Jakob Manthey, Inese Gobiņa, Laura Isajeva, Jarosław Neneman, Rainer Reile, Mindaugas Štelemėkas, Jürgen Rehm

{"title":"The Impact of Raising Alcohol Taxes on Government Tax Revenue: Insights from Five European Countries","authors":"Jakob Manthey, Inese Gobiņa, Laura Isajeva, Jarosław Neneman, Rainer Reile, Mindaugas Štelemėkas, Jürgen Rehm","doi":"10.1007/s40258-024-00873-5","DOIUrl":null,"url":null,"abstract":"<div><h3>Background and Objective</h3><p>Reducing the affordability of alcoholic beverages by increasing alcohol excise taxation can lead to a reduction in alcohol consumption but the impact on government alcohol excise tax revenue is poorly understood. This study aimed to (a) describe cross-country tax revenue variations and (b) investigate how changes in taxation were related to changes in government tax revenue, using data from Estonia, Germany, Latvia, Lithuania and Poland.</p><h3>Methods</h3><p>For the population aged 15 years or older, we calculated the annual per capita alcohol excise tax revenue, total tax revenue, gross domestic product and alcohol consumption. In addition to descriptive analyses, joinpoint regressions were performed to identify whether changes in alcohol excise taxation were linked to changes in alcohol excise revenue since 1999.</p><h3>Results</h3><p>In 2022, the per capita alcohol excise tax revenue was lowest in Germany (€44.2) and highest in Estonia (€218.4). In all countries, the alcohol excise tax revenue was mostly determined by spirit sales (57–72% of total alcohol tax revenue). During 2010–20, inflation-adjusted per capita alcohol excise tax revenues have declined in Germany (− 22.9%), Poland (− 19.1%) and Estonia (− 4.2%) and increased in Latvia (+ 56.8%) and Lithuania (+ 49.3%). In periods of policy non-action, alcohol consumption and tax revenue showed similar trends, but tax level increases were accompanied by increased revenue and stagnant or decreased consumption.</p><h3>Conclusions</h3><p>Increasing alcohol taxation was not linked to decreased but increased government revenue. Policymakers can increase revenue and reduce alcohol consumption and harm by increasing alcohol taxes.</p></div>","PeriodicalId":8065,"journal":{"name":"Applied Health Economics and Health Policy","volume":"22 3","pages":"363 - 374"},"PeriodicalIF":3.1000,"publicationDate":"2024-02-22","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://link.springer.com/content/pdf/10.1007/s40258-024-00873-5.pdf","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Applied Health Economics and Health Policy","FirstCategoryId":"3","ListUrlMain":"https://link.springer.com/article/10.1007/s40258-024-00873-5","RegionNum":4,"RegionCategory":"医学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

Background and Objective

Reducing the affordability of alcoholic beverages by increasing alcohol excise taxation can lead to a reduction in alcohol consumption but the impact on government alcohol excise tax revenue is poorly understood. This study aimed to (a) describe cross-country tax revenue variations and (b) investigate how changes in taxation were related to changes in government tax revenue, using data from Estonia, Germany, Latvia, Lithuania and Poland.

Methods

For the population aged 15 years or older, we calculated the annual per capita alcohol excise tax revenue, total tax revenue, gross domestic product and alcohol consumption. In addition to descriptive analyses, joinpoint regressions were performed to identify whether changes in alcohol excise taxation were linked to changes in alcohol excise revenue since 1999.

Results

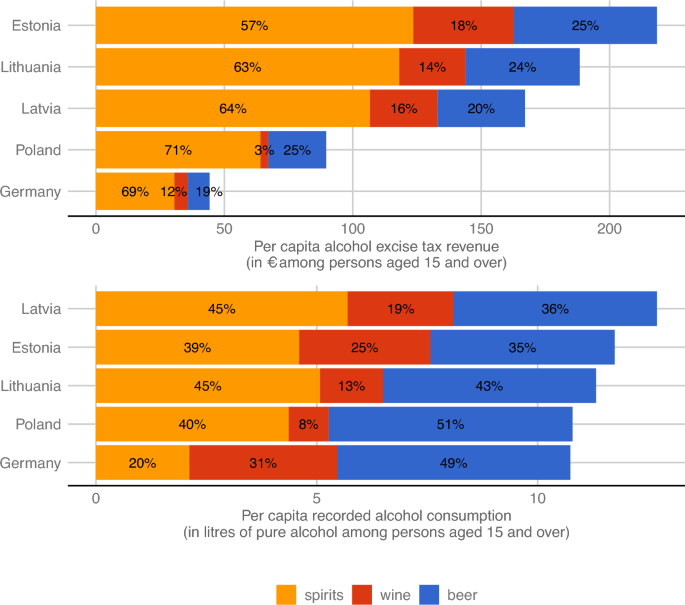

In 2022, the per capita alcohol excise tax revenue was lowest in Germany (€44.2) and highest in Estonia (€218.4). In all countries, the alcohol excise tax revenue was mostly determined by spirit sales (57–72% of total alcohol tax revenue). During 2010–20, inflation-adjusted per capita alcohol excise tax revenues have declined in Germany (− 22.9%), Poland (− 19.1%) and Estonia (− 4.2%) and increased in Latvia (+ 56.8%) and Lithuania (+ 49.3%). In periods of policy non-action, alcohol consumption and tax revenue showed similar trends, but tax level increases were accompanied by increased revenue and stagnant or decreased consumption.

Conclusions

Increasing alcohol taxation was not linked to decreased but increased government revenue. Policymakers can increase revenue and reduce alcohol consumption and harm by increasing alcohol taxes.

期刊介绍:

Applied Health Economics and Health Policy provides timely publication of cutting-edge research and expert opinion from this increasingly important field, making it a vital resource for payers, providers and researchers alike. The journal includes high quality economic research and reviews of all aspects of healthcare from various perspectives and countries, designed to communicate the latest applied information in health economics and health policy.

While emphasis is placed on information with practical applications, a strong basis of underlying scientific rigor is maintained.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: