Jinhan Xie, Xianwen Ding, Bei Jiang, Xiaodong Yan, Linglong Kong

{"title":"分位数回归的高维模型平均","authors":"Jinhan Xie, Xianwen Ding, Bei Jiang, Xiaodong Yan, Linglong Kong","doi":"10.1002/cjs.11789","DOIUrl":null,"url":null,"abstract":"<p>This article considers robust prediction issues in ultrahigh-dimensional (UHD) datasets and proposes combining quantile regression with sequential model averaging to arrive at a quantile sequential model averaging (QSMA) procedure. The QSMA method is made computationally feasible by employing a sequential screening process and a Bayesian information criterion (BIC) model averaging method for UHD quantile regression and provides a more accurate and stable prediction of the conditional quantile of a response variable. Meanwhile, the proposed method shows effective behaviour in dealing with prediction in UHD datasets and saves a great deal of computational cost with the help of the sequential technique. Under some suitable conditions, we show that the proposed QSMA method can mitigate overfitting and yields reliable predictions. Numerical studies, including extensive simulations and a real data example, are presented to confirm that the proposed method performs well.</p>","PeriodicalId":55281,"journal":{"name":"Canadian Journal of Statistics-Revue Canadienne De Statistique","volume":"52 2","pages":"618-635"},"PeriodicalIF":1.0000,"publicationDate":"2023-08-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/cjs.11789","citationCount":"0","resultStr":"{\"title\":\"High-dimensional model averaging for quantile regression\",\"authors\":\"Jinhan Xie, Xianwen Ding, Bei Jiang, Xiaodong Yan, Linglong Kong\",\"doi\":\"10.1002/cjs.11789\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This article considers robust prediction issues in ultrahigh-dimensional (UHD) datasets and proposes combining quantile regression with sequential model averaging to arrive at a quantile sequential model averaging (QSMA) procedure. The QSMA method is made computationally feasible by employing a sequential screening process and a Bayesian information criterion (BIC) model averaging method for UHD quantile regression and provides a more accurate and stable prediction of the conditional quantile of a response variable. Meanwhile, the proposed method shows effective behaviour in dealing with prediction in UHD datasets and saves a great deal of computational cost with the help of the sequential technique. Under some suitable conditions, we show that the proposed QSMA method can mitigate overfitting and yields reliable predictions. Numerical studies, including extensive simulations and a real data example, are presented to confirm that the proposed method performs well.</p>\",\"PeriodicalId\":55281,\"journal\":{\"name\":\"Canadian Journal of Statistics-Revue Canadienne De Statistique\",\"volume\":\"52 2\",\"pages\":\"618-635\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-08-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/cjs.11789\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Canadian Journal of Statistics-Revue Canadienne De Statistique\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/cjs.11789\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Canadian Journal of Statistics-Revue Canadienne De Statistique","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/cjs.11789","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

High-dimensional model averaging for quantile regression

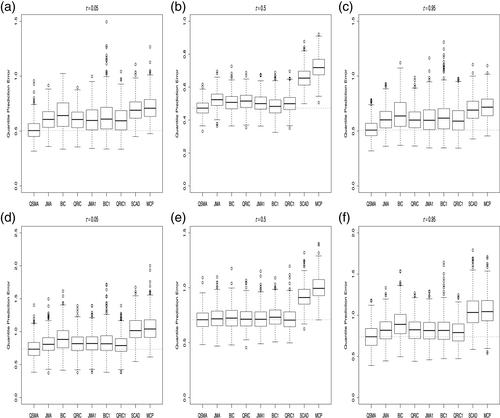

This article considers robust prediction issues in ultrahigh-dimensional (UHD) datasets and proposes combining quantile regression with sequential model averaging to arrive at a quantile sequential model averaging (QSMA) procedure. The QSMA method is made computationally feasible by employing a sequential screening process and a Bayesian information criterion (BIC) model averaging method for UHD quantile regression and provides a more accurate and stable prediction of the conditional quantile of a response variable. Meanwhile, the proposed method shows effective behaviour in dealing with prediction in UHD datasets and saves a great deal of computational cost with the help of the sequential technique. Under some suitable conditions, we show that the proposed QSMA method can mitigate overfitting and yields reliable predictions. Numerical studies, including extensive simulations and a real data example, are presented to confirm that the proposed method performs well.

期刊介绍:

The Canadian Journal of Statistics is the official journal of the Statistical Society of Canada. It has a reputation internationally as an excellent journal. The editorial board is comprised of statistical scientists with applied, computational, methodological, theoretical and probabilistic interests. Their role is to ensure that the journal continues to provide an international forum for the discipline of Statistics.

The journal seeks papers making broad points of interest to many readers, whereas papers making important points of more specific interest are better placed in more specialized journals. The levels of innovation and impact are key in the evaluation of submitted manuscripts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: