{"title":"Which Messages Motivate Tax Compliance in Low Administrative Capacity Settings? Experimental Evidence From Two Mozambican Municipalities","authors":"Armin von Schiller","doi":"10.1002/pa.2960","DOIUrl":null,"url":null,"abstract":"<p>Over the past two decades, tax nudging has gained popularity as a method to boost tax compliance and help revenue authorities increase tax collection. However, most evidence on the effect of behaviourally informed tax letters comes from environments with high administrative capacity, which raises doubts about its generalizability. Against this background, this article tests the compliance effect of including messages that trigger deterrence or reciprocity beliefs in tax letters through a randomized controlled trial implemented in two mid-sized Mozambican municipalities, Vilankulo and Dondo. Conducted in 2018, the experiment focuses on property taxation, a tax overwhelmingly perceived to perform well below its potential in many low- and middle-income countries. The analysis relies on administrative data and exploits the complete universe of registered property tax taxpayers, including individuals and enterprises. The results indicate that (i) receiving a notification letter – not necessarily common practice in many contexts – has a significant positive impact on compliance; (ii) among enterprises, the message alluding to reciprocity backfires, while the most effective message to include generally is the one alluding to deterrence; and (iii) previously compliant taxpayers react negatively to the letter, regardless of the message included. These results carry relevant policy implications, indicating the large scope for behaviourally informed letters to help increase tax compliance, even in low administrative capacity settings.</p>","PeriodicalId":47153,"journal":{"name":"Journal of Public Affairs","volume":"24 4","pages":""},"PeriodicalIF":1.8000,"publicationDate":"2024-11-19","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/pa.2960","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Public Affairs","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/pa.2960","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"PUBLIC ADMINISTRATION","Score":null,"Total":0}

引用次数: 0

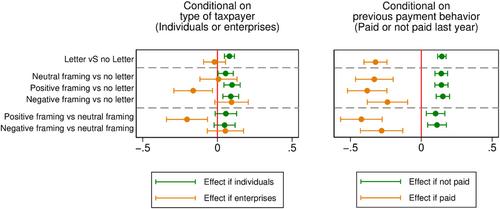

Abstract

Over the past two decades, tax nudging has gained popularity as a method to boost tax compliance and help revenue authorities increase tax collection. However, most evidence on the effect of behaviourally informed tax letters comes from environments with high administrative capacity, which raises doubts about its generalizability. Against this background, this article tests the compliance effect of including messages that trigger deterrence or reciprocity beliefs in tax letters through a randomized controlled trial implemented in two mid-sized Mozambican municipalities, Vilankulo and Dondo. Conducted in 2018, the experiment focuses on property taxation, a tax overwhelmingly perceived to perform well below its potential in many low- and middle-income countries. The analysis relies on administrative data and exploits the complete universe of registered property tax taxpayers, including individuals and enterprises. The results indicate that (i) receiving a notification letter – not necessarily common practice in many contexts – has a significant positive impact on compliance; (ii) among enterprises, the message alluding to reciprocity backfires, while the most effective message to include generally is the one alluding to deterrence; and (iii) previously compliant taxpayers react negatively to the letter, regardless of the message included. These results carry relevant policy implications, indicating the large scope for behaviourally informed letters to help increase tax compliance, even in low administrative capacity settings.

期刊介绍:

The Journal of Public Affairs provides an international forum for refereed papers, case studies and reviews on the latest developments, practice and thinking in government relations, public affairs, and political marketing. The Journal is guided by the twin objectives of publishing submissions of the utmost relevance to the day-to-day practice of communication specialists, and promoting the highest standards of intellectual rigour.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: