{"title":"Reddit上的财务建议、股票回报率和累积前景理论。","authors":"Felix Reichenbach, Martin Walther","doi":"10.1007/s42521-023-00084-y","DOIUrl":null,"url":null,"abstract":"<p><p>This study investigates stock recommendations from the three largest finance subreddits on Reddit: wallstreetbets, investing and stocks. A simple strategy that buys recommended stocks weighted by the number of posts per day yields a portfolio with higher average returns at the expense of higher risks than the market for all holding periods, i.e., unfavorable Sharpe ratios. Furthermore, the strategy leads to positive (insignificant) short-term and negative (significant) long-term alphas when considering common risk factors. This is consistent with the idea of \"meme stocks\", meaning that the recommended stocks are artificially inflated in the short term when they are recommended, and that the posts contain no information about long-term success. However, it is likely that Reddit users, especially on the subreddit wallstreetbets, have preferences for bets which are not captured by the mean-variance framework. Therefore, we draw on cumulative prospect theory (CPT). We find that the CPT-valuations of the Reddit portfolio exceed those of the market, which may explain the persistent attractiveness for investors to follow social media stock recommendations despite the unfavorable risk-return ratio.</p>","PeriodicalId":72817,"journal":{"name":"Digital finance","volume":" ","pages":"1-28"},"PeriodicalIF":0.0000,"publicationDate":"2023-04-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10111308/pdf/","citationCount":"1","resultStr":"{\"title\":\"Financial recommendations on Reddit, stock returns and cumulative prospect theory.\",\"authors\":\"Felix Reichenbach, Martin Walther\",\"doi\":\"10.1007/s42521-023-00084-y\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>This study investigates stock recommendations from the three largest finance subreddits on Reddit: wallstreetbets, investing and stocks. A simple strategy that buys recommended stocks weighted by the number of posts per day yields a portfolio with higher average returns at the expense of higher risks than the market for all holding periods, i.e., unfavorable Sharpe ratios. Furthermore, the strategy leads to positive (insignificant) short-term and negative (significant) long-term alphas when considering common risk factors. This is consistent with the idea of \\\"meme stocks\\\", meaning that the recommended stocks are artificially inflated in the short term when they are recommended, and that the posts contain no information about long-term success. However, it is likely that Reddit users, especially on the subreddit wallstreetbets, have preferences for bets which are not captured by the mean-variance framework. Therefore, we draw on cumulative prospect theory (CPT). We find that the CPT-valuations of the Reddit portfolio exceed those of the market, which may explain the persistent attractiveness for investors to follow social media stock recommendations despite the unfavorable risk-return ratio.</p>\",\"PeriodicalId\":72817,\"journal\":{\"name\":\"Digital finance\",\"volume\":\" \",\"pages\":\"1-28\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-04-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10111308/pdf/\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Digital finance\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s42521-023-00084-y\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Digital finance","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s42521-023-00084-y","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Financial recommendations on Reddit, stock returns and cumulative prospect theory.

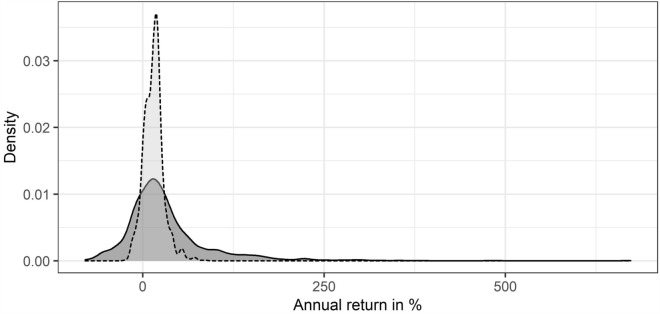

This study investigates stock recommendations from the three largest finance subreddits on Reddit: wallstreetbets, investing and stocks. A simple strategy that buys recommended stocks weighted by the number of posts per day yields a portfolio with higher average returns at the expense of higher risks than the market for all holding periods, i.e., unfavorable Sharpe ratios. Furthermore, the strategy leads to positive (insignificant) short-term and negative (significant) long-term alphas when considering common risk factors. This is consistent with the idea of "meme stocks", meaning that the recommended stocks are artificially inflated in the short term when they are recommended, and that the posts contain no information about long-term success. However, it is likely that Reddit users, especially on the subreddit wallstreetbets, have preferences for bets which are not captured by the mean-variance framework. Therefore, we draw on cumulative prospect theory (CPT). We find that the CPT-valuations of the Reddit portfolio exceed those of the market, which may explain the persistent attractiveness for investors to follow social media stock recommendations despite the unfavorable risk-return ratio.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: