How Integrated are Credit and Equity Markets? Evidence from Index Options

IF 7.6

1区 经济学

Q1 BUSINESS, FINANCE

引用次数: 0

Abstract

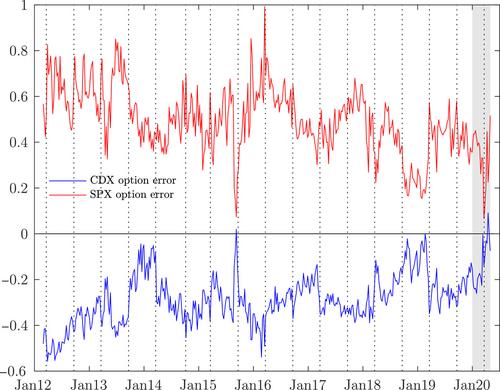

We study the extent to which credit index (CDX) options are priced consistent with S&P 500 (SPX) equity index options. We derive analytical expressions for CDX and SPX options within a structural credit-risk model with stochastic volatility and jumps using new results for pricing compound options via multivariate affine transform analysis. The model captures many aspects of the joint dynamics of CDX and SPX options. However, it cannot reconcile the relative levels of option prices, suggesting that credit and equity markets are not fully integrated. A strategy of selling CDX volatility yields significantly higher excess returns than selling SPX volatility.

信贷市场和股票市场的融合程度如何?指数期权的证据

我们研究了信贷指数(CDX)期权与 S&P 500(SPX)股票指数期权的定价一致程度。我们通过多变量仿射变换分析,利用复合期权定价的新结果,在具有随机波动率和跳跃的结构性信用风险模型中推导出 CDX 和 SPX 期权的分析表达式。该模型捕捉了 CDX 和 SPX 期权联合动态的许多方面。然而,该模型无法调和期权价格的相对水平,表明信贷市场和股票市场并未完全融合。卖出 CDX 波动率的策略产生的超额收益明显高于卖出 SPX 波动率的策略。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Journal of Finance

Multiple-

CiteScore

12.90

自引率

2.50%

发文量

88

期刊介绍:

The Journal of Finance is a renowned publication that disseminates cutting-edge research across all major fields of financial inquiry. Widely regarded as the most cited academic journal in finance, each issue reaches over 8,000 academics, finance professionals, libraries, government entities, and financial institutions worldwide. Published bi-monthly, the journal serves as the official publication of The American Finance Association, the premier academic organization dedicated to advancing knowledge and understanding in financial economics. Join us in exploring the forefront of financial research and scholarship.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: