{"title":"Internal auditing's role in preventing and detecting fraud: An empirical analysis","authors":"Annika Bonrath, Marc Eulerich","doi":"10.1111/ijau.12342","DOIUrl":null,"url":null,"abstract":"<p>Internal auditing plays a pivotal role in preventing and detecting fraudulent activities. However, the orientation and role of internal auditing in dealing with fraud risk can vary significantly across different companies. This study examines the relationship between the internal audit function (IAF) and fraud, providing new insights into the current practices of internal auditing. Using a survey dataset comprising responses from 275 Chief Audit Executives across Germany, Switzerland and Austria, we investigate factors that correlate with an increased propensity for IAFs to engage in fraud prevention and detection. Our findings suggest that a robust corporate governance environment significantly influences the extent to which the IAF is involved in preventing and detecting fraud. Shedding light on the positioning of internal auditing between management and the audit committee with respect to fraud, our results show that increased IAF involvement with management positively affects the level of activities to prevent and detect fraud, while increased IAF involvement with the audit committee has the opposite effect. Furthermore, we find that the propensity of IAFs to engage in fraud prevention and detection increases when the IAF applies technology-based auditing techniques for risk identification. Our results have implications for building appropriate protection against the steadily increasing risk of fraud within organizations, while holistically addressing the ambiguity regarding the responsibility for preventing and detecting fraud.</p>","PeriodicalId":47092,"journal":{"name":"International Journal of Auditing","volume":"28 4","pages":"615-631"},"PeriodicalIF":1.4000,"publicationDate":"2024-02-05","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijau.12342","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Auditing","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijau.12342","RegionNum":4,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

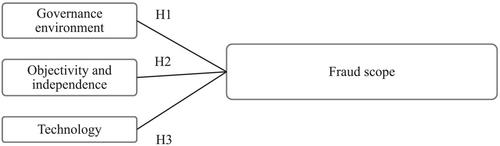

Internal auditing plays a pivotal role in preventing and detecting fraudulent activities. However, the orientation and role of internal auditing in dealing with fraud risk can vary significantly across different companies. This study examines the relationship between the internal audit function (IAF) and fraud, providing new insights into the current practices of internal auditing. Using a survey dataset comprising responses from 275 Chief Audit Executives across Germany, Switzerland and Austria, we investigate factors that correlate with an increased propensity for IAFs to engage in fraud prevention and detection. Our findings suggest that a robust corporate governance environment significantly influences the extent to which the IAF is involved in preventing and detecting fraud. Shedding light on the positioning of internal auditing between management and the audit committee with respect to fraud, our results show that increased IAF involvement with management positively affects the level of activities to prevent and detect fraud, while increased IAF involvement with the audit committee has the opposite effect. Furthermore, we find that the propensity of IAFs to engage in fraud prevention and detection increases when the IAF applies technology-based auditing techniques for risk identification. Our results have implications for building appropriate protection against the steadily increasing risk of fraud within organizations, while holistically addressing the ambiguity regarding the responsibility for preventing and detecting fraud.

期刊介绍:

In addition to communicating the results of original auditing research, the International Journal of Auditing also aims to advance knowledge in auditing by publishing critiques, thought leadership papers and literature reviews on specific aspects of auditing. The journal seeks to publish articles that have international appeal either due to the topic transcending national frontiers or due to the clear potential for readers to apply the results or ideas in their local environments. While articles must be methodologically and theoretically sound, any research orientation is acceptable. This means that papers may have an analytical and statistical, behavioural, economic and financial (including agency), sociological, critical, or historical basis. The editors consider articles for publication which fit into one or more of the following subject categories: • Financial statement audits • Public sector/governmental auditing • Internal auditing • Audit education and methods of teaching auditing (including case studies) • Audit aspects of corporate governance, including audit committees • Audit quality • Audit fees and related issues • Environmental, social and sustainability audits • Audit related ethical issues • Audit regulation • Independence issues • Legal liability and other legal issues • Auditing history • New and emerging audit and assurance issues

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: