一种利用新闻量和情绪进行投资组合选择的新方法

IF 2.6

4区 经济学

Q2 BUSINESS, FINANCE

引用次数: 0

摘要

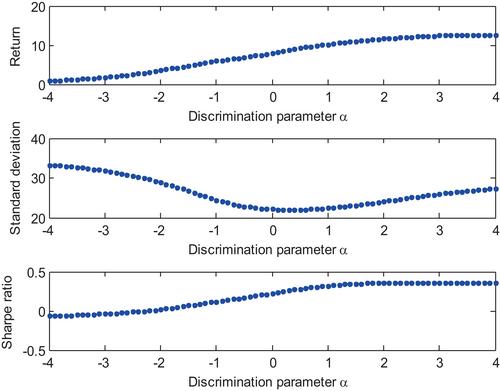

在本研究中,我们开发了一种新颖的方法,通过将新闻量和情绪信息与k近邻(kNN)算法相结合来实现投资组合多样化。实证分析表明,高新闻量增加了投资组合风险,而新闻情绪增加了投资组合收益。基于这些发现,我们提出了一种kNN算法用于投资组合选择。我们的样本内和样本外测试表明,所提出的kNN投资组合选择方法优于基准指数投资组合。总体而言,我们表明将新闻量和情绪纳入投资组合选择可以通过提高回报和降低风险来提高投资组合绩效。本文章由计算机程序翻译,如有差异,请以英文原文为准。

A novel approach to portfolio selection using news volume and sentiment

In this study, we develop a novel approach to portfolio diversification by integrating information on news volume and sentiment with the k-nearest neighbors (kNN) algorithm. Our empirical analysis indicates that high news volume contributes to portfolio risk, whereas news sentiment contributes to portfolio return. Based on these findings, we propose a kNN algorithm for portfolio selection. Our in-sample and out-of-sample tests suggest that the proposed kNN portfolio selection approach outperforms the benchmark index portfolio. Overall, we show that incorporating news volume and sentiment into portfolio selection can enhance portfolio performance by improving returns and reducing risk.

求助全文

通过发布文献求助,成功后即可免费获取论文全文。

去求助

来源期刊

International Review of Finance

BUSINESS, FINANCE-

CiteScore

3.30

自引率

5.90%

发文量

28

期刊介绍:

The International Review of Finance (IRF) publishes high-quality research on all aspects of financial economics, including traditional areas such as asset pricing, corporate finance, market microstructure, financial intermediation and regulation, financial econometrics, financial engineering and risk management, as well as new areas such as markets and institutions of emerging market economies, especially those in the Asia-Pacific region. In addition, the Letters Section in IRF is a premium outlet of letter-length research in all fields of finance. The length of the articles in the Letters Section is limited to a maximum of eight journal pages.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: