{"title":"通过双重触发猫债券提供疫情业务中断保险。","authors":"André Schmitt, Sandrine Spaeter","doi":"10.1057/s41288-023-00299-5","DOIUrl":null,"url":null,"abstract":"<p><p>The aim of this paper is to show how qualified investors in cat bonds can offer adequate pandemic business interruption protection in a comprehensive public-private coverage scheme. First, we propose a numerical model to expose how cat bonds can contribute to complement standard re/insurance by improving coverage of cedents even though risks are positively correlated during a pandemic. Second, we introduce double trigger pandemic business interruption cat bonds, which we name PBI bonds, and discuss their precise characteristics to provide efficient coverage. A first trigger should be pulled when the World Health Organization declares a Public Health Emergency of International Concern (PHEIC). The second trigger determines the payout of the bond based on the modelised business interruption losses of an industry in a country. We discuss moral hazard, basis risk, correlation and liquidity issues which are critical in the context of a pandemic. Third, we simulate the life of theoretical PBI bonds in the restaurant industry in France by using data gathered during the COVID-19 pandemic.</p>","PeriodicalId":75009,"journal":{"name":"The Geneva papers on risk and insurance. Issues and practice","volume":" ","pages":"1-27"},"PeriodicalIF":3.3000,"publicationDate":"2023-05-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10228458/pdf/","citationCount":"1","resultStr":"{\"title\":\"Providing pandemic business interruption coverage with double trigger cat bonds.\",\"authors\":\"André Schmitt, Sandrine Spaeter\",\"doi\":\"10.1057/s41288-023-00299-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>The aim of this paper is to show how qualified investors in cat bonds can offer adequate pandemic business interruption protection in a comprehensive public-private coverage scheme. First, we propose a numerical model to expose how cat bonds can contribute to complement standard re/insurance by improving coverage of cedents even though risks are positively correlated during a pandemic. Second, we introduce double trigger pandemic business interruption cat bonds, which we name PBI bonds, and discuss their precise characteristics to provide efficient coverage. A first trigger should be pulled when the World Health Organization declares a Public Health Emergency of International Concern (PHEIC). The second trigger determines the payout of the bond based on the modelised business interruption losses of an industry in a country. We discuss moral hazard, basis risk, correlation and liquidity issues which are critical in the context of a pandemic. Third, we simulate the life of theoretical PBI bonds in the restaurant industry in France by using data gathered during the COVID-19 pandemic.</p>\",\"PeriodicalId\":75009,\"journal\":{\"name\":\"The Geneva papers on risk and insurance. Issues and practice\",\"volume\":\" \",\"pages\":\"1-27\"},\"PeriodicalIF\":3.3000,\"publicationDate\":\"2023-05-30\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10228458/pdf/\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"The Geneva papers on risk and insurance. Issues and practice\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1057/s41288-023-00299-5\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"The Geneva papers on risk and insurance. Issues and practice","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1057/s41288-023-00299-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

Providing pandemic business interruption coverage with double trigger cat bonds.

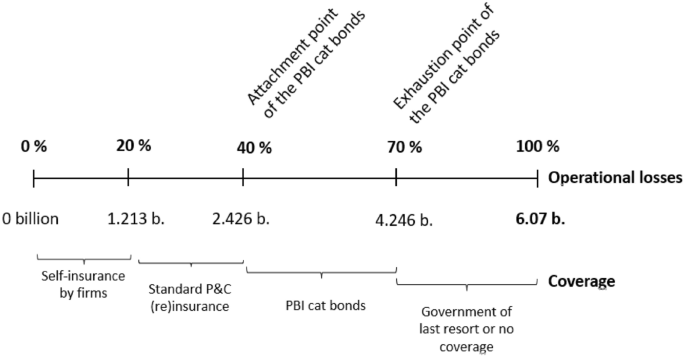

The aim of this paper is to show how qualified investors in cat bonds can offer adequate pandemic business interruption protection in a comprehensive public-private coverage scheme. First, we propose a numerical model to expose how cat bonds can contribute to complement standard re/insurance by improving coverage of cedents even though risks are positively correlated during a pandemic. Second, we introduce double trigger pandemic business interruption cat bonds, which we name PBI bonds, and discuss their precise characteristics to provide efficient coverage. A first trigger should be pulled when the World Health Organization declares a Public Health Emergency of International Concern (PHEIC). The second trigger determines the payout of the bond based on the modelised business interruption losses of an industry in a country. We discuss moral hazard, basis risk, correlation and liquidity issues which are critical in the context of a pandemic. Third, we simulate the life of theoretical PBI bonds in the restaurant industry in France by using data gathered during the COVID-19 pandemic.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: