{"title":"欧洲网络监管背景下的贝塔估计:什么重要,什么不重要,什么是不可或缺的。","authors":"Dmitry Bazhutov, André Betzer, Richard Stehle","doi":"10.1007/s11408-023-00428-z","DOIUrl":null,"url":null,"abstract":"<p><p>Most studies on beta estimation look at the whole universe of stocks. We focus on a small subset that consists of stocks of companies which are subject to European network regulation. This allows us to examine beta time series of individual stocks and small peer groups in great detail. Our most important conclusions are: (1) Sudden beta increases or decreases occur that often last only short periods of time and may therefore cause a significant misestimation of the future beta. (2) Three- and especially five-year betas are much more stable than one-year betas. (3) The choice between purely local, European or global betas may matter considerably. (4) Weekly or daily betas seem to be better than monthly ones. (5) Vasicek and Blume adjustments towards one lead to beta predictions that are too high.</p>","PeriodicalId":44895,"journal":{"name":"Financial Markets and Portfolio Management","volume":" ","pages":"1-37"},"PeriodicalIF":1.8000,"publicationDate":"2023-04-26","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10131524/pdf/","citationCount":"1","resultStr":"{\"title\":\"Beta estimation in the European network regulation context: what matters, what doesn't, and what is indispensable.\",\"authors\":\"Dmitry Bazhutov, André Betzer, Richard Stehle\",\"doi\":\"10.1007/s11408-023-00428-z\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>Most studies on beta estimation look at the whole universe of stocks. We focus on a small subset that consists of stocks of companies which are subject to European network regulation. This allows us to examine beta time series of individual stocks and small peer groups in great detail. Our most important conclusions are: (1) Sudden beta increases or decreases occur that often last only short periods of time and may therefore cause a significant misestimation of the future beta. (2) Three- and especially five-year betas are much more stable than one-year betas. (3) The choice between purely local, European or global betas may matter considerably. (4) Weekly or daily betas seem to be better than monthly ones. (5) Vasicek and Blume adjustments towards one lead to beta predictions that are too high.</p>\",\"PeriodicalId\":44895,\"journal\":{\"name\":\"Financial Markets and Portfolio Management\",\"volume\":\" \",\"pages\":\"1-37\"},\"PeriodicalIF\":1.8000,\"publicationDate\":\"2023-04-26\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10131524/pdf/\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Markets and Portfolio Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s11408-023-00428-z\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Markets and Portfolio Management","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s11408-023-00428-z","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Beta estimation in the European network regulation context: what matters, what doesn't, and what is indispensable.

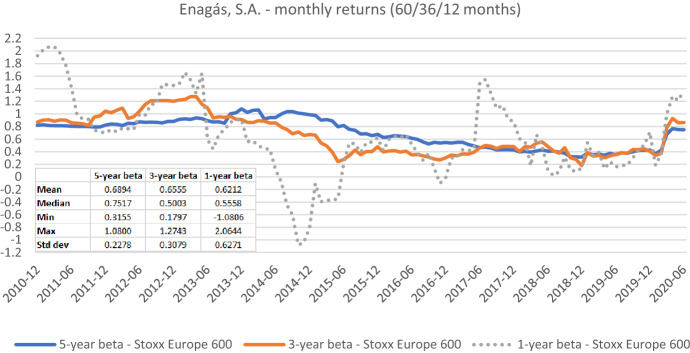

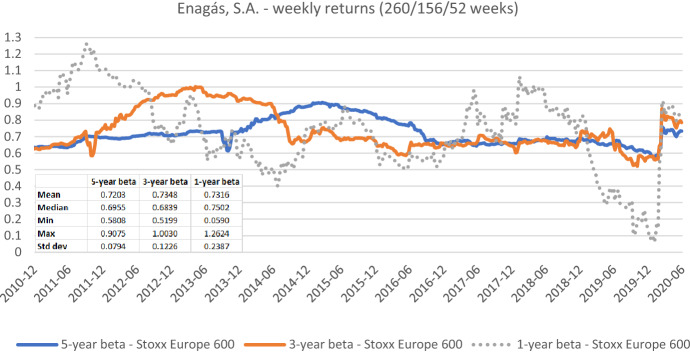

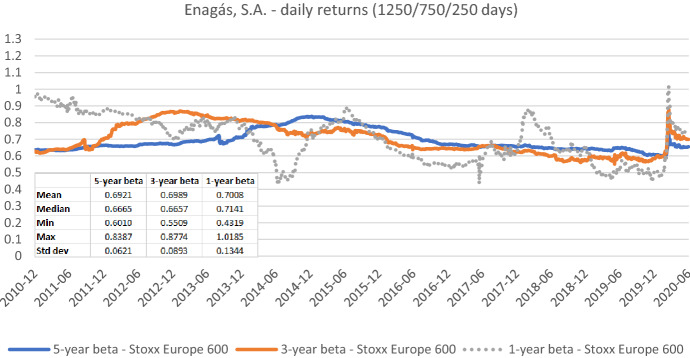

Most studies on beta estimation look at the whole universe of stocks. We focus on a small subset that consists of stocks of companies which are subject to European network regulation. This allows us to examine beta time series of individual stocks and small peer groups in great detail. Our most important conclusions are: (1) Sudden beta increases or decreases occur that often last only short periods of time and may therefore cause a significant misestimation of the future beta. (2) Three- and especially five-year betas are much more stable than one-year betas. (3) The choice between purely local, European or global betas may matter considerably. (4) Weekly or daily betas seem to be better than monthly ones. (5) Vasicek and Blume adjustments towards one lead to beta predictions that are too high.

期刊介绍:

The journal Financial Markets and Portfolio Management invites submissions of original research articles in all areas of finance, especially in – but not limited to – financial markets, portfolio choice and wealth management, asset pricing, risk management, and regulation. Its principal objective is to publish high-quality articles of innovative research and practical application. The readers of Financial Markets and Portfolio Management are academics and professionals in finance and economics, especially in the areas of asset management. FMPM publishes academic and applied research articles, shorter ''Perspectives'' and survey articles on current topics of interest to the financial community, as well as book reviews. All article submissions are subject to a double-blind peer review. http://www.fmpm.org

Officially cited as: Financ Mark Portf Manag

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: