{"title":"Michael Jensen's contributions to the theory of the firm: A tribute in three acts","authors":"Bartley J. Madden, Douglas E. Stevens","doi":"10.1111/jacf.12620","DOIUrl":null,"url":null,"abstract":"<p>Michael Cole Jensen (1939–2024) passed away on April 2, 2024 in Sarasota, Florida. A number of fitting tributes have appeared celebrating the life of one of the world's most productive and influential financial economists. A tribute to Jensen by Eugene Fama on the University of Chicago website <i>ProMarket</i> emphasizes how Jensen's research contributions put him in the highest echelons of academic finance and economics. Fama cites several of Jensen's seminal papers, including his 1976 paper coauthored with William Meckling, “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.”1 Jensen's paper with Meckling became the most heavily cited paper in the corporate finance literature and established agency theory as the dominant theory of the firm in finance and accounting. Fama also highlights Jensen's role in the transformation of finance into a scientific discipline, noting that he founded the <i>Journal of Financial Economics</i> in 1974 and edited it for over 20 years to drag the <i>Journal of Finance</i> “into the era of scientific research.” Finally, Fama highlights Jensen's leadership and foresight in launching the Social Science Research Network (SSRN) in 1994 to advance research across the social sciences.2</p><p>Another tribute to Jensen on <i>ProMarket</i> by Cambridge Law Professor Brian Cheffins suggests that Jensen's thinking on the public corporation underwent a 180-degree turn. In Cheffins's account, Jensen began his career as a strong advocate of the corporation as a driver of innovation and growth in the economy, calling it “an awesome social invention” in his seminal article with Meckling. After the economic stagnation and rampant inflation of the 1970s, however, Jensen allegedly became a fierce critic of the corporation, expressing skepticism about internal corporate systems and emphasizing the effectiveness of the market for corporate control to discipline manager opportunism. Cheffins highlights Jensen's promotion of the corporate takeover boom of the 1980s and the proliferation of incentive pay for executives based on stock options and earnings targets.</p><p>When the takeover boom suddenly halted in the 1990s, Cheffins notes that Jensen blamed executives and politicians who had put up roadblocks to corporate takeovers. Jensen also criticized self-serving managers and compliant boards who had used incentive pay to shield executives from market risk while adding significantly to their total compensation. Yet, public corporations continued to grow in number and size and were a major contributor to strong economic growth and soaring stock prices throughout the 1990s. But in Cheffins’ view, for all the accomplishments of US public companies, “there would be no reversal of Jensen's 180 degree turn regarding the public company.”3</p><p>In contrast to prior tributes, we focus on Jensen's contributions to the theory of the firm over his illustrious career. We argue that his contributions in this area represent the greatest and yet, in some respects, the most misunderstood part of Jensen's legacy. We identify three phases or “acts” in Jensen's thinking regarding the public corporation and the role of management. Consistent with Cheffins’ tribute, we argue that Jensen had a 180-degree turn in his thinking after the economic stagnation of the 1970s and became a fierce critic of <i>certain practices</i> of the public corporation. However, we argue that Jensen renewed (if indeed he ever completely lost) his confidence in the public corporation later in life. That renewed confidence came with the realization that his original theory of the firm was incomplete. We focus on Jensen's third act, where he attempted to revise his theory by incorporating integrity and stakeholder perspectives and developed a highly innovative educational program for leadership training. Despite the dramatic changes we observe across these three acts, however, we identify a continuity in Jensen's thought that provides a path forward for future development in the theory of the firm to address the challenges of modern capitalism.</p><p>Jensen received his PhD at the University of Chicago in 1968, at a time when the economics department had already pivoted from the institutional economics of Thorstein Veblen and Frank Knight to the neoclassical economics of Milton Friedman and George Stigler. His dissertation, which was supervised by Merton Miller, developed a method of measuring fund manager performance called Jensen's alpha and was later published in <i>The Journal of Finance</i>.4 Through his association with Miller and Eugene Fama at Chicago, Jensen's early work focused on market efficiency, the capital asset pricing model (CAPM), and market reactions to financial information releases. For example, he coauthored a 1969 paper with Fama, Lawrence Fisher, and Richard Roll establishing the event-study method that became the standard in capital market studies in finance and accounting.5</p><p>Most academic researchers, however, associate Jensen's early career with the powerful theory of the firm he developed with William Meckling called <i>agency theory</i>. Previous theories of the firm used the marginal analysis presented by Alfred Marshall (1842–1924) in his early synthesis of neoclassical economics at Cambridge University. It was under Marshall's influence that Cambridge dropped political economy from the moral sciences in 1903 before expunging the label “political” in its attempts to make the field of economics an objective science.6 Based on Marshall's price theory, economists initially modeled the firm as a set of cost and demand curves categorized by market structure (whether perfect competition, pure monopoly, monopolistic competition, or some other intermediate variation thereof). The economic function of a firm was said to be to combine economic resources (plant, machinery, labor, etc.) in order to produce goods and services demanded by consumers. The first task of a theory of the firm, therefore, is to explain why firm coordination is superior to market coordination.</p><p>In his seminal paper published in 1937 entitled, “The Nature of the Firm,” Ronald Coase (1910–2013) argued that firms emerge from a competitive process as the most efficient, or least-cost, means of coordinating economic activity. Coase also argued that firm size is influenced by rising marginal costs of organization and supervision, so a firm will eventually stop growing when the marginal costs rise to meet the marginal benefits.7</p><p>In contrast to previous neoclassical theories, Jensen and Meckling viewed the firm as a “nexus of contracts” among all the different stakeholders with claims on the firm. Their theory of the firm focused on the agency relationship that arises when a principal hires an agent to perform some task that involves the delegation of decision-making authority. Jensen argued that agency relationships exist in all organizations and across all levels of management, including the relationship between shareholders and managers of a public corporation. Given the traditional assumptions of information asymmetry and self-interested agents, the theory characterized the principal's problem as choosing some combination of formal contracting and financial incentives to control opportunistic behavior on the part of agents to maximize the wealth of the firm's shareholders (as the residual claimants).</p><p>Like previous neoclassical theories, agency theory assumed that individuals have a well-defined utility function with preferences only for wealth and leisure. Although Jensen and Meckling themselves made serious efforts to investigate alternative models of human behavior,8 the Jensen-Meckling agency framework nevertheless relied on self-interested maximizing behavior to make the theory tractable for their formal modeling and theorizing. The underlying behavioral assumptions of agency theory contrasted sharply with the assumptions of institutional economic theory, which characterized economic agents as influenced by nonfinancial factors such as social norms, institutions, and culture. Institutional economists had established business schools in the new research university in the late 19th century and their theoretical perspective still dominated the nation's business schools.9</p><p>Jensen played a central role in promoting agency theory through his own research and in his role as editor of the <i>Journal of Financial Economics</i>. Further, he promoted the theory in practitioner-oriented outlets such as the <i>Harvard Business Review</i> and the <i>Wall Street Journal</i>. Finally, Jensen promoted his theory of the firm to students in his MBA courses at the University of Rochester and later at Harvard. Between 1967 and 1988, Jensen taught finance and business administration at the University of Rochester Graduate School of Business Administration. He joined the Harvard Business School on a half-time appointment in 1985, dividing his time between Rochester and Harvard, before taking a full-time appointment at Harvard in 1988.</p><p>Khurana credits Jensen's influence at Rochester and Harvard with changing the focus of management training from the “higher aims” of institutional economists to the “hired hands” of a renewed neoclassical theory. Jensen took pains to make clear that the objective of firm management was to maximize total enterprise value (the market value of debt plus equity). In Khurana's telling of the story, however, agency theory reduced corporate managers and their “captured” regulators to self-interested opportunists and narrowed managerial responsibilities to “the maximization of stock price.”12</p><p>The neoclassical theory of the firm developed by Jensen and Meckling focused on three mechanisms for managing the agency conflict between managers and owners of the firm: (1) monitoring managerial performance, (2) providing economic incentives, and (3) promoting an active market for corporate control. The first mechanism incorporated accounting disclosures, internal control systems, and a professional board of directors. The second mechanism incorporated powerful financial incentives that aligned the financial interests of managers with shareholders. The third mechanism incorporated the threat that poorly performing management “insiders” would be replaced by efficiency- and profit-oriented “outsiders.” Jensen blamed the economic stagnation of the 1970s and early 1980s to top management's opportunistic pursuit of growth and diversification. The solution, according to Jensen, was to subject these managers to the discipline of the financial markets.</p><p>By promoting a view of managers as opportunistic agents pursuing an agenda at odds with investors, Jensen harkened back to an earlier era in America. During the second industrial revolution, investors like J. P. Morgan took large debt and equity positions in public companies and often participated in stock price manipulation and strategic decision-making. Morgan himself famously quipped, “I owe the public nothing.” In a similarly provocative spirit, Milton Friedman published his famous article in the <i>New York Times Magazine</i> in 1970 arguing that “the social responsibility of business is to increase its profits.”</p><p>According to Khurana, Jensen viewed Friedman's article as “a sign of growing academic skepticism about managerialism and an important cultural event in its own right.”13 In what we characterize as his second act, Jensen came to doubt the effectiveness of corporate governance and management control and looked to economic incentives and the market for corporate control to motivate managers to act in the best interest of shareholders. As Cheffins argues in his tribute, Jensen's writings in the popular press during this time encouraged a large wave of takeover and restructuring activity in America in the 1980s as well as a dramatic increase in CEO compensation.14</p><p>The dramatic increase in CEO compensation during this time was also heralded by Jensen's four-decade collaboration with Kevin Murphy. In their seminal paper published in 1990 in the <i>Journal of Political Economy</i>, Jensen and Murphy argued that executive compensation was not sufficiently “high-powered.”15 In particular, they argued that executive compensation should take the form of increased stock ownership or be tied substantially to the stock price of the firm. In response, corporate boards dramatically increased the financial incentives of top executives. Between 1992 and 2000, the average inflation-adjusted pay of CEOs at S&P 500 firms climbed from $3.5 million to $14.7 million.16 This increase in CEO pay, which included shares of stock granted as well as stock options, far outpaced the growth in average employee pay. As a result, the ratio of average CEO pay to average worker pay at these large companies grew from 140:1 to 500:1.17</p><p>Jensen draws direct parallels between the merger boom of the 1980s and the merger activity during the second industrial revolution in America. First, he argues that in both periods the capital markets played a major role in eliminating excess capacity and increasing profit for shareholders. Second, he argues that the takeover specialists in both periods were disparaged by managers, policy makers, and the press. He directly associates the takeover specialists of the 1980s with “the so-called Robber Barons” of the late nineteenth century. Third, he states that in both periods “the criticism was followed by public policy changes that restricted the capital markets: in the nineteenth century the passage of antitrust laws restricting combination, and in the late 1980s the renewed regulation of the credit markets, antitakeover legislation, and court decisions that restricted the market for corporate control.” Jensen concludes that corporate governance and managerial control failed to provide the same discipline and productivity as the market for corporate control.20</p><p>In the following section, we discuss how Jensen answered his own call for further research regarding the theory of the firm in his third and final act.</p><p>In 2000, Jensen stepped down from his position as Jesse Isidor Straus Professor of Business Administration at Harvard University and retired from academia. Far from ending his research on the theory of the firm, however, Jensen simply entered a new phase of his research. He immediately went to work for Michael Porter's management strategy company, Monitor Group (now Monitor Deloitte), where he put his theory of the firm to practical use from 2000 to 2009.</p><p>The paucity of coverage given to Jensen's research efforts after 2000 (they aren't even mentioned on his webpage on Wikipedia) adds to the mystery surrounding his final views of the theory of the firm. Most researchers in finance and accounting are strangely unaware of Jensen's shift in views later in life. We emphasize the third act of Jensen's career in our tribute for the following reasons: (1) prior tributes have ignored or shortchanged this highly productive period in Jensen's life; (2) the lack of coverage regarding this period has clouded Jensen's legacy and caused us to want to “set the record straight”; and (3) both of us have drawn inspiration from Jensen's later research regarding the corporation and the role of management.</p><p>In Jensen's attempt to reform people, he returned to the underlying behavioral assumptions of his theory of the firm. He never abandoned the conflict of interest at the core of the public corporate form, nor did he immediately embrace integrity as a replacement for self-interest or apply useful aspects of Freeman's stakeholder theory. In articles published in 2001 and 2002, in fact, Jensen showed his continued skepticism about two managerial controls commonly used in practice: the use of participative budgeting and tying bonuses to performance relative to the budget because it invited and indeed encouraged managers to “lie,”24 and the use of the balanced scorecard in evaluating managerial performance because of its foundation in stakeholder theory and tendency to cause confusion about the corporate mission of long-run value maximization (an idea Jensen insisted on to the last).25</p><p>The first public signs of a shift in Jensen's thinking appeared in 2004, when he partnered with Werner Erhard to develop a leadership course that emphasized integrity as a necessary ingredient to the workability of an organization (what Jensen liked to call a “new factor” in the corporate productivity function). Lemann describes how Jensen's oldest daughter invited him to attend one of Erhard's seminars called “Landmark Forum” as a way of reconciling their broken relationship.27 Jensen became actively involved in Landmark soon afterward and began to work with Erhard and another Landmark executive, Steve Zaffron. Together with Erhard and Zaffron, Jensen developed a positive economic model of integrity and began to circulate it as a working paper for further discussion.28</p><p>While some members of the Chicago School shrugged off the global market crash of 2007–08 as just a normal part of free markets,30 Jensen viewed the crash as a threat to free-market capitalism itself and blamed his own narrow theory of the firm. In his third and final act, therefore, Jensen joined Erhard in a decade of research “to seriously confront the unconfronted (and often even hidden) cost of our own and others’ out-of-integrity behavior.” But again, Jensen did not turn his back on the public corporation as the engine of value creation for the firm and the economy. Instead, he joined his co-authors in incorporating integrity into his economic theory of the firm while continuing his earlier efforts to incorporate useful aspects of stakeholder theory into his overarching goal of long-run value maximization.</p><p>In attempting to throw off the straitjacket of narrow self-interest, however, Jensen was unable or unwilling to wander far from the realm of positive economics. This is reflected in the positive model of integrity developed by Erhard, Jensen, and Zaffron. Because of their commitment to positive economics, Jensen and his co-authors ignored all definitions of integrity with normative implications and focused on a definition from engineering. In particular, they defined integrity as “the state of being whole, complete, unbroken, unimpaired, sound, perfect condition,” which they argued was empirically observable and, importantly, a purely positive phenomenon.</p><p>Although Lemann's book also emphasizes Jensen's ground-breaking research in the later years of his life, it takes a rather unflattering view of Jensen as the embodiment of “the transaction man.” In a positive but perspective-correcting review, Don Chew acknowledges that “Jensen's eye-catching collaboration with Werner Erhard and the Landmark Group after leaving the Harvard Business School in the early 2000s took a lot of his colleagues by surprise.” But Chew takes strong exception to Lemann's suggestion that Jensen ever regretted, recanted, or viewed with anything but pride, his earlier analysis of and solutions to the traditional principal-agent problem, including his core belief in the social benefits of a vigorous, well-functioning market for corporate control.</p><p>In harmony with Chew's characterization of Jensen's research in this later period, we have benefitted from Jensen's collaboration with Erhard in our own research on the theory of the firm. We argue that value creation and knowledge building in the firm are opposite sides of the same coin. Our pragmatic theory of the firm views knowledge-building proficiency as the critical determinant of a company's long-term performance. Hence, our theory incorporates a knowledge-building loop as a needed analytical tool to better understand the knowledge-building process. We employ this knowledge building loop to dissect the key ideas developed by Erhard and Jensen to improve a firm's performance by upgrading management's leadership skills.</p><p>Despite the deeply philosophical language, the contents of the course are pragmatic and highly useful. Erhard and Jensen's goal is to turn students taking the course into leaders. “Acting” the part of a leader is not the same as “being” one, and would-be followers are quick to perceive the difference.</p><p>Erhard and Jensen view the firm as a holistic system in which knowledge building continually occurs as an integral part of managers and employees living and working with one another. This leads to the foundational observation that employees’ performance is profoundly influenced and affected by their perceptions of the firm, its people, and their collective capabilities. This is a hand-in-glove fit with the pragmatic theory of the firm. Figure 1, which displays the knowledge-building loop from our framework, also offers a useful way of understanding the OPM.</p><p>As shown in Figure 1, the <i>knowledge base</i> contains assumptions of varying degrees of reliability. One's <i>worldview</i> reflects not only one's training and experience but also insights gained from traversing the knowledge building loop to achieve one's <i>purposes</i>. As for <i>perceptions</i>, our brains store past experiences to facilitate predictions via analogy to the past. Language is perception's silent partner and has a potentially subversive influence in camouflaging instead of revealing assumptions. This in turn means that the reliability of linear cause-and-effect thinking, when applied to the physical universe, can lead decision-makers to a false sense of confidence when applied to complex systems that involve human behavior. (In our framework, fast and effective traversing of the knowledge building loop provides useful <i>feedback</i> that enables one to become more proficient in taking <i>actions</i> that produce desired <i>consequences</i>.)</p><p>Our reading of the SSRN working papers by Erhard, Jensen, and colleagues confirms their agreement with the key takeaways of the knowledge-building loop illustrated in Figure 1. This includes the importance of asking better questions, using effective language, and applying systems thinking. The bullet points listed in the box inset below summarize the key ideas covered in the OPM course,34 and demonstrate how they are remarkably consistent with the components of the knowledge-building loop in our pragmatic theory of the firm.</p><p>We conclude that the third act of Jensen's illustrious career was highly productive and provided useful insights for extending the theory of the firm. In particular, Jensen developed and promoted a radically improved model for predicting how people perform, with the goal of orchestrating change that can substantially improve performance while sustaining win-win relationships. Jensen had come full circle from criticizing leadership that serves its self-interest over organizational effectiveness to laying out a practical roadmap for achieving great leadership. In contrast to the behavioral assumptions of agency theory, however, Jensen's leadership training emphasized integrity as well as useful aspects of stakeholder theory.</p><p>In this tribute to Michael C. Jensen, we highlight three phases or “acts” in his thinking regarding the public corporation and the role of management. In his first act, Jensen built on the neoclassical economic theory of the Chicago School to develop a theory of the firm that gave management a role. In his second act, Jensen emphasized the market for corporate control and financial incentives as effective controls for opportunistic self-interest. We focus on Jensen's third act, where he attempted to revise his theory by incorporating integrity and stakeholder perspectives and developed a highly innovative educational program for leadership training. As such, we contribute to Jensen's legacy by clarifying his final views on the theory of the firm.</p><p>Despite the dramatic changes we observe across the three acts of Jensen's career, we identify a continuity of thought that provides a path forward for future development in the theory of the firm. In each act, for example, we find Jensen building on previous insights gleaned from applying neoclassical economic theory to the firm. In particular, Jensen's efforts to incorporate integrity, useful aspects of stakeholder theory, and leadership training later in life built on previous insights from neoclassical economic theory. In contrast to Jensen's commitment to positive economics, however, agency researchers have recently used Adam Smith's moral theory to incorporate shared values and social norms into the theory of the firm.37 If these efforts continue and bear fruit, Jensen's efforts to extend his theory of the firm later in life may turn out to be his greatest legacy.</p>","PeriodicalId":46789,"journal":{"name":"Journal of Applied Corporate Finance","volume":"36 3","pages":"117-125"},"PeriodicalIF":1.4000,"publicationDate":"2024-09-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/jacf.12620","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Applied Corporate Finance","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/jacf.12620","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

Michael Cole Jensen (1939–2024) passed away on April 2, 2024 in Sarasota, Florida. A number of fitting tributes have appeared celebrating the life of one of the world's most productive and influential financial economists. A tribute to Jensen by Eugene Fama on the University of Chicago website ProMarket emphasizes how Jensen's research contributions put him in the highest echelons of academic finance and economics. Fama cites several of Jensen's seminal papers, including his 1976 paper coauthored with William Meckling, “Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure.”1 Jensen's paper with Meckling became the most heavily cited paper in the corporate finance literature and established agency theory as the dominant theory of the firm in finance and accounting. Fama also highlights Jensen's role in the transformation of finance into a scientific discipline, noting that he founded the Journal of Financial Economics in 1974 and edited it for over 20 years to drag the Journal of Finance “into the era of scientific research.” Finally, Fama highlights Jensen's leadership and foresight in launching the Social Science Research Network (SSRN) in 1994 to advance research across the social sciences.2

Another tribute to Jensen on ProMarket by Cambridge Law Professor Brian Cheffins suggests that Jensen's thinking on the public corporation underwent a 180-degree turn. In Cheffins's account, Jensen began his career as a strong advocate of the corporation as a driver of innovation and growth in the economy, calling it “an awesome social invention” in his seminal article with Meckling. After the economic stagnation and rampant inflation of the 1970s, however, Jensen allegedly became a fierce critic of the corporation, expressing skepticism about internal corporate systems and emphasizing the effectiveness of the market for corporate control to discipline manager opportunism. Cheffins highlights Jensen's promotion of the corporate takeover boom of the 1980s and the proliferation of incentive pay for executives based on stock options and earnings targets.

When the takeover boom suddenly halted in the 1990s, Cheffins notes that Jensen blamed executives and politicians who had put up roadblocks to corporate takeovers. Jensen also criticized self-serving managers and compliant boards who had used incentive pay to shield executives from market risk while adding significantly to their total compensation. Yet, public corporations continued to grow in number and size and were a major contributor to strong economic growth and soaring stock prices throughout the 1990s. But in Cheffins’ view, for all the accomplishments of US public companies, “there would be no reversal of Jensen's 180 degree turn regarding the public company.”3

In contrast to prior tributes, we focus on Jensen's contributions to the theory of the firm over his illustrious career. We argue that his contributions in this area represent the greatest and yet, in some respects, the most misunderstood part of Jensen's legacy. We identify three phases or “acts” in Jensen's thinking regarding the public corporation and the role of management. Consistent with Cheffins’ tribute, we argue that Jensen had a 180-degree turn in his thinking after the economic stagnation of the 1970s and became a fierce critic of certain practices of the public corporation. However, we argue that Jensen renewed (if indeed he ever completely lost) his confidence in the public corporation later in life. That renewed confidence came with the realization that his original theory of the firm was incomplete. We focus on Jensen's third act, where he attempted to revise his theory by incorporating integrity and stakeholder perspectives and developed a highly innovative educational program for leadership training. Despite the dramatic changes we observe across these three acts, however, we identify a continuity in Jensen's thought that provides a path forward for future development in the theory of the firm to address the challenges of modern capitalism.

Jensen received his PhD at the University of Chicago in 1968, at a time when the economics department had already pivoted from the institutional economics of Thorstein Veblen and Frank Knight to the neoclassical economics of Milton Friedman and George Stigler. His dissertation, which was supervised by Merton Miller, developed a method of measuring fund manager performance called Jensen's alpha and was later published in The Journal of Finance.4 Through his association with Miller and Eugene Fama at Chicago, Jensen's early work focused on market efficiency, the capital asset pricing model (CAPM), and market reactions to financial information releases. For example, he coauthored a 1969 paper with Fama, Lawrence Fisher, and Richard Roll establishing the event-study method that became the standard in capital market studies in finance and accounting.5

Most academic researchers, however, associate Jensen's early career with the powerful theory of the firm he developed with William Meckling called agency theory. Previous theories of the firm used the marginal analysis presented by Alfred Marshall (1842–1924) in his early synthesis of neoclassical economics at Cambridge University. It was under Marshall's influence that Cambridge dropped political economy from the moral sciences in 1903 before expunging the label “political” in its attempts to make the field of economics an objective science.6 Based on Marshall's price theory, economists initially modeled the firm as a set of cost and demand curves categorized by market structure (whether perfect competition, pure monopoly, monopolistic competition, or some other intermediate variation thereof). The economic function of a firm was said to be to combine economic resources (plant, machinery, labor, etc.) in order to produce goods and services demanded by consumers. The first task of a theory of the firm, therefore, is to explain why firm coordination is superior to market coordination.

In his seminal paper published in 1937 entitled, “The Nature of the Firm,” Ronald Coase (1910–2013) argued that firms emerge from a competitive process as the most efficient, or least-cost, means of coordinating economic activity. Coase also argued that firm size is influenced by rising marginal costs of organization and supervision, so a firm will eventually stop growing when the marginal costs rise to meet the marginal benefits.7

In contrast to previous neoclassical theories, Jensen and Meckling viewed the firm as a “nexus of contracts” among all the different stakeholders with claims on the firm. Their theory of the firm focused on the agency relationship that arises when a principal hires an agent to perform some task that involves the delegation of decision-making authority. Jensen argued that agency relationships exist in all organizations and across all levels of management, including the relationship between shareholders and managers of a public corporation. Given the traditional assumptions of information asymmetry and self-interested agents, the theory characterized the principal's problem as choosing some combination of formal contracting and financial incentives to control opportunistic behavior on the part of agents to maximize the wealth of the firm's shareholders (as the residual claimants).

Like previous neoclassical theories, agency theory assumed that individuals have a well-defined utility function with preferences only for wealth and leisure. Although Jensen and Meckling themselves made serious efforts to investigate alternative models of human behavior,8 the Jensen-Meckling agency framework nevertheless relied on self-interested maximizing behavior to make the theory tractable for their formal modeling and theorizing. The underlying behavioral assumptions of agency theory contrasted sharply with the assumptions of institutional economic theory, which characterized economic agents as influenced by nonfinancial factors such as social norms, institutions, and culture. Institutional economists had established business schools in the new research university in the late 19th century and their theoretical perspective still dominated the nation's business schools.9

Jensen played a central role in promoting agency theory through his own research and in his role as editor of the Journal of Financial Economics. Further, he promoted the theory in practitioner-oriented outlets such as the Harvard Business Review and the Wall Street Journal. Finally, Jensen promoted his theory of the firm to students in his MBA courses at the University of Rochester and later at Harvard. Between 1967 and 1988, Jensen taught finance and business administration at the University of Rochester Graduate School of Business Administration. He joined the Harvard Business School on a half-time appointment in 1985, dividing his time between Rochester and Harvard, before taking a full-time appointment at Harvard in 1988.

Khurana credits Jensen's influence at Rochester and Harvard with changing the focus of management training from the “higher aims” of institutional economists to the “hired hands” of a renewed neoclassical theory. Jensen took pains to make clear that the objective of firm management was to maximize total enterprise value (the market value of debt plus equity). In Khurana's telling of the story, however, agency theory reduced corporate managers and their “captured” regulators to self-interested opportunists and narrowed managerial responsibilities to “the maximization of stock price.”12

The neoclassical theory of the firm developed by Jensen and Meckling focused on three mechanisms for managing the agency conflict between managers and owners of the firm: (1) monitoring managerial performance, (2) providing economic incentives, and (3) promoting an active market for corporate control. The first mechanism incorporated accounting disclosures, internal control systems, and a professional board of directors. The second mechanism incorporated powerful financial incentives that aligned the financial interests of managers with shareholders. The third mechanism incorporated the threat that poorly performing management “insiders” would be replaced by efficiency- and profit-oriented “outsiders.” Jensen blamed the economic stagnation of the 1970s and early 1980s to top management's opportunistic pursuit of growth and diversification. The solution, according to Jensen, was to subject these managers to the discipline of the financial markets.

By promoting a view of managers as opportunistic agents pursuing an agenda at odds with investors, Jensen harkened back to an earlier era in America. During the second industrial revolution, investors like J. P. Morgan took large debt and equity positions in public companies and often participated in stock price manipulation and strategic decision-making. Morgan himself famously quipped, “I owe the public nothing.” In a similarly provocative spirit, Milton Friedman published his famous article in the New York Times Magazine in 1970 arguing that “the social responsibility of business is to increase its profits.”

According to Khurana, Jensen viewed Friedman's article as “a sign of growing academic skepticism about managerialism and an important cultural event in its own right.”13 In what we characterize as his second act, Jensen came to doubt the effectiveness of corporate governance and management control and looked to economic incentives and the market for corporate control to motivate managers to act in the best interest of shareholders. As Cheffins argues in his tribute, Jensen's writings in the popular press during this time encouraged a large wave of takeover and restructuring activity in America in the 1980s as well as a dramatic increase in CEO compensation.14

The dramatic increase in CEO compensation during this time was also heralded by Jensen's four-decade collaboration with Kevin Murphy. In their seminal paper published in 1990 in the Journal of Political Economy, Jensen and Murphy argued that executive compensation was not sufficiently “high-powered.”15 In particular, they argued that executive compensation should take the form of increased stock ownership or be tied substantially to the stock price of the firm. In response, corporate boards dramatically increased the financial incentives of top executives. Between 1992 and 2000, the average inflation-adjusted pay of CEOs at S&P 500 firms climbed from $3.5 million to $14.7 million.16 This increase in CEO pay, which included shares of stock granted as well as stock options, far outpaced the growth in average employee pay. As a result, the ratio of average CEO pay to average worker pay at these large companies grew from 140:1 to 500:1.17

Jensen draws direct parallels between the merger boom of the 1980s and the merger activity during the second industrial revolution in America. First, he argues that in both periods the capital markets played a major role in eliminating excess capacity and increasing profit for shareholders. Second, he argues that the takeover specialists in both periods were disparaged by managers, policy makers, and the press. He directly associates the takeover specialists of the 1980s with “the so-called Robber Barons” of the late nineteenth century. Third, he states that in both periods “the criticism was followed by public policy changes that restricted the capital markets: in the nineteenth century the passage of antitrust laws restricting combination, and in the late 1980s the renewed regulation of the credit markets, antitakeover legislation, and court decisions that restricted the market for corporate control.” Jensen concludes that corporate governance and managerial control failed to provide the same discipline and productivity as the market for corporate control.20

In the following section, we discuss how Jensen answered his own call for further research regarding the theory of the firm in his third and final act.

In 2000, Jensen stepped down from his position as Jesse Isidor Straus Professor of Business Administration at Harvard University and retired from academia. Far from ending his research on the theory of the firm, however, Jensen simply entered a new phase of his research. He immediately went to work for Michael Porter's management strategy company, Monitor Group (now Monitor Deloitte), where he put his theory of the firm to practical use from 2000 to 2009.

The paucity of coverage given to Jensen's research efforts after 2000 (they aren't even mentioned on his webpage on Wikipedia) adds to the mystery surrounding his final views of the theory of the firm. Most researchers in finance and accounting are strangely unaware of Jensen's shift in views later in life. We emphasize the third act of Jensen's career in our tribute for the following reasons: (1) prior tributes have ignored or shortchanged this highly productive period in Jensen's life; (2) the lack of coverage regarding this period has clouded Jensen's legacy and caused us to want to “set the record straight”; and (3) both of us have drawn inspiration from Jensen's later research regarding the corporation and the role of management.

In Jensen's attempt to reform people, he returned to the underlying behavioral assumptions of his theory of the firm. He never abandoned the conflict of interest at the core of the public corporate form, nor did he immediately embrace integrity as a replacement for self-interest or apply useful aspects of Freeman's stakeholder theory. In articles published in 2001 and 2002, in fact, Jensen showed his continued skepticism about two managerial controls commonly used in practice: the use of participative budgeting and tying bonuses to performance relative to the budget because it invited and indeed encouraged managers to “lie,”24 and the use of the balanced scorecard in evaluating managerial performance because of its foundation in stakeholder theory and tendency to cause confusion about the corporate mission of long-run value maximization (an idea Jensen insisted on to the last).25

The first public signs of a shift in Jensen's thinking appeared in 2004, when he partnered with Werner Erhard to develop a leadership course that emphasized integrity as a necessary ingredient to the workability of an organization (what Jensen liked to call a “new factor” in the corporate productivity function). Lemann describes how Jensen's oldest daughter invited him to attend one of Erhard's seminars called “Landmark Forum” as a way of reconciling their broken relationship.27 Jensen became actively involved in Landmark soon afterward and began to work with Erhard and another Landmark executive, Steve Zaffron. Together with Erhard and Zaffron, Jensen developed a positive economic model of integrity and began to circulate it as a working paper for further discussion.28

While some members of the Chicago School shrugged off the global market crash of 2007–08 as just a normal part of free markets,30 Jensen viewed the crash as a threat to free-market capitalism itself and blamed his own narrow theory of the firm. In his third and final act, therefore, Jensen joined Erhard in a decade of research “to seriously confront the unconfronted (and often even hidden) cost of our own and others’ out-of-integrity behavior.” But again, Jensen did not turn his back on the public corporation as the engine of value creation for the firm and the economy. Instead, he joined his co-authors in incorporating integrity into his economic theory of the firm while continuing his earlier efforts to incorporate useful aspects of stakeholder theory into his overarching goal of long-run value maximization.

In attempting to throw off the straitjacket of narrow self-interest, however, Jensen was unable or unwilling to wander far from the realm of positive economics. This is reflected in the positive model of integrity developed by Erhard, Jensen, and Zaffron. Because of their commitment to positive economics, Jensen and his co-authors ignored all definitions of integrity with normative implications and focused on a definition from engineering. In particular, they defined integrity as “the state of being whole, complete, unbroken, unimpaired, sound, perfect condition,” which they argued was empirically observable and, importantly, a purely positive phenomenon.

Although Lemann's book also emphasizes Jensen's ground-breaking research in the later years of his life, it takes a rather unflattering view of Jensen as the embodiment of “the transaction man.” In a positive but perspective-correcting review, Don Chew acknowledges that “Jensen's eye-catching collaboration with Werner Erhard and the Landmark Group after leaving the Harvard Business School in the early 2000s took a lot of his colleagues by surprise.” But Chew takes strong exception to Lemann's suggestion that Jensen ever regretted, recanted, or viewed with anything but pride, his earlier analysis of and solutions to the traditional principal-agent problem, including his core belief in the social benefits of a vigorous, well-functioning market for corporate control.

In harmony with Chew's characterization of Jensen's research in this later period, we have benefitted from Jensen's collaboration with Erhard in our own research on the theory of the firm. We argue that value creation and knowledge building in the firm are opposite sides of the same coin. Our pragmatic theory of the firm views knowledge-building proficiency as the critical determinant of a company's long-term performance. Hence, our theory incorporates a knowledge-building loop as a needed analytical tool to better understand the knowledge-building process. We employ this knowledge building loop to dissect the key ideas developed by Erhard and Jensen to improve a firm's performance by upgrading management's leadership skills.

Despite the deeply philosophical language, the contents of the course are pragmatic and highly useful. Erhard and Jensen's goal is to turn students taking the course into leaders. “Acting” the part of a leader is not the same as “being” one, and would-be followers are quick to perceive the difference.

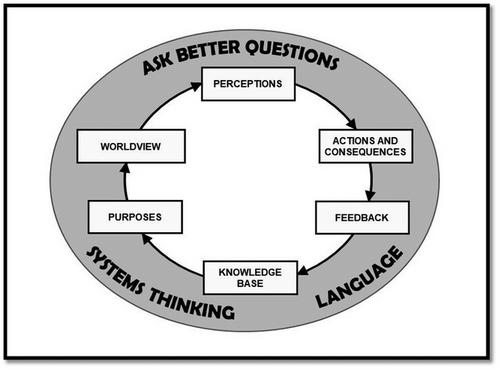

Erhard and Jensen view the firm as a holistic system in which knowledge building continually occurs as an integral part of managers and employees living and working with one another. This leads to the foundational observation that employees’ performance is profoundly influenced and affected by their perceptions of the firm, its people, and their collective capabilities. This is a hand-in-glove fit with the pragmatic theory of the firm. Figure 1, which displays the knowledge-building loop from our framework, also offers a useful way of understanding the OPM.

As shown in Figure 1, the knowledge base contains assumptions of varying degrees of reliability. One's worldview reflects not only one's training and experience but also insights gained from traversing the knowledge building loop to achieve one's purposes. As for perceptions, our brains store past experiences to facilitate predictions via analogy to the past. Language is perception's silent partner and has a potentially subversive influence in camouflaging instead of revealing assumptions. This in turn means that the reliability of linear cause-and-effect thinking, when applied to the physical universe, can lead decision-makers to a false sense of confidence when applied to complex systems that involve human behavior. (In our framework, fast and effective traversing of the knowledge building loop provides useful feedback that enables one to become more proficient in taking actions that produce desired consequences.)

Our reading of the SSRN working papers by Erhard, Jensen, and colleagues confirms their agreement with the key takeaways of the knowledge-building loop illustrated in Figure 1. This includes the importance of asking better questions, using effective language, and applying systems thinking. The bullet points listed in the box inset below summarize the key ideas covered in the OPM course,34 and demonstrate how they are remarkably consistent with the components of the knowledge-building loop in our pragmatic theory of the firm.

We conclude that the third act of Jensen's illustrious career was highly productive and provided useful insights for extending the theory of the firm. In particular, Jensen developed and promoted a radically improved model for predicting how people perform, with the goal of orchestrating change that can substantially improve performance while sustaining win-win relationships. Jensen had come full circle from criticizing leadership that serves its self-interest over organizational effectiveness to laying out a practical roadmap for achieving great leadership. In contrast to the behavioral assumptions of agency theory, however, Jensen's leadership training emphasized integrity as well as useful aspects of stakeholder theory.

In this tribute to Michael C. Jensen, we highlight three phases or “acts” in his thinking regarding the public corporation and the role of management. In his first act, Jensen built on the neoclassical economic theory of the Chicago School to develop a theory of the firm that gave management a role. In his second act, Jensen emphasized the market for corporate control and financial incentives as effective controls for opportunistic self-interest. We focus on Jensen's third act, where he attempted to revise his theory by incorporating integrity and stakeholder perspectives and developed a highly innovative educational program for leadership training. As such, we contribute to Jensen's legacy by clarifying his final views on the theory of the firm.

Despite the dramatic changes we observe across the three acts of Jensen's career, we identify a continuity of thought that provides a path forward for future development in the theory of the firm. In each act, for example, we find Jensen building on previous insights gleaned from applying neoclassical economic theory to the firm. In particular, Jensen's efforts to incorporate integrity, useful aspects of stakeholder theory, and leadership training later in life built on previous insights from neoclassical economic theory. In contrast to Jensen's commitment to positive economics, however, agency researchers have recently used Adam Smith's moral theory to incorporate shared values and social norms into the theory of the firm.37 If these efforts continue and bear fruit, Jensen's efforts to extend his theory of the firm later in life may turn out to be his greatest legacy.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: