Melody Harvey, Cliff A. Robb, Christopher L. Peterson

{"title":"Law and order? Associations between payday lending prohibition and alternative financial services use by degree of enforcement","authors":"Melody Harvey, Cliff A. Robb, Christopher L. Peterson","doi":"10.1111/joca.12583","DOIUrl":null,"url":null,"abstract":"<p>Sixteen jurisdictions in the United States prohibit payday lending through stringent usury laws or well-established nonprofitable 36% interest rate caps. Yet over one in 10 consumers residing in these jurisdictions borrowed payday loans in the past 5 years. This raises questions about actual policy implementation and enforcement. We employ data from the 2018 National Financial Capability Study to investigate if associations between payday lending prohibitions and payday borrowing differ by degree of enforcement. We find that nuances in degree of enforcement among restrictive states are not associated with payday borrowing likelihoods. However, these nuances appear when examining payday borrowing frequency, particularly when controlling for consumers' financial circumstances and when conditioning on alternative financial services consumers. We consistently note the highest borrowing behaviors for states sans regulation. Policymakers may consider strengthening enforcement in cases where the primary goal is preventing or reducing payday borrowing.</p>","PeriodicalId":47976,"journal":{"name":"Journal of Consumer Affairs","volume":"58 2","pages":"538-557"},"PeriodicalIF":3.2000,"publicationDate":"2024-04-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/joca.12583","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Consumer Affairs","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/joca.12583","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 0

Abstract

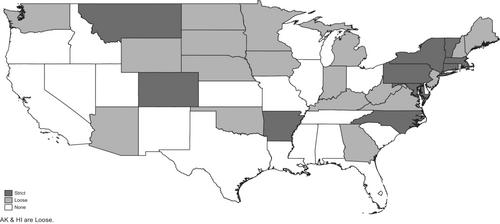

Sixteen jurisdictions in the United States prohibit payday lending through stringent usury laws or well-established nonprofitable 36% interest rate caps. Yet over one in 10 consumers residing in these jurisdictions borrowed payday loans in the past 5 years. This raises questions about actual policy implementation and enforcement. We employ data from the 2018 National Financial Capability Study to investigate if associations between payday lending prohibitions and payday borrowing differ by degree of enforcement. We find that nuances in degree of enforcement among restrictive states are not associated with payday borrowing likelihoods. However, these nuances appear when examining payday borrowing frequency, particularly when controlling for consumers' financial circumstances and when conditioning on alternative financial services consumers. We consistently note the highest borrowing behaviors for states sans regulation. Policymakers may consider strengthening enforcement in cases where the primary goal is preventing or reducing payday borrowing.

期刊介绍:

The ISI impact score of Journal of Consumer Affairs now places it among the leading business journals and one of the top handful of marketing- related publications. The immediacy index score, showing how swiftly the published studies are cited or applied in other publications, places JCA seventh of those same 77 journals. More importantly, in these difficult economic times, JCA is the leading journal whose focus for over four decades has been on the interests of consumers in the marketplace. With the journal"s origins in the consumer movement and consumer protection concerns, the focus for papers in terms of both research questions and implications must involve the consumer"s interest and topics must be addressed from the consumers point of view.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: