{"title":"How the new fed municipal bond facility capped municipal-treasury yield spreads in the Covid-19 recession","authors":"Michael D. Bordo , John V. Duca","doi":"10.1016/j.jjie.2022.101245","DOIUrl":null,"url":null,"abstract":"<div><p>For over two centuries, the municipal (muni) bond market has been a source of systemic risk, which returned early in the Covid-19 downturn when borrowing from securities markets became costly for many private and public entities, and some found it difficult to borrow at all. Indeed, just before the Fed announced its unprecedented intervention into the muni market, spreads of muni over Treasury yields rose in line with the unemployment rate and appeared headed to levels not seen since the Great Depression, when real municipal gross investment plunged 35 percent below 1929 levels. To prevent such a calamity, the Fed created the Municipal Liquidity Facility (MLF) to purchase newly issued, (near) investment-grade state and local government bonds at ratings-based interest rate spreads over the safe OIS benchmark yield. In general, these spreads were initially about 100 basis points above average spreads under more normal market conditions and were later lowered by 50 basis points in August 2020. Despite a modest take-up, our study documents the MLF prevented muni spreads from rising much above those margins (plus a modest 10 basis point fee) and limited the extent to which interest rate spreads could have amplified the impact of the Covid pandemic. To establish the MLF the Fed needed Treasury indemnification against default losses. There were concerns about whether the creation of the MLF could induce moral hazard among borrowers and could undermine the efficiency of the bond market if the facility had lasted too long. Partly for this reason and because the muni market had settled down by yearend 2020, the Treasury terminated the MLF at that time. Future assessments of these downside aspects will help answer the question whether the program's benefits addressed here exceeded its costs.</p></div>","PeriodicalId":47082,"journal":{"name":"Journal of the Japanese and International Economies","volume":"67 ","pages":"Article 101245"},"PeriodicalIF":3.1000,"publicationDate":"2023-03-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC9789544/pdf/","citationCount":"14","resultStr":null,"platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of the Japanese and International Economies","FirstCategoryId":"96","ListUrlMain":"https://www.sciencedirect.com/science/article/pii/S0889158322000545","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"ECONOMICS","Score":null,"Total":0}

引用次数: 14

Abstract

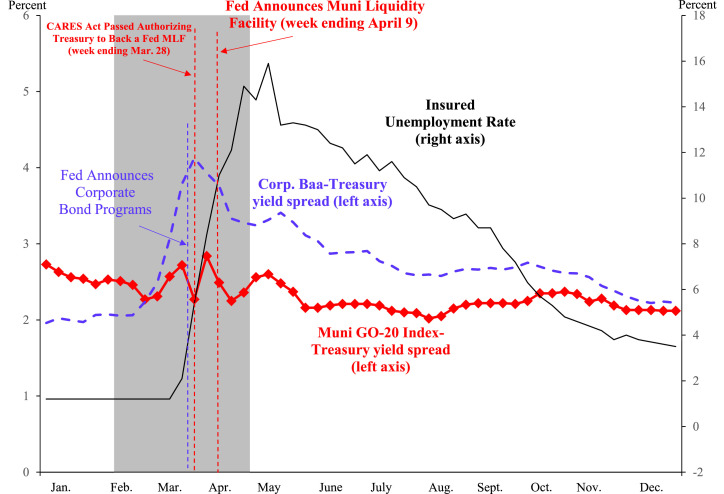

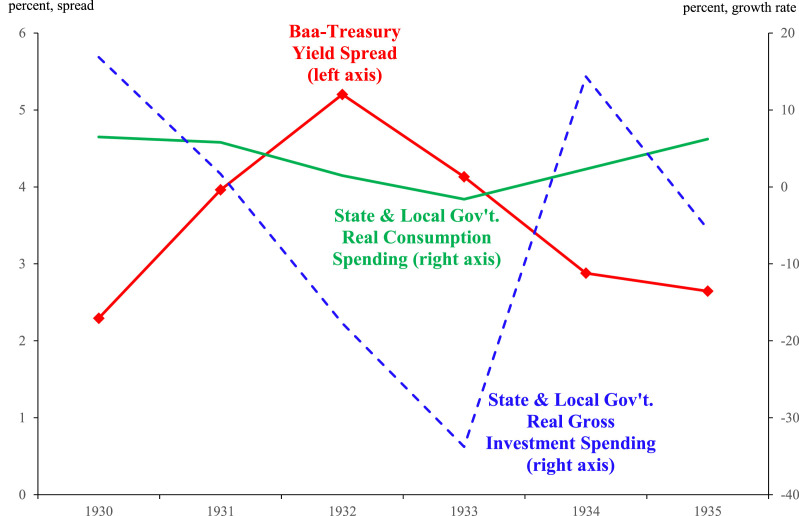

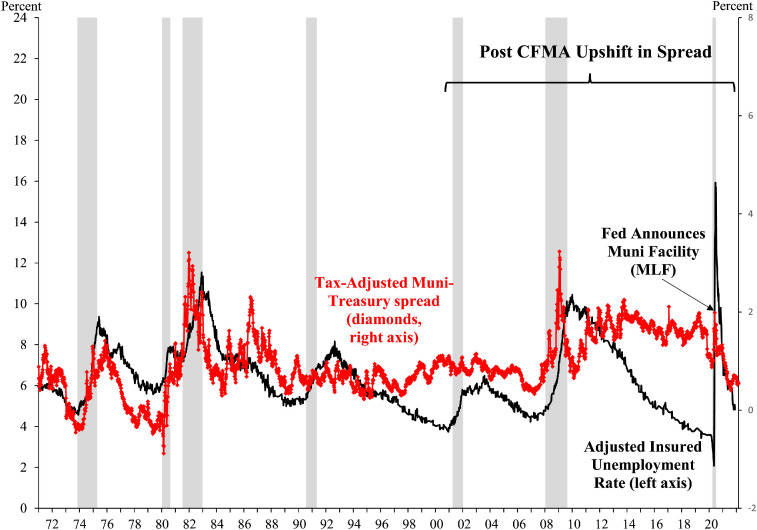

For over two centuries, the municipal (muni) bond market has been a source of systemic risk, which returned early in the Covid-19 downturn when borrowing from securities markets became costly for many private and public entities, and some found it difficult to borrow at all. Indeed, just before the Fed announced its unprecedented intervention into the muni market, spreads of muni over Treasury yields rose in line with the unemployment rate and appeared headed to levels not seen since the Great Depression, when real municipal gross investment plunged 35 percent below 1929 levels. To prevent such a calamity, the Fed created the Municipal Liquidity Facility (MLF) to purchase newly issued, (near) investment-grade state and local government bonds at ratings-based interest rate spreads over the safe OIS benchmark yield. In general, these spreads were initially about 100 basis points above average spreads under more normal market conditions and were later lowered by 50 basis points in August 2020. Despite a modest take-up, our study documents the MLF prevented muni spreads from rising much above those margins (plus a modest 10 basis point fee) and limited the extent to which interest rate spreads could have amplified the impact of the Covid pandemic. To establish the MLF the Fed needed Treasury indemnification against default losses. There were concerns about whether the creation of the MLF could induce moral hazard among borrowers and could undermine the efficiency of the bond market if the facility had lasted too long. Partly for this reason and because the muni market had settled down by yearend 2020, the Treasury terminated the MLF at that time. Future assessments of these downside aspects will help answer the question whether the program's benefits addressed here exceeded its costs.

期刊介绍:

The Journal of the Japanese and International Economies publishes original reports of research devoted to academic analyses of the Japanese economy and its interdependence on other national economies. The Journal also features articles that present related theoretical, empirical, and comparative analyses with their policy implications. Book reviews are also published.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: