{"title":"定向网络的传染风险和安全投资。","authors":"Hamed Amini","doi":"10.1007/s11579-023-00336-w","DOIUrl":null,"url":null,"abstract":"<p><p>We develop a model for contagion risks and optimal security investment in a directed network of interconnected agents with heterogeneous degrees, loss functions, and security profiles. Our model generalizes several contagion models in the literature, particularly the independent cascade model and the linear threshold model. We state various limit theorems on the final size of infected agents in the case of random networks with given vertex degrees for finite and infinite-variance degree distributions. The results allow us to derive a resilience condition for the network in response to the infection of a large group of agents and quantify how contagion amplifies small shocks to the network. We show that when the degree distribution has infinite variance and highly correlated in- and out-degrees, even when agents have high thresholds, a sub-linear fraction of initially infected agents is enough to trigger the infection of a positive fraction of nodes. We also demonstrate how these results are sensitive to vertex and edge percolation (intervention). We then study the asymptotic Nash equilibrium and socially optimal security investment. In the asymptotic limit, agents' risk depends on all other agents' investments through an aggregate quantity that we call network vulnerability. The limit theorems enable us to capture the impact of one class of agents' decisions on the overall network vulnerability. Based on our results, the vulnerability is semi-analytic, allowing for a tractable Nash equilibrium. We provide sufficient conditions for investment in equilibrium to be monotone in network vulnerability. When investment is monotone, we demonstrate that the (asymptotic) Nash equilibrium is unique. In the specific example of two types of core-periphery agents, we illustrate the strong effect of cost heterogeneity on network vulnerability and the non-monotonous investment as a function of costs.</p>","PeriodicalId":48722,"journal":{"name":"Mathematics and Financial Economics","volume":"17 2","pages":"247-283"},"PeriodicalIF":1.0000,"publicationDate":"2023-01-01","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10189239/pdf/","citationCount":"3","resultStr":"{\"title\":\"Contagion risks and security investment in directed networks.\",\"authors\":\"Hamed Amini\",\"doi\":\"10.1007/s11579-023-00336-w\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>We develop a model for contagion risks and optimal security investment in a directed network of interconnected agents with heterogeneous degrees, loss functions, and security profiles. Our model generalizes several contagion models in the literature, particularly the independent cascade model and the linear threshold model. We state various limit theorems on the final size of infected agents in the case of random networks with given vertex degrees for finite and infinite-variance degree distributions. The results allow us to derive a resilience condition for the network in response to the infection of a large group of agents and quantify how contagion amplifies small shocks to the network. We show that when the degree distribution has infinite variance and highly correlated in- and out-degrees, even when agents have high thresholds, a sub-linear fraction of initially infected agents is enough to trigger the infection of a positive fraction of nodes. We also demonstrate how these results are sensitive to vertex and edge percolation (intervention). We then study the asymptotic Nash equilibrium and socially optimal security investment. In the asymptotic limit, agents' risk depends on all other agents' investments through an aggregate quantity that we call network vulnerability. The limit theorems enable us to capture the impact of one class of agents' decisions on the overall network vulnerability. Based on our results, the vulnerability is semi-analytic, allowing for a tractable Nash equilibrium. We provide sufficient conditions for investment in equilibrium to be monotone in network vulnerability. When investment is monotone, we demonstrate that the (asymptotic) Nash equilibrium is unique. In the specific example of two types of core-periphery agents, we illustrate the strong effect of cost heterogeneity on network vulnerability and the non-monotonous investment as a function of costs.</p>\",\"PeriodicalId\":48722,\"journal\":{\"name\":\"Mathematics and Financial Economics\",\"volume\":\"17 2\",\"pages\":\"247-283\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-01-01\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10189239/pdf/\",\"citationCount\":\"3\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Mathematics and Financial Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://doi.org/10.1007/s11579-023-00336-w\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"2023/5/17 0:00:00\",\"PubModel\":\"Epub\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Mathematics and Financial Economics","FirstCategoryId":"96","ListUrlMain":"https://doi.org/10.1007/s11579-023-00336-w","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"2023/5/17 0:00:00","PubModel":"Epub","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Contagion risks and security investment in directed networks.

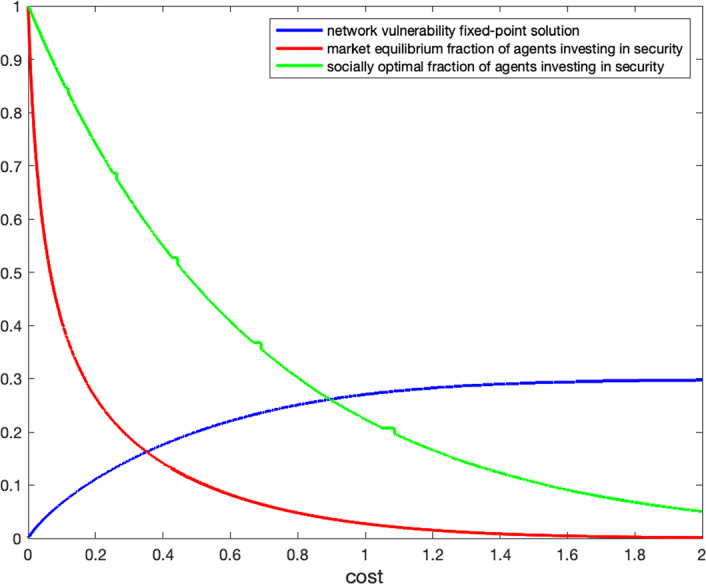

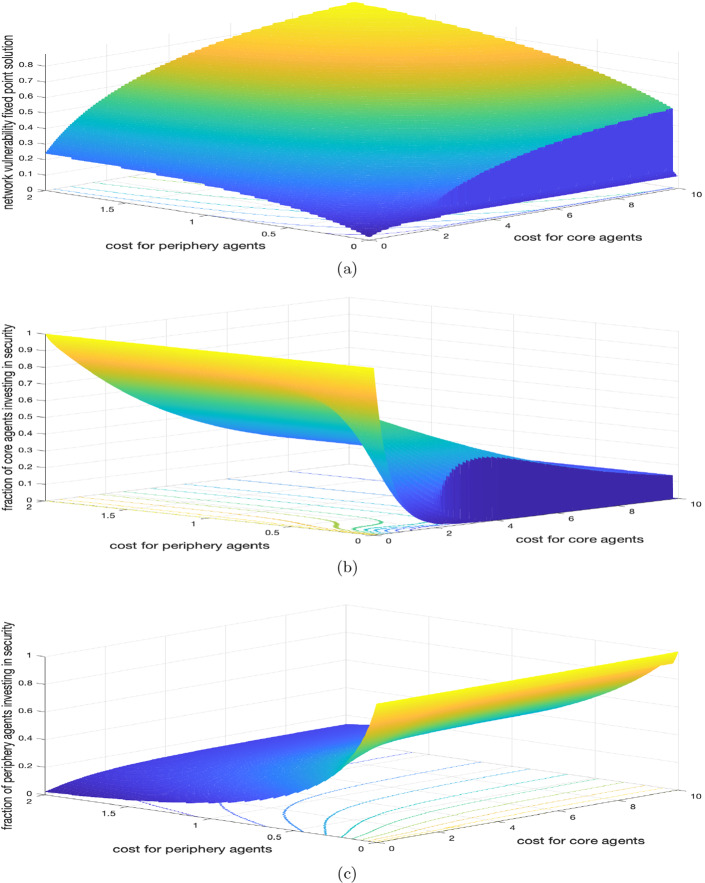

We develop a model for contagion risks and optimal security investment in a directed network of interconnected agents with heterogeneous degrees, loss functions, and security profiles. Our model generalizes several contagion models in the literature, particularly the independent cascade model and the linear threshold model. We state various limit theorems on the final size of infected agents in the case of random networks with given vertex degrees for finite and infinite-variance degree distributions. The results allow us to derive a resilience condition for the network in response to the infection of a large group of agents and quantify how contagion amplifies small shocks to the network. We show that when the degree distribution has infinite variance and highly correlated in- and out-degrees, even when agents have high thresholds, a sub-linear fraction of initially infected agents is enough to trigger the infection of a positive fraction of nodes. We also demonstrate how these results are sensitive to vertex and edge percolation (intervention). We then study the asymptotic Nash equilibrium and socially optimal security investment. In the asymptotic limit, agents' risk depends on all other agents' investments through an aggregate quantity that we call network vulnerability. The limit theorems enable us to capture the impact of one class of agents' decisions on the overall network vulnerability. Based on our results, the vulnerability is semi-analytic, allowing for a tractable Nash equilibrium. We provide sufficient conditions for investment in equilibrium to be monotone in network vulnerability. When investment is monotone, we demonstrate that the (asymptotic) Nash equilibrium is unique. In the specific example of two types of core-periphery agents, we illustrate the strong effect of cost heterogeneity on network vulnerability and the non-monotonous investment as a function of costs.

期刊介绍:

The primary objective of the journal is to provide a forum for work in finance which expresses economic ideas using formal mathematical reasoning. The work should have real economic content and the mathematical reasoning should be new and correct.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: