Fernando Alvarez, Francesco Lippi, Panagiotis Souganidis

{"title":"Price Setting With Strategic Complementarities as a Mean Field Game","authors":"Fernando Alvarez, Francesco Lippi, Panagiotis Souganidis","doi":"10.3982/ECTA20797","DOIUrl":null,"url":null,"abstract":"<div>\n <p>We study the propagation of monetary shocks in a sticky-price general equilibrium economy where the firms' pricing strategy features a complementarity with the decisions of other firms. In a dynamic equilibrium, the firm's price-setting decisions depend on aggregates, which in turn depend on the firms' decisions. We cast this fixed-point problem as a Mean Field Game and prove several analytic results. We establish existence and uniqueness of the equilibrium and characterize the impulse response function (IRF) of output following an aggregate shock. We prove that strategic complementarities make the IRF larger at each horizon. We establish that complementarities may give rise to an IRF with a hump-shaped profile. As the complementarity becomes large enough, the IRF diverges, and at a critical point there is no equilibrium. Finally, we show that the amplification effect of the strategic interactions is similar across models: the Calvo model and the Golosov–Lucas model display a comparable amplification, in spite of the fact that the non-neutrality in Calvo is much larger.</p>\n </div>","PeriodicalId":50556,"journal":{"name":"Econometrica","volume":"91 6","pages":"2005-2039"},"PeriodicalIF":6.6000,"publicationDate":"2023-12-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.3982/ECTA20797","citationCount":"0","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Econometrica","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.3982/ECTA20797","RegionNum":1,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 0

Abstract

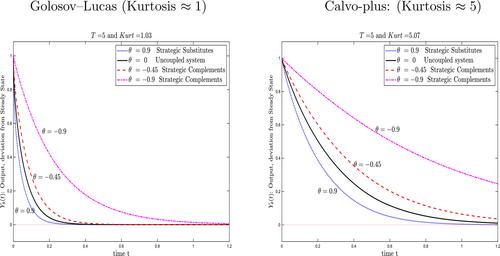

We study the propagation of monetary shocks in a sticky-price general equilibrium economy where the firms' pricing strategy features a complementarity with the decisions of other firms. In a dynamic equilibrium, the firm's price-setting decisions depend on aggregates, which in turn depend on the firms' decisions. We cast this fixed-point problem as a Mean Field Game and prove several analytic results. We establish existence and uniqueness of the equilibrium and characterize the impulse response function (IRF) of output following an aggregate shock. We prove that strategic complementarities make the IRF larger at each horizon. We establish that complementarities may give rise to an IRF with a hump-shaped profile. As the complementarity becomes large enough, the IRF diverges, and at a critical point there is no equilibrium. Finally, we show that the amplification effect of the strategic interactions is similar across models: the Calvo model and the Golosov–Lucas model display a comparable amplification, in spite of the fact that the non-neutrality in Calvo is much larger.

期刊介绍:

Econometrica publishes original articles in all branches of economics - theoretical and empirical, abstract and applied, providing wide-ranging coverage across the subject area. It promotes studies that aim at the unification of the theoretical-quantitative and the empirical-quantitative approach to economic problems and that are penetrated by constructive and rigorous thinking. It explores a unique range of topics each year - from the frontier of theoretical developments in many new and important areas, to research on current and applied economic problems, to methodologically innovative, theoretical and applied studies in econometrics.

Econometrica maintains a long tradition that submitted articles are refereed carefully and that detailed and thoughtful referee reports are provided to the author as an aid to scientific research, thus ensuring the high calibre of papers found in Econometrica. An international board of editors, together with the referees it has selected, has succeeded in substantially reducing editorial turnaround time, thereby encouraging submissions of the highest quality.

We strongly encourage recent Ph. D. graduates to submit their work to Econometrica. Our policy is to take into account the fact that recent graduates are less experienced in the process of writing and submitting papers.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: