Elena Villar-Rubio, María-Dolores Huete-Morales, Federico Galán-Valdivieso

{"title":"使用EGARCH模型预测未合并金融市场的波动性:以欧洲碳配额为例。","authors":"Elena Villar-Rubio, María-Dolores Huete-Morales, Federico Galán-Valdivieso","doi":"10.1007/s13412-023-00838-5","DOIUrl":null,"url":null,"abstract":"<p><p>The growing interest and direct impact of carbon trading in the economy have drawn an increasing attention to the evolution of the price of CO2 allowances (European Union Allowances, EUAs) under the European Union Emissions Trading Scheme (EU ETS). As a novel financial market, the dynamic analysis of its volatility is essential for policymakers to assess market efficiency and for investors to carry out an adequate risk management on carbon emission rights. In this research, the main autoregressive conditional heteroskedasticity (ARCH) models were applied to evaluate and analyze the volatility of daily data of the European carbon future prices, focusing on the last finished phase of market operations (phase III, 2013-2020), which is structurally and significantly different from previous phases. Some empirical findings derive from the results obtained. First, the EGARCH (1,1) model exhibits a superior ability to describe the price volatility even using fewer parameters, partly because it allows to collect the sign of the changes produced over time. In this model, the Akaike information criterion (AIC) is lower than ARCH (4) and GARCH (1,1) models, and all its coefficients are significative (<i>p</i> < 0.02). Second, a sustained increase in prices is detected at the end of phase III, which makes it possible to foresee a stabilization path with higher prices for the first years of phase IV. These changes will motivate both companies and individual energy investors to be proactive in making decisions about the risk management on carbon allowances.</p>","PeriodicalId":44550,"journal":{"name":"Journal of Environmental Studies and Sciences","volume":" ","pages":"1-10"},"PeriodicalIF":2.3000,"publicationDate":"2023-05-11","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10172064/pdf/","citationCount":"0","resultStr":"{\"title\":\"Using EGARCH models to predict volatility in unconsolidated financial markets: the case of European carbon allowances.\",\"authors\":\"Elena Villar-Rubio, María-Dolores Huete-Morales, Federico Galán-Valdivieso\",\"doi\":\"10.1007/s13412-023-00838-5\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p><p>The growing interest and direct impact of carbon trading in the economy have drawn an increasing attention to the evolution of the price of CO2 allowances (European Union Allowances, EUAs) under the European Union Emissions Trading Scheme (EU ETS). As a novel financial market, the dynamic analysis of its volatility is essential for policymakers to assess market efficiency and for investors to carry out an adequate risk management on carbon emission rights. In this research, the main autoregressive conditional heteroskedasticity (ARCH) models were applied to evaluate and analyze the volatility of daily data of the European carbon future prices, focusing on the last finished phase of market operations (phase III, 2013-2020), which is structurally and significantly different from previous phases. Some empirical findings derive from the results obtained. First, the EGARCH (1,1) model exhibits a superior ability to describe the price volatility even using fewer parameters, partly because it allows to collect the sign of the changes produced over time. In this model, the Akaike information criterion (AIC) is lower than ARCH (4) and GARCH (1,1) models, and all its coefficients are significative (<i>p</i> < 0.02). Second, a sustained increase in prices is detected at the end of phase III, which makes it possible to foresee a stabilization path with higher prices for the first years of phase IV. These changes will motivate both companies and individual energy investors to be proactive in making decisions about the risk management on carbon allowances.</p>\",\"PeriodicalId\":44550,\"journal\":{\"name\":\"Journal of Environmental Studies and Sciences\",\"volume\":\" \",\"pages\":\"1-10\"},\"PeriodicalIF\":2.3000,\"publicationDate\":\"2023-05-11\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://www.ncbi.nlm.nih.gov/pmc/articles/PMC10172064/pdf/\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Journal of Environmental Studies and Sciences\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://doi.org/10.1007/s13412-023-00838-5\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"ENVIRONMENTAL SCIENCES\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Journal of Environmental Studies and Sciences","FirstCategoryId":"1085","ListUrlMain":"https://doi.org/10.1007/s13412-023-00838-5","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"ENVIRONMENTAL SCIENCES","Score":null,"Total":0}

Using EGARCH models to predict volatility in unconsolidated financial markets: the case of European carbon allowances.

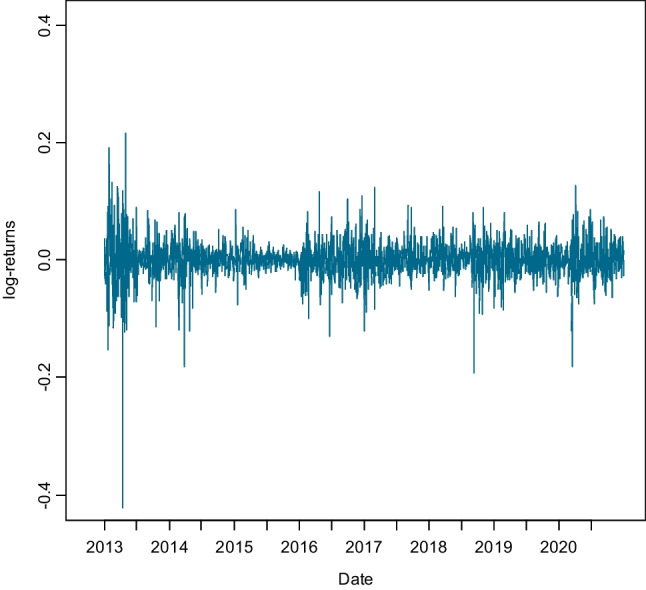

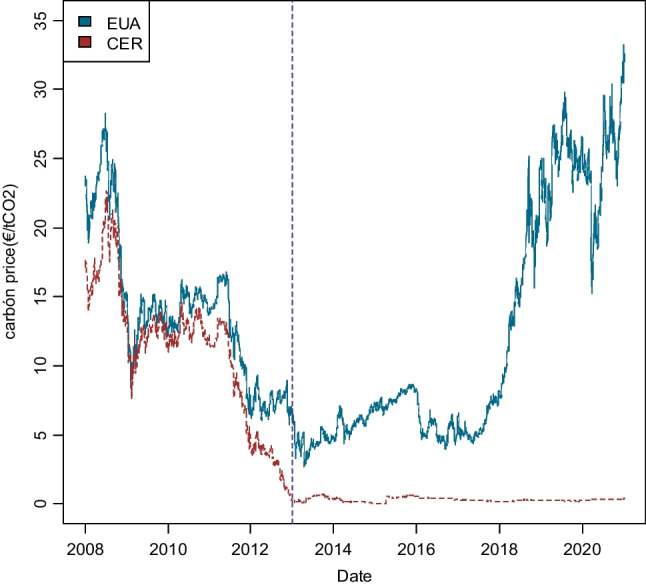

The growing interest and direct impact of carbon trading in the economy have drawn an increasing attention to the evolution of the price of CO2 allowances (European Union Allowances, EUAs) under the European Union Emissions Trading Scheme (EU ETS). As a novel financial market, the dynamic analysis of its volatility is essential for policymakers to assess market efficiency and for investors to carry out an adequate risk management on carbon emission rights. In this research, the main autoregressive conditional heteroskedasticity (ARCH) models were applied to evaluate and analyze the volatility of daily data of the European carbon future prices, focusing on the last finished phase of market operations (phase III, 2013-2020), which is structurally and significantly different from previous phases. Some empirical findings derive from the results obtained. First, the EGARCH (1,1) model exhibits a superior ability to describe the price volatility even using fewer parameters, partly because it allows to collect the sign of the changes produced over time. In this model, the Akaike information criterion (AIC) is lower than ARCH (4) and GARCH (1,1) models, and all its coefficients are significative (p < 0.02). Second, a sustained increase in prices is detected at the end of phase III, which makes it possible to foresee a stabilization path with higher prices for the first years of phase IV. These changes will motivate both companies and individual energy investors to be proactive in making decisions about the risk management on carbon allowances.

期刊介绍:

The Journal of Environmental Studies and Sciences is the official publication for the Association for Environmental?Studies and Sciences?(AESS). Interdisciplinary environmental studies require an integration of many different scientific and professional disciplines. The AESS and the Journal provide fora for the advancement of interdisciplinary approaches to the study of the coupled human-nature systems. A major goal of AESS is to encourage this advancement by promoting related teaching research and service and by facilitating communication across boundaries that may inhibit environmental discourse across traditional academic disciplines—for example between and among the physical biological social sciences the humanities and environmental professions. This commitment also involves supporting the professional development of Association members and advancing the educational status of Environmental Studies and Sciences programs. The Journal provides a peer-reviewed academically rigorous and professionally recognized venue for the publication of explicitly interdisciplinary environmental research policy analysis and advocacy educational discourse and other related matters. Contributions are welcome from any discipline or combination of disciplines any vocation or professional affiliation any national ethnic or cultural background. Articles may relate to any historical and global setting. These contributions should explicitly involve multi-disciplinary or trans-disciplinary aspects of environmental issues; and identify the way(s) in which the work will contribute to environmental research policy making advocacy education or related activities.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: