Equity Term Structures without Dividend Strips Data

IF 7.6

1区 经济学

Q1 BUSINESS, FINANCE

引用次数: 0

Abstract

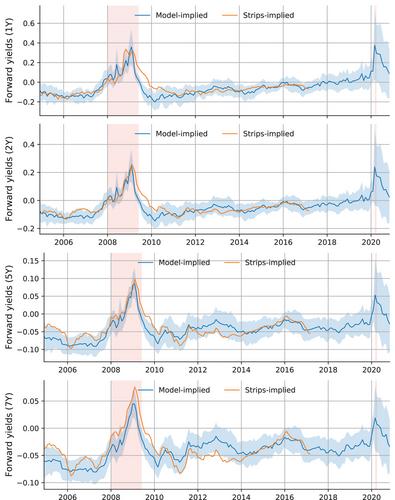

We use a large cross section of equity returns to estimate a rich affine model of equity prices, dividends, returns, and their dynamics. Our model prices dividend strips of the market and equity portfolios without using strips data in the estimation. Yet model-implied equity yields closely match yields on traded strips. Our model extends equity term-structure data over time (to the 1970s) and across maturities, and generates term structures for various equity portfolios. The novel cross section of term structures from our model covers 45 years and includes several recessions, providing a novel set of empirical moments to discipline asset pricing models.

无红利带的股本期限结构数据

我们利用股票收益的大量横截面数据来估计股票价格、股息、收益及其动态的丰富仿射模型。我们的模型为市场和股票投资组合的股息条定价,在估算过程中不使用股息条数据。然而,模型推测的股票收益率与交易股息条的收益率非常接近。我们的模型对股票期限结构数据进行了跨时间(到 20 世纪 70 年代)和跨期限的扩展,并生成了各种股票组合的期限结构。我们的模型所产生的期限结构的新横截面覆盖了 45 年的时间,包括了几次经济衰退,为规范资产定价模型提供了一套新颖的经验矩。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Journal of Finance

Multiple-

CiteScore

12.90

自引率

2.50%

发文量

88

期刊介绍:

The Journal of Finance is a renowned publication that disseminates cutting-edge research across all major fields of financial inquiry. Widely regarded as the most cited academic journal in finance, each issue reaches over 8,000 academics, finance professionals, libraries, government entities, and financial institutions worldwide. Published bi-monthly, the journal serves as the official publication of The American Finance Association, the premier academic organization dedicated to advancing knowledge and understanding in financial economics. Join us in exploring the forefront of financial research and scholarship.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: