{"title":"加入标准普尔500指数后收益为负,删除后收益为正?标准普尔500指数与标准普尔400指数吸引力的新证据","authors":"Anand M. Vijh, Jiawei (Brooke) Wang","doi":"10.1111/fima.12391","DOIUrl":null,"url":null,"abstract":"<p>In recent years, the majority of additions to and deletions from the S&P 500 index have been stocks that were previously or subsequently included in the S&P 400 index. The announcement returns of these changes have been the opposite of what has been documented for all S&P 500 additions and deletions in an extensive literature. During 2016–2020, such “upward additions” to the S&P 500 index resulted in an average announcement excess return of –2.48% over a 3-day period, while “downward deletions” to the S&P 400 index resulted in an excess return of +1.37%. We explain these new results by the increasing total institutional ownership of S&P 400 stocks. Our results thus show the increasing benefits of being included in the mid-cap S&P 400 index relative to being included in the large-cap S&P 500 index.</p>","PeriodicalId":48123,"journal":{"name":"Financial Management","volume":"51 4","pages":"1127-1164"},"PeriodicalIF":2.9000,"publicationDate":"2022-02-24","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fima.12391","citationCount":"0","resultStr":"{\"title\":\"Negative returns on addition to the S&P 500 index and positive returns on deletion? New evidence on the attractiveness of S&P 500 versus S&P 400 indexes\",\"authors\":\"Anand M. Vijh, Jiawei (Brooke) Wang\",\"doi\":\"10.1111/fima.12391\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>In recent years, the majority of additions to and deletions from the S&P 500 index have been stocks that were previously or subsequently included in the S&P 400 index. The announcement returns of these changes have been the opposite of what has been documented for all S&P 500 additions and deletions in an extensive literature. During 2016–2020, such “upward additions” to the S&P 500 index resulted in an average announcement excess return of –2.48% over a 3-day period, while “downward deletions” to the S&P 400 index resulted in an excess return of +1.37%. We explain these new results by the increasing total institutional ownership of S&P 400 stocks. Our results thus show the increasing benefits of being included in the mid-cap S&P 400 index relative to being included in the large-cap S&P 500 index.</p>\",\"PeriodicalId\":48123,\"journal\":{\"name\":\"Financial Management\",\"volume\":\"51 4\",\"pages\":\"1127-1164\"},\"PeriodicalIF\":2.9000,\"publicationDate\":\"2022-02-24\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1111/fima.12391\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Financial Management\",\"FirstCategoryId\":\"96\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1111/fima.12391\",\"RegionNum\":3,\"RegionCategory\":\"经济学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"BUSINESS, FINANCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Financial Management","FirstCategoryId":"96","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1111/fima.12391","RegionNum":3,"RegionCategory":"经济学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"BUSINESS, FINANCE","Score":null,"Total":0}

Negative returns on addition to the S&P 500 index and positive returns on deletion? New evidence on the attractiveness of S&P 500 versus S&P 400 indexes

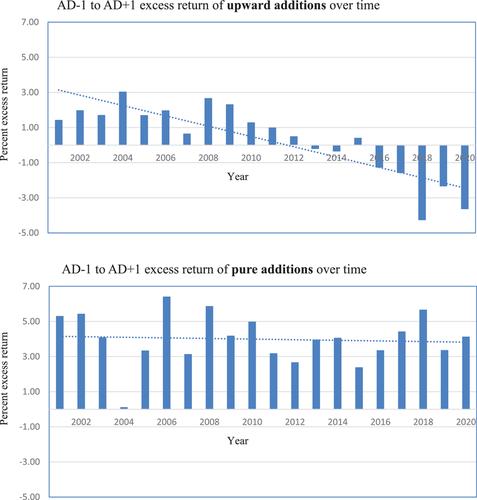

In recent years, the majority of additions to and deletions from the S&P 500 index have been stocks that were previously or subsequently included in the S&P 400 index. The announcement returns of these changes have been the opposite of what has been documented for all S&P 500 additions and deletions in an extensive literature. During 2016–2020, such “upward additions” to the S&P 500 index resulted in an average announcement excess return of –2.48% over a 3-day period, while “downward deletions” to the S&P 400 index resulted in an excess return of +1.37%. We explain these new results by the increasing total institutional ownership of S&P 400 stocks. Our results thus show the increasing benefits of being included in the mid-cap S&P 400 index relative to being included in the large-cap S&P 500 index.

期刊介绍:

Financial Management (FM) serves both academics and practitioners concerned with the financial management of nonfinancial businesses, financial institutions, and public or private not-for-profit organizations.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: