Nils Arne Lindaas, Kjartan Sarheim Anthun, Jon Magnussen

{"title":"公立医院信托的预算编制:盈余、乐观和准确","authors":"Nils Arne Lindaas, Kjartan Sarheim Anthun, Jon Magnussen","doi":"10.1111/faam.12358","DOIUrl":null,"url":null,"abstract":"<p>Hospitals in Norway are organized as trusts, required to follow the same accounting principles as the private sector, and responsible for funding their own investments. Thus, being able to run with a surplus has been an important part of their management. We analyze hospital budgeting for the whole sector over a 9-year period, looking at the size of the budget surplus, degree of optimism bias, and degree of budget accuracy when comparing to the actual financial results. Our findings indicate that on average, health trusts budget with a relatively small surplus. We find indications for optimism bias, but also examples of pessimism bias. Large health trusts seem to have a higher degree of accuracy of the budgeted results. Trusts that fail to meet budgeted results have a lower budgeted surplus the following period. Capital intensity, an indication of need for new investments, is not associated with budget surplus, degree of optimism, or budget accuracy.</p>","PeriodicalId":47120,"journal":{"name":"Financial Accountability & Management","volume":"39 3","pages":"514-533"},"PeriodicalIF":2.6000,"publicationDate":"2023-02-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/faam.12358","citationCount":"0","resultStr":"{\"title\":\"Budgeting in public hospital trusts: Surplus, optimism, and accuracy\",\"authors\":\"Nils Arne Lindaas, Kjartan Sarheim Anthun, Jon Magnussen\",\"doi\":\"10.1111/faam.12358\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>Hospitals in Norway are organized as trusts, required to follow the same accounting principles as the private sector, and responsible for funding their own investments. Thus, being able to run with a surplus has been an important part of their management. We analyze hospital budgeting for the whole sector over a 9-year period, looking at the size of the budget surplus, degree of optimism bias, and degree of budget accuracy when comparing to the actual financial results. Our findings indicate that on average, health trusts budget with a relatively small surplus. We find indications for optimism bias, but also examples of pessimism bias. Large health trusts seem to have a higher degree of accuracy of the budgeted results. Trusts that fail to meet budgeted results have a lower budgeted surplus the following period. Capital intensity, an indication of need for new investments, is not associated with budget surplus, degree of optimism, or budget accuracy.</p>\",\"PeriodicalId\":47120,\"journal\":{\"name\":\"Financial Accountability & Management\",\"volume\":\"39 3\",\"pages\":\"514-533\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-02-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/faam.12358\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Accountability & Management\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/faam.12358\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Accountability & Management","FirstCategoryId":"1085","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/faam.12358","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Budgeting in public hospital trusts: Surplus, optimism, and accuracy

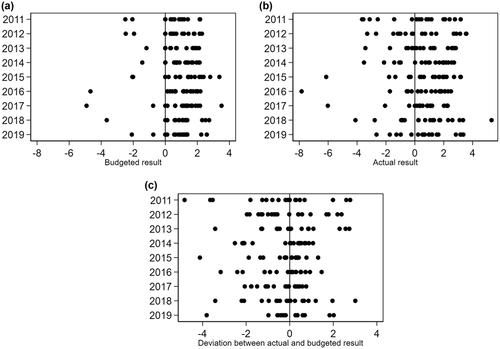

Hospitals in Norway are organized as trusts, required to follow the same accounting principles as the private sector, and responsible for funding their own investments. Thus, being able to run with a surplus has been an important part of their management. We analyze hospital budgeting for the whole sector over a 9-year period, looking at the size of the budget surplus, degree of optimism bias, and degree of budget accuracy when comparing to the actual financial results. Our findings indicate that on average, health trusts budget with a relatively small surplus. We find indications for optimism bias, but also examples of pessimism bias. Large health trusts seem to have a higher degree of accuracy of the budgeted results. Trusts that fail to meet budgeted results have a lower budgeted surplus the following period. Capital intensity, an indication of need for new investments, is not associated with budget surplus, degree of optimism, or budget accuracy.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: