{"title":"可再生能源价格:稳健性分析*","authors":"Manuel Landajo, María José Presno","doi":"10.1111/1467-8489.12468","DOIUrl":null,"url":null,"abstract":"<p>This paper addresses the problem of testing for persistence in the effects of the shocks affecting the prices of renewable commodities, which have potential implications on stabilisation policies and economic forecasting, among other areas. A robust methodology is employed that enables the determination of the potential presence and number of instant/gradual structural changes in the series, stationarity testing conditional on the number of changes detected and the detection of change points. This procedure is applied to the annual real prices of eighteen renewable commodities over the period of 1900–2018. Results indicate that most of the series display non-linear features, including quadratic patterns and regime transitions that often coincide with well-known political and economic episodes. The conclusions of stationarity testing suggest that roughly half of the series are integrated. Stationarity fails to be rejected for grains, whereas most livestock and textile commodities do reject stationarity. Evidence is mixed in all soft commodities and tropical crops, where stationarity can be rejected in approximately half of the cases. The implication would be that for these commodities, stabilisation schemes would not be recommended.</p>","PeriodicalId":55427,"journal":{"name":"Australian Journal of Agricultural and Resource Economics","volume":"66 2","pages":"447-470"},"PeriodicalIF":2.6000,"publicationDate":"2022-03-07","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8489.12468","citationCount":"1","resultStr":"{\"title\":\"The prices of renewable commodities: a robust stationarity analysis*\",\"authors\":\"Manuel Landajo, María José Presno\",\"doi\":\"10.1111/1467-8489.12468\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>This paper addresses the problem of testing for persistence in the effects of the shocks affecting the prices of renewable commodities, which have potential implications on stabilisation policies and economic forecasting, among other areas. A robust methodology is employed that enables the determination of the potential presence and number of instant/gradual structural changes in the series, stationarity testing conditional on the number of changes detected and the detection of change points. This procedure is applied to the annual real prices of eighteen renewable commodities over the period of 1900–2018. Results indicate that most of the series display non-linear features, including quadratic patterns and regime transitions that often coincide with well-known political and economic episodes. The conclusions of stationarity testing suggest that roughly half of the series are integrated. Stationarity fails to be rejected for grains, whereas most livestock and textile commodities do reject stationarity. Evidence is mixed in all soft commodities and tropical crops, where stationarity can be rejected in approximately half of the cases. The implication would be that for these commodities, stabilisation schemes would not be recommended.</p>\",\"PeriodicalId\":55427,\"journal\":{\"name\":\"Australian Journal of Agricultural and Resource Economics\",\"volume\":\"66 2\",\"pages\":\"447-470\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2022-03-07\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/1467-8489.12468\",\"citationCount\":\"1\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Australian Journal of Agricultural and Resource Economics\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/1467-8489.12468\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"AGRICULTURAL ECONOMICS & POLICY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Australian Journal of Agricultural and Resource Economics","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/1467-8489.12468","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"AGRICULTURAL ECONOMICS & POLICY","Score":null,"Total":0}

The prices of renewable commodities: a robust stationarity analysis*

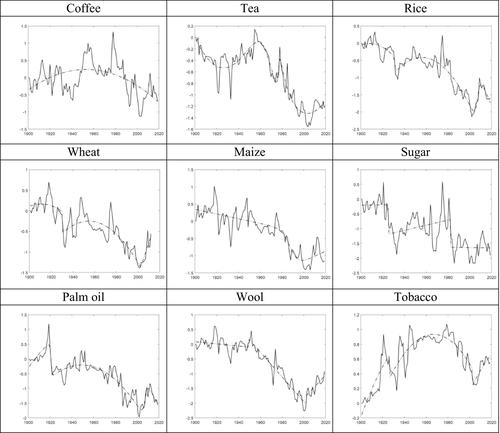

This paper addresses the problem of testing for persistence in the effects of the shocks affecting the prices of renewable commodities, which have potential implications on stabilisation policies and economic forecasting, among other areas. A robust methodology is employed that enables the determination of the potential presence and number of instant/gradual structural changes in the series, stationarity testing conditional on the number of changes detected and the detection of change points. This procedure is applied to the annual real prices of eighteen renewable commodities over the period of 1900–2018. Results indicate that most of the series display non-linear features, including quadratic patterns and regime transitions that often coincide with well-known political and economic episodes. The conclusions of stationarity testing suggest that roughly half of the series are integrated. Stationarity fails to be rejected for grains, whereas most livestock and textile commodities do reject stationarity. Evidence is mixed in all soft commodities and tropical crops, where stationarity can be rejected in approximately half of the cases. The implication would be that for these commodities, stabilisation schemes would not be recommended.

期刊介绍:

The Australian Journal of Agricultural and Resource Economics (AJARE) provides a forum for innovative and scholarly work in agricultural and resource economics. First published in 1997, the Journal succeeds the Australian Journal of Agricultural Economics and the Review of Marketing and Agricultural Economics, upholding the tradition of these long-established journals.

Accordingly, the editors are guided by the following objectives:

-To maintain a high standard of analytical rigour offering sufficient variety of content so as to appeal to a broad spectrum of both academic and professional economists and policymakers.

-In maintaining the tradition of its predecessor journals, to combine articles with policy reviews and surveys of key analytical issues in agricultural and resource economics.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: