Till Strunge, Lukas Küng, Nixon Sunny, Nilay Shah, Phil Renforth and Mijndert Van der Spek

{"title":"Finding least-cost net-zero CO2e strategies for the European cement industry using geospatial techno-economic modelling†","authors":"Till Strunge, Lukas Küng, Nixon Sunny, Nilay Shah, Phil Renforth and Mijndert Van der Spek","doi":"10.1039/D4SU00373J","DOIUrl":null,"url":null,"abstract":"<p >Cement production is responsible for approximately 7% of anthropogenic CO<small><sub>2</sub></small>-equivalent (CO<small><sub>2e</sub></small>) emissions, while characterised by low margins and the highest carbon intensity of any industry per unit of revenue. Hence, economically viable decarbonisation strategies must be found. The costs of many emission reduction strategies depend on geographical factors, such as plant location and proximity to feedstock or on synergies with other cement producers. The current literature lacks quantification of least-cost decarbonisation strategies of a country or region's total cement sector, while taking stock of these geospatial differences. Here, we quantify which intervention ensembles could lead to least-cost, full decarbonisation of the European cement industry, for multiple European regions. We show that least-cost strategies include the use of calcined clay cements coupled with carbon capture and storage (CCS) from existing cement plants and direct air capture with carbon storage (DACCS) in locations close to CO<small><sub>2</sub></small> storage sites. We find that these strategies could cost €72–€75 per tonne of cement (t<small><sub>cement</sub></small><small><sup>−1</sup></small>, up from €46–€51.5 t<small><sub>cement</sub></small><small><sup>−1</sup></small>), which could be offset by future costs of cement production otherwise amounting to €105–€130 t<small><sub>cement</sub></small><small><sup>−1</sup></small> taking the cost of CO<small><sub>2e</sub></small> emission certificates into account. The analysis shows that for economically viable decarbonisation, collaborative and region-catered approaches become imperative, while supplementary cementitious materials including calcined clays have a key role.</p>","PeriodicalId":74745,"journal":{"name":"RSC sustainability","volume":" 10","pages":" 3054-3076"},"PeriodicalIF":0.0000,"publicationDate":"2024-09-13","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://pubs.rsc.org/en/content/articlepdf/2024/su/d4su00373j?page=search","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"RSC sustainability","FirstCategoryId":"1085","ListUrlMain":"https://pubs.rsc.org/en/content/articlelanding/2024/su/d4su00373j","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

引用次数: 0

Abstract

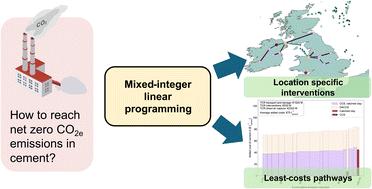

Cement production is responsible for approximately 7% of anthropogenic CO2-equivalent (CO2e) emissions, while characterised by low margins and the highest carbon intensity of any industry per unit of revenue. Hence, economically viable decarbonisation strategies must be found. The costs of many emission reduction strategies depend on geographical factors, such as plant location and proximity to feedstock or on synergies with other cement producers. The current literature lacks quantification of least-cost decarbonisation strategies of a country or region's total cement sector, while taking stock of these geospatial differences. Here, we quantify which intervention ensembles could lead to least-cost, full decarbonisation of the European cement industry, for multiple European regions. We show that least-cost strategies include the use of calcined clay cements coupled with carbon capture and storage (CCS) from existing cement plants and direct air capture with carbon storage (DACCS) in locations close to CO2 storage sites. We find that these strategies could cost €72–€75 per tonne of cement (tcement−1, up from €46–€51.5 tcement−1), which could be offset by future costs of cement production otherwise amounting to €105–€130 tcement−1 taking the cost of CO2e emission certificates into account. The analysis shows that for economically viable decarbonisation, collaborative and region-catered approaches become imperative, while supplementary cementitious materials including calcined clays have a key role.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: