accounting or other “games” with profit in the fourth quarter, since any increase in fourth quarter bonuses will be met with an equal but opposite decrease in bonuses in the following quarter. The CEO paid under a linear pay-performance plan also has no incentive to engage in excess risk-taking, since the rewards for positive profits are the same as the penalties for losses. Finally, another advantage of linear plans is that they are simple: non-linear bonus plans are typically needlessly complicated to implement (and often difficult to communicate to the participants). The simpler the plan, the more likely the incentive outcome.

Truncating otherwise-negative bonuses at zero seems like a practical solution to the messy problem of imposing or enforcing negative bonuses on CEOs. However, protecting the CEO from negative bonuses (through “upside-only bonuses” set to zero when profit is negative) puts a non-linearity or “kink” or in the pay-performance relation at zero profit, which creates many of the problems discussed above. In particular, CEOs paid under this plan will have no incentives to improve profit this year when they see no way to generate positive profit. In addition, they will predictably attempt to shift profit from the current year to next year in this situation so that they can more be profitable next year. Finally, truncating bonuses at zero can also lead to excessive risk-taking, since such plans reward CEOs for positive profit but do not penalize them for losses.

Solving the problems with upside-only bonuses involves designing (and enforcing) plans with negative bonuses. It is our experience (and perhaps common sense) that executives are loathe to write end-of-the-year “negative bonus” checks back to the company for sub-par performance. Fortunately, there are alternative and palatable ways to introduce effective negative bonuses into executive bonus contracts that do not involve writing checks back to the company.

Bonuses are typically based on performance compared to something the company might call a performance standard, bogey, target, hurdle, or benchmark. Henceforth, we use the term “benchmark” to refer to any or all of these commonly used terms. Examples include net income measured against budgeted net income, earnings-per-share (EPS) versus last year's EPS, sales growth (i.e., this year's sales vs. last year's sales), cash flow versus a charge for capital, performance measured relative to peer-group performance, or performance measured against financial or nonfinancial strategic “milestones.” It is useful to think of these benchmark alternatives as determining how the pay-performance relation depicted in Figure 1 is initially set, and how it shifts to the right or the leftover time.

First let us recognize that when performance in a bonus plan is measured relative to a benchmark, there are two ways to achieve higher bonuses: increase the performance measure, or decrease the benchmark. Suppose that the performance measure is X and that the benchmark is B and bonuses are based on the difference between them (X—B). The benchmark B might be budgeted performance, prior-year performance, strategic milestones, or the performance of other executives or an industry peer group. Because bonuses are increased either by increasing X or by decreasing B, the integrity of the plan is reduced whenever the people eligible to receive bonuses under the plan (“plan participants”) can take actions that reduce B. And in most bonus systems plan participants in one way or another can and do influence the benchmark B.

Business history is littered with companies that “got what they paid for.” Paying salespeople commissions based on revenues, for example, provides incentives to increase revenues regardless of the costs or relative margins of different products. Likewise, paying rank-and-file workers “piece rates” based on units produced provides incentives to maximize quantity irrespective of quality, and paying a division head based solely on divisional profit leads the division head to ignore the effects of his decisions on the profits of other divisions. Similarly, paying CEOs based on short-run accounting profits provides incentives to increase short-run profits (by, e.g., cutting R&D) even if doing so reduces value in the long run. In each of these cases, employees will predictably take actions to increase their compensation, even if these actions are at the expense of long-run firm value. Indeed, many examples of dysfunctional compensation and incentive systems can be traced to inappropriate performance measures.

The problem of inappropriate performance measures is illustrated succinctly by the title of Steven Kerr's famous 1975 article, “On the folly of rewarding A, while hoping for B.”5 For CEOs, well-intentioned compensation committees hope to increase firm value (“B”) by rewarding the executive on a variety of performance measures (“A”) that induce actions not perfectly correlated (or even inversely correlated) with the actions that increase firm value. Conceptually, the “perfect” performance measure for a CEO is the CEO's personal contribution to the value of the firm. This contribution includes the effect that the CEO has on the performance of others in the organization, and also the effects that the CEO's actions this year have on performance in future periods. Unfortunately, the CEO's contribution to firm value is never directly measurable; the available measures will inevitably fail to capture ways that the CEO creates value and will capture the effects of factors not due to the efforts of the CEO or fail to capture ways that the CEO destroys value. The challenge in designing incentive plans is to select performance measures that capture important aspects of the CEO's contributions to firm value, while recognizing that all performance measures are imperfect and therefore create unintended side effects.

We start this discussion by considering the counterproductive effects associated with using accounting performance measures, and the even worse problems that are created when these measures are expressed as ratios or rates of return (such as EPS or ROE). We then move on to discuss the advantages and challenges associated with incorporating charges for the cost of capital into incentive plans and conclude by outlining simple steps that can dramatically improve almost any existing bonus plan.

It is generally impossible to create fool-proof objective and accurate measures of the contribution to firm value by an individual, department, or division. And this also applies to the performance measurement and compensation of the CEO. Therefore, every bonus system should allow for denial or adjustment of a bonus that is not earned by the CEO or is earned from actions that do not benefit the firm or even damage the firm. In addition, it is important to include contributions of the CEO that do not show up in his or her objective performance measure. While explicitly allowing for such ex post adjustments creates its own problems and challenges we believe failing to confront these subjective issues results in greater mistakes than dealing with them directly.

Thus, we believe it is important for compensation committees to make after-the-fact ex post adjustments to both the measure of CEO performance and the compensation actually paid to the CEO. The three most important and common failings in this domain are: (a) failing to make subjective assessments of CEO performance, (b) protecting CEOs too much from factors beyond their control, and (c) failing to claw back inappropriate rewards to the CEO.

No discussion of executive bonus plans is complete without an analysis of the Wall Street “bonus culture” that has routinely been blamed for causing the 2007–2009 financial crisis and the continuing problems in the economy. Public anger over banking bonuses surfaced in January 2009 amid reports that Wall Street bankers were set to receive nearly $20 billion in bonuses for 2008 performance,13 and heightened with revelations that bailout-recipient Merrill Lynch paid nearly $4 billion in year-end bonuses just prior to the completion of its acquisition by Bank of America.14 Outrage further intensified following the March 2009 revelation that American International Group (AIG) was in the process of paying $168 million in “retention bonuses” to its executives. These revelations—coupled with suspicions that the bonus culture facilitated excessive risk-taking—led to an effective prohibition on cash bonuses for participants in the government's Troubled Asset Relief Program (TARP) and to more sweeping regulation of executive compensation as part of the July 2010 Dodd-Frank Wall Street Reform Act. While most of the regulations focus on senior executive officers, the banking-specific provisions in Dodd-Frank were applicable to any employee that could expose the institution to substantial losses.

In this section, we analyze the bonus culture as it applies to three groups of banking employees: top-level executives, mortgage brokers, and traders. Ultimately, we find little evidence that the bonus culture provided incentives for excessive risk-taking for top-level executives; indeed, the general structure of low base salaries and high bonus opportunities paid in a combination of cash, stock, and options not only mitigates risk-taking but fulfills many of the “guiding principles” for bonus design espoused in this paper. However, we also identify design flaws in the performance measures used for mortgage brokers and loan officers, who were too often paid to write loans with little regard for the borrowers’ ability to repay.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: