Stefan Schaltegger, Katherine L. Christ, Julius Wenzig, Roger L. Burritt

{"title":"Corporate sustainability management accounting and multi-level links for sustainability – A systematic review","authors":"Stefan Schaltegger, Katherine L. Christ, Julius Wenzig, Roger L. Burritt","doi":"10.1111/ijmr.12288","DOIUrl":null,"url":null,"abstract":"<p>The societal vision of sustainable development changes both the context of businesses and expectations that management should contribute to solving sustainability problems beyond organizational boundaries. Companies are influenced by macro-level developments such as new environmental regulations and by meso-level context such as social industry standards and guidelines. At the same time, companies are expected to contribute to sustainability transformations of markets at the meso-level and to solving grand sustainability problems at the macro-level such as the greenhouse effect. These developments increase and change sustainability information needs of managers and management accounting. This paper provides a systematic literature review of how sustainability management accounting (SMA) addresses links with the organization's contexts and contributions to sustainability transformations beyond organizational boundaries. The analysis questions the conventional assumption of an internal scope for SMA. It recognises this as a problematic constricting assumption in the literature and, instead, proposes a multi-level Context, Action-formation and Transformative contributions (CAT) framework for further development of SMA.</p>","PeriodicalId":48326,"journal":{"name":"International Journal of Management Reviews","volume":"24 4","pages":"480-500"},"PeriodicalIF":7.5000,"publicationDate":"2022-01-17","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/ijmr.12288","citationCount":"22","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"International Journal of Management Reviews","FirstCategoryId":"91","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/ijmr.12288","RegionNum":1,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"BUSINESS","Score":null,"Total":0}

引用次数: 22

Abstract

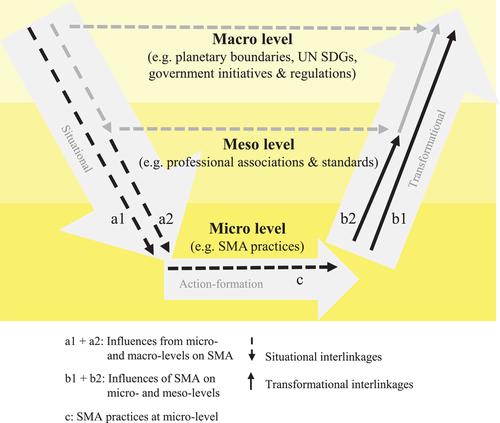

The societal vision of sustainable development changes both the context of businesses and expectations that management should contribute to solving sustainability problems beyond organizational boundaries. Companies are influenced by macro-level developments such as new environmental regulations and by meso-level context such as social industry standards and guidelines. At the same time, companies are expected to contribute to sustainability transformations of markets at the meso-level and to solving grand sustainability problems at the macro-level such as the greenhouse effect. These developments increase and change sustainability information needs of managers and management accounting. This paper provides a systematic literature review of how sustainability management accounting (SMA) addresses links with the organization's contexts and contributions to sustainability transformations beyond organizational boundaries. The analysis questions the conventional assumption of an internal scope for SMA. It recognises this as a problematic constricting assumption in the literature and, instead, proposes a multi-level Context, Action-formation and Transformative contributions (CAT) framework for further development of SMA.

期刊介绍:

The International Journal of Management Reviews (IJMR) stands as the premier global review journal in Organisation and Management Studies (OMS). Its published papers aim to provide substantial conceptual contributions, acting as a strategic platform for new research directions. IJMR plays a pivotal role in influencing how OMS scholars conceptualize research in their respective fields. The journal's reviews critically assess the state of knowledge in specific fields, appraising the conceptual foundations of competing paradigms to advance current and future research in the area.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: