Aditi Kar Gangopadhyay, Tanay Sheth, Sneha Chauhan

{"title":"金融领域的LAD:会计分析和欺诈检测","authors":"Aditi Kar Gangopadhyay, Tanay Sheth, Sneha Chauhan","doi":"10.1007/s43674-023-00052-4","DOIUrl":null,"url":null,"abstract":"<div><p>The paper explores advancements in accounting analytics using the logical analysis of data (LAD) approach by identifying fraudulent firms and transactions. The straightforward approach to fraud detection with an analytic model is to identify possible predictors of fraud associated with known fraudsters and their historical actions. LAD is a machine learning methodology that combines Boolean functions, optimization, and logic ideas in alignment with the traditional approach. The key characteristic of the LAD is discovering minimal sets of features necessary for explaining all observations and detecting hidden patterns in the data capable of distinguishing observations describing “positive” outcome events from “negative” outcome events. The combinatorial optimization model described in the paper represents a variation on the general theme of set covering and concludes with an outline of LAD applications to detect fraudulent firms and financial frauds. The dataset consists of Annual data of 777 firms from 14 different sectors. The results demonstrate 97.4% accuracy with an F1 score of 0.97. Another dataset on credit card transactions and finance is also used to test the effectiveness of LAD in finance. With the appearance of the immense growth of financial fraud cases, these promising results lead to future advancements in analytical audit fieldwork.</p></div>","PeriodicalId":72089,"journal":{"name":"Advances in computational intelligence","volume":"3 1","pages":""},"PeriodicalIF":0.0000,"publicationDate":"2023-01-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"LAD in finance: accounting analytics and fraud detection\",\"authors\":\"Aditi Kar Gangopadhyay, Tanay Sheth, Sneha Chauhan\",\"doi\":\"10.1007/s43674-023-00052-4\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>The paper explores advancements in accounting analytics using the logical analysis of data (LAD) approach by identifying fraudulent firms and transactions. The straightforward approach to fraud detection with an analytic model is to identify possible predictors of fraud associated with known fraudsters and their historical actions. LAD is a machine learning methodology that combines Boolean functions, optimization, and logic ideas in alignment with the traditional approach. The key characteristic of the LAD is discovering minimal sets of features necessary for explaining all observations and detecting hidden patterns in the data capable of distinguishing observations describing “positive” outcome events from “negative” outcome events. The combinatorial optimization model described in the paper represents a variation on the general theme of set covering and concludes with an outline of LAD applications to detect fraudulent firms and financial frauds. The dataset consists of Annual data of 777 firms from 14 different sectors. The results demonstrate 97.4% accuracy with an F1 score of 0.97. Another dataset on credit card transactions and finance is also used to test the effectiveness of LAD in finance. With the appearance of the immense growth of financial fraud cases, these promising results lead to future advancements in analytical audit fieldwork.</p></div>\",\"PeriodicalId\":72089,\"journal\":{\"name\":\"Advances in computational intelligence\",\"volume\":\"3 1\",\"pages\":\"\"},\"PeriodicalIF\":0.0000,\"publicationDate\":\"2023-01-30\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Advances in computational intelligence\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s43674-023-00052-4\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"\",\"JCRName\":\"\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Advances in computational intelligence","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s43674-023-00052-4","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"","JCRName":"","Score":null,"Total":0}

LAD in finance: accounting analytics and fraud detection

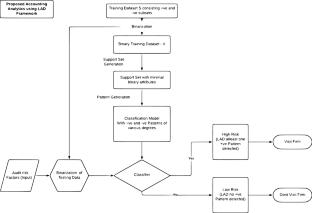

The paper explores advancements in accounting analytics using the logical analysis of data (LAD) approach by identifying fraudulent firms and transactions. The straightforward approach to fraud detection with an analytic model is to identify possible predictors of fraud associated with known fraudsters and their historical actions. LAD is a machine learning methodology that combines Boolean functions, optimization, and logic ideas in alignment with the traditional approach. The key characteristic of the LAD is discovering minimal sets of features necessary for explaining all observations and detecting hidden patterns in the data capable of distinguishing observations describing “positive” outcome events from “negative” outcome events. The combinatorial optimization model described in the paper represents a variation on the general theme of set covering and concludes with an outline of LAD applications to detect fraudulent firms and financial frauds. The dataset consists of Annual data of 777 firms from 14 different sectors. The results demonstrate 97.4% accuracy with an F1 score of 0.97. Another dataset on credit card transactions and finance is also used to test the effectiveness of LAD in finance. With the appearance of the immense growth of financial fraud cases, these promising results lead to future advancements in analytical audit fieldwork.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: