{"title":"媒体报道、实际盈余管理和长期市场表现:来自中国IPO的证据","authors":"Danning Yu","doi":"10.1007/s10690-022-09396-2","DOIUrl":null,"url":null,"abstract":"<div><p>This study investigates how real earnings management (REM) in the initial public offering (IPO) year affects long-run post-IPO market performance. The empirical results show that the effect of REM on a firm’s stock returns varies with the forms of REM. Abnormal production costs are positively associated with long-run returns, whereas abnormal cuts in discretionary expenses are negatively associated with long-run returns. These results suggest that investors are not fully aware of the implications of REM and initially undervalue or overvalue the firm based on different REM activities. Further, this study examines the long-run role of the media in the capital market by examining the impact of media coverage on the consequences of IPO firms’ REM practices. The results indicate that the associations between REM and stock returns become weaker if the IPO firm is more visible through the media. Additional analyses show that retail investors are more likely to initially misprice REM activities and be influenced by media information. Compared with media coverage, audit quality or analyst following has a relatively less pronounced effect on the consequences of REM activities. These findings imply that media coverage appears to mitigate the influence of REM on stock returns, facilitating market efficiency after a firm’s IPO in the long run.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"30 4","pages":"729 - 760"},"PeriodicalIF":2.6000,"publicationDate":"2023-01-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"1","resultStr":"{\"title\":\"Media Coverage, Real Earnings Management, and Long-Run Market Performance: Evidence from Chinese IPOs\",\"authors\":\"Danning Yu\",\"doi\":\"10.1007/s10690-022-09396-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study investigates how real earnings management (REM) in the initial public offering (IPO) year affects long-run post-IPO market performance. The empirical results show that the effect of REM on a firm’s stock returns varies with the forms of REM. Abnormal production costs are positively associated with long-run returns, whereas abnormal cuts in discretionary expenses are negatively associated with long-run returns. These results suggest that investors are not fully aware of the implications of REM and initially undervalue or overvalue the firm based on different REM activities. Further, this study examines the long-run role of the media in the capital market by examining the impact of media coverage on the consequences of IPO firms’ REM practices. The results indicate that the associations between REM and stock returns become weaker if the IPO firm is more visible through the media. Additional analyses show that retail investors are more likely to initially misprice REM activities and be influenced by media information. Compared with media coverage, audit quality or analyst following has a relatively less pronounced effect on the consequences of REM activities. These findings imply that media coverage appears to mitigate the influence of REM on stock returns, facilitating market efficiency after a firm’s IPO in the long run.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"30 4\",\"pages\":\"729 - 760\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-01-14\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-022-09396-2\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-022-09396-2","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Media Coverage, Real Earnings Management, and Long-Run Market Performance: Evidence from Chinese IPOs

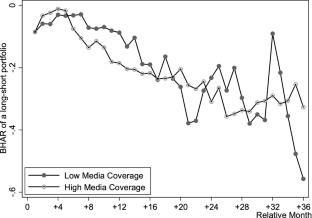

This study investigates how real earnings management (REM) in the initial public offering (IPO) year affects long-run post-IPO market performance. The empirical results show that the effect of REM on a firm’s stock returns varies with the forms of REM. Abnormal production costs are positively associated with long-run returns, whereas abnormal cuts in discretionary expenses are negatively associated with long-run returns. These results suggest that investors are not fully aware of the implications of REM and initially undervalue or overvalue the firm based on different REM activities. Further, this study examines the long-run role of the media in the capital market by examining the impact of media coverage on the consequences of IPO firms’ REM practices. The results indicate that the associations between REM and stock returns become weaker if the IPO firm is more visible through the media. Additional analyses show that retail investors are more likely to initially misprice REM activities and be influenced by media information. Compared with media coverage, audit quality or analyst following has a relatively less pronounced effect on the consequences of REM activities. These findings imply that media coverage appears to mitigate the influence of REM on stock returns, facilitating market efficiency after a firm’s IPO in the long run.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: