Empirical evidence on the Euler equation for investment in the US

IF 3.1

3区 经济学

Q2 ECONOMICS

引用次数: 0

Abstract

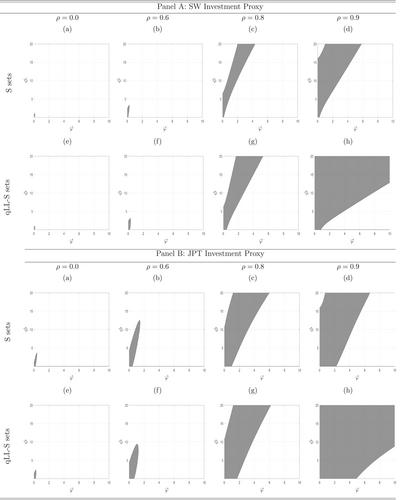

Is the typical specification of the Euler equation for investment employed in dynamic stochastic general equilibrium (DSGE) models consistent with aggregate macro data? The answer is yes using state-of-the-art econometric methods that are robust to weak instruments and exploit information in possible structural changes. Unfortunately, however, there is very little information about the values of the parameters in aggregate data because investment is unresponsive to changes in capital utilization and the real interest rate. Bayesian estimation using fully specified DSGE models is more accurate due to both informative priors and cross-equation restrictions.

美国投资欧拉方程的经验证据

摘要 动态随机一般均衡(DSGE)模型中采用的投资欧拉方程的典型规格是否与宏观总量数据一致?使用最先进的计量经济学方法,答案是肯定的,这些方法对弱工具具有稳健性,并能利用可能的结构变化信息。但遗憾的是,由于投资对资本利用率和实际利率的变化反应迟钝,因此有关总体数据中参数值的信息非常少。由于信息先验和交叉方程限制,使用完全指定的 DSGE 模型进行贝叶斯估计更为准确。

本文章由计算机程序翻译,如有差异,请以英文原文为准。

求助全文

约1分钟内获得全文

求助全文

来源期刊

Journal of Applied Econometrics

Multiple-

CiteScore

3.70

自引率

4.80%

发文量

63

期刊介绍:

The Journal of Applied Econometrics is an international journal published bi-monthly, plus 1 additional issue (total 7 issues). It aims to publish articles of high quality dealing with the application of existing as well as new econometric techniques to a wide variety of problems in economics and related subjects, covering topics in measurement, estimation, testing, forecasting, and policy analysis. The emphasis is on the careful and rigorous application of econometric techniques and the appropriate interpretation of the results. The economic content of the articles is stressed. A special feature of the Journal is its emphasis on the replicability of results by other researchers. To achieve this aim, authors are expected to make available a complete set of the data used as well as any specialised computer programs employed through a readily accessible medium, preferably in a machine-readable form. The use of microcomputers in applied research and transferability of data is emphasised. The Journal also features occasional sections of short papers re-evaluating previously published papers. The intention of the Journal of Applied Econometrics is to provide an outlet for innovative, quantitative research in economics which cuts across areas of specialisation, involves transferable techniques, and is easily replicable by other researchers. Contributions that introduce statistical methods that are applicable to a variety of economic problems are actively encouraged. The Journal also aims to publish review and survey articles that make recent developments in the field of theoretical and applied econometrics more readily accessible to applied economists in general.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: