{"title":"Affine Heston model style with self-exciting jumps and long memory","authors":"Charles Guy Njike Leunga, Donatien Hainaut","doi":"10.1007/s10436-023-00436-z","DOIUrl":null,"url":null,"abstract":"<div><p>Classic diffusion processes fail to explain asset return volatility. Many empirical findings on asset return time series, such as heavy tails, skewness and volatility clustering, suggest decomposing the volatility of an asset’s return into two components, one caused by a Brownian motion and another by a jump process. We analyze the sensitivity of European call options to memory and self-excitation parameters, underlying price, volatility and jump risks. We expand Heston’s stochastic volatility model by adding to the instantaneous asset prices, a jump component driven by a Hawkes process with a kernel function or memory kernel that is a Fourier transform of a probability measure. This kernel function defines the memory of the asset price process. For instance, if it is fast decreasing, the contagion effect between asset price jumps is limited in time. Otherwise, the processes remember the history of asset price jumps for a long period. To investigate the impact of different rates of decay or types of memory, we consider four probability measures: Laplace, Gaussian, Logistic and Cauchy. Unlike Hawkes processes with exponential kernels, the Markov property is lost but stationarity is preserved; this ensures that the unconditional expected arrival rate of the jump does not explode. In the absence of the Markov property, we use the Fourier transform representation to derive a closed form expression of a European call option price based on characteristic functions. A numerical illustration shows that our extension of the Heston model achieves a better fit of the Euro Stoxx 50 option data than the standard version.</p></div>","PeriodicalId":45289,"journal":{"name":"Annals of Finance","volume":"20 1","pages":"1 - 43"},"PeriodicalIF":0.7000,"publicationDate":"2024-01-12","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Finance","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10436-023-00436-z","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q4","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

引用次数: 0

Abstract

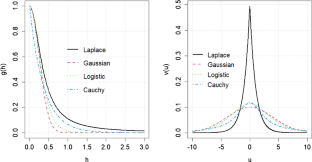

Classic diffusion processes fail to explain asset return volatility. Many empirical findings on asset return time series, such as heavy tails, skewness and volatility clustering, suggest decomposing the volatility of an asset’s return into two components, one caused by a Brownian motion and another by a jump process. We analyze the sensitivity of European call options to memory and self-excitation parameters, underlying price, volatility and jump risks. We expand Heston’s stochastic volatility model by adding to the instantaneous asset prices, a jump component driven by a Hawkes process with a kernel function or memory kernel that is a Fourier transform of a probability measure. This kernel function defines the memory of the asset price process. For instance, if it is fast decreasing, the contagion effect between asset price jumps is limited in time. Otherwise, the processes remember the history of asset price jumps for a long period. To investigate the impact of different rates of decay or types of memory, we consider four probability measures: Laplace, Gaussian, Logistic and Cauchy. Unlike Hawkes processes with exponential kernels, the Markov property is lost but stationarity is preserved; this ensures that the unconditional expected arrival rate of the jump does not explode. In the absence of the Markov property, we use the Fourier transform representation to derive a closed form expression of a European call option price based on characteristic functions. A numerical illustration shows that our extension of the Heston model achieves a better fit of the Euro Stoxx 50 option data than the standard version.

期刊介绍:

Annals of Finance provides an outlet for original research in all areas of finance and its applications to other disciplines having a clear and substantive link to the general theme of finance. In particular, innovative research papers of moderate length of the highest quality in all scientific areas that are motivated by the analysis of financial problems will be considered. Annals of Finance''s scope encompasses - but is not limited to - the following areas: accounting and finance, asset pricing, banking and finance, capital markets and finance, computational finance, corporate finance, derivatives, dynamical and chaotic systems in finance, economics and finance, empirical finance, experimental finance, finance and the theory of the firm, financial econometrics, financial institutions, mathematical finance, money and finance, portfolio analysis, regulation, stochastic analysis and finance, stock market analysis, systemic risk and financial stability. Annals of Finance also publishes special issues on any topic in finance and its applications of current interest. A small section, entitled finance notes, will be devoted solely to publishing short articles – up to ten pages in length, of substantial interest in finance. Officially cited as: Ann Finance

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: