{"title":"Audit simulation and learning styles: Enhancing students' experiential learning and performance at a MENA university","authors":"Nader Elsayed, Mostafa Kamal Hassan","doi":"10.1111/ijau.12345","DOIUrl":null,"url":null,"abstract":"<p>Drawing on experiential learning theory (ELT), this study (1) explores students' perceived benefits of experiencing different learning styles through an audit simulation (AS) assignment and (2) analyses its role in enhancing students' performance at a Middle East and North Africa (MENA) university. The study compares students' performance across two different periods, 2019 and 2022, with 46 and 48 participants, respectively, independently completing a questionnaire of six open-ended questions paired with follow-up feedback, the instructor's observations and the analyses of students' grades. Our study findings indicate that the AS assignment enabled students to effectively experience different learning styles at different times during the AS learning process. They visualised an authentic AS experience by critically analysing and practically evaluating AS documents while showing strong preferences for initiating new experiences. It also reveals an improvement in students' grades after the AS implementation. Our study has theoretical implications relating to cognitive and constructivist learning, learning transfer and ethics awareness, as well as practical implications in audit education, skill development, teamwork, professional development, auditors' evaluation and curriculum assessment in other disciplines than auditing.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"28 4","pages":"632-651"},"PeriodicalIF":1.4000,"publicationDate":"2024-03-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12345","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12345","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

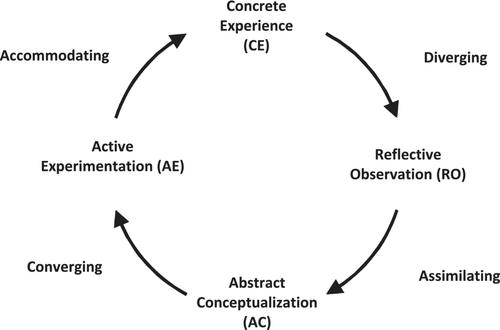

Drawing on experiential learning theory (ELT), this study (1) explores students' perceived benefits of experiencing different learning styles through an audit simulation (AS) assignment and (2) analyses its role in enhancing students' performance at a Middle East and North Africa (MENA) university. The study compares students' performance across two different periods, 2019 and 2022, with 46 and 48 participants, respectively, independently completing a questionnaire of six open-ended questions paired with follow-up feedback, the instructor's observations and the analyses of students' grades. Our study findings indicate that the AS assignment enabled students to effectively experience different learning styles at different times during the AS learning process. They visualised an authentic AS experience by critically analysing and practically evaluating AS documents while showing strong preferences for initiating new experiences. It also reveals an improvement in students' grades after the AS implementation. Our study has theoretical implications relating to cognitive and constructivist learning, learning transfer and ethics awareness, as well as practical implications in audit education, skill development, teamwork, professional development, auditors' evaluation and curriculum assessment in other disciplines than auditing.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: