{"title":"在其他市场参与者的不确定性下进行交易","authors":"Dimitris Papadimitriou","doi":"10.1111/fire.12333","DOIUrl":null,"url":null,"abstract":"<p>I present an asymmetric information model of financial markets in which there is uncertainty and learning not only about fundamentals but also about the proportion of informed-to-noise traders in the market. Extreme news leads to an increase in both types of uncertainty, while it decreases price informativeness. Uncertainty about the market composition constitutes a type of liquidity risk and is associated with high expected returns. The resulting price–volume relationship is U-shaped and positively sloped. In a dynamic extension of the model I show that this mechanism generates momentum as well as history-dependent volatility and price informativeness.</p>","PeriodicalId":47617,"journal":{"name":"FINANCIAL REVIEW","volume":"58 2","pages":"343-367"},"PeriodicalIF":2.6000,"publicationDate":"2023-01-18","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fire.12333","citationCount":"0","resultStr":"{\"title\":\"Trading under uncertainty about other market participants\",\"authors\":\"Dimitris Papadimitriou\",\"doi\":\"10.1111/fire.12333\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>I present an asymmetric information model of financial markets in which there is uncertainty and learning not only about fundamentals but also about the proportion of informed-to-noise traders in the market. Extreme news leads to an increase in both types of uncertainty, while it decreases price informativeness. Uncertainty about the market composition constitutes a type of liquidity risk and is associated with high expected returns. The resulting price–volume relationship is U-shaped and positively sloped. In a dynamic extension of the model I show that this mechanism generates momentum as well as history-dependent volatility and price informativeness.</p>\",\"PeriodicalId\":47617,\"journal\":{\"name\":\"FINANCIAL REVIEW\",\"volume\":\"58 2\",\"pages\":\"343-367\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-01-18\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fire.12333\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"FINANCIAL REVIEW\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/fire.12333\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"FINANCIAL REVIEW","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/fire.12333","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Trading under uncertainty about other market participants

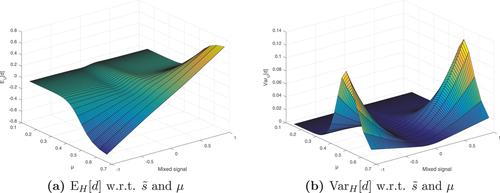

I present an asymmetric information model of financial markets in which there is uncertainty and learning not only about fundamentals but also about the proportion of informed-to-noise traders in the market. Extreme news leads to an increase in both types of uncertainty, while it decreases price informativeness. Uncertainty about the market composition constitutes a type of liquidity risk and is associated with high expected returns. The resulting price–volume relationship is U-shaped and positively sloped. In a dynamic extension of the model I show that this mechanism generates momentum as well as history-dependent volatility and price informativeness.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: