{"title":"台湾期货市场交易时段收益率波动预测:跳变方法的周期性制度转换","authors":"Yi-Hao Lai, Yi-Chiuan Wang, Yu-Ching Chang","doi":"10.1007/s10690-023-09415-w","DOIUrl":null,"url":null,"abstract":"<div><p>This study develops a novel periodic regime-switching model (the PRS model) to improve the forecasting of stock market volatility by accounting for the information from non-trading and trading periods, including regular trading and after-hour trading. Empirical analysis of the Taiwan Futures Exchange (TAIFEX) demonstrates the significant improvements of the PRS model in both in-sample and out-of-sample periods. Our results also show that the introduction of after-hour trading sessions has provided valuable information for volatility forecasting in subsequent regular trading sessions, emphasizing the importance of considering diverse information flows across different trading and non-trading times. The PRS model effectively captures the dynamics of non-trading and trading sessions and the influence of unusual news arrivals and jumps on market volatility, contributing to investment and risk management strategies.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"31 2","pages":"285 - 305"},"PeriodicalIF":2.6000,"publicationDate":"2023-09-08","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Forecasting Trading-Session Return Volatility in Taiwan Futures Market: A Periodic Regime Switching with Jump Approach\",\"authors\":\"Yi-Hao Lai, Yi-Chiuan Wang, Yu-Ching Chang\",\"doi\":\"10.1007/s10690-023-09415-w\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study develops a novel periodic regime-switching model (the PRS model) to improve the forecasting of stock market volatility by accounting for the information from non-trading and trading periods, including regular trading and after-hour trading. Empirical analysis of the Taiwan Futures Exchange (TAIFEX) demonstrates the significant improvements of the PRS model in both in-sample and out-of-sample periods. Our results also show that the introduction of after-hour trading sessions has provided valuable information for volatility forecasting in subsequent regular trading sessions, emphasizing the importance of considering diverse information flows across different trading and non-trading times. The PRS model effectively captures the dynamics of non-trading and trading sessions and the influence of unusual news arrivals and jumps on market volatility, contributing to investment and risk management strategies.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"31 2\",\"pages\":\"285 - 305\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-09-08\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-023-09415-w\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09415-w","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Forecasting Trading-Session Return Volatility in Taiwan Futures Market: A Periodic Regime Switching with Jump Approach

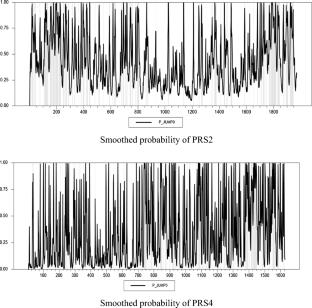

This study develops a novel periodic regime-switching model (the PRS model) to improve the forecasting of stock market volatility by accounting for the information from non-trading and trading periods, including regular trading and after-hour trading. Empirical analysis of the Taiwan Futures Exchange (TAIFEX) demonstrates the significant improvements of the PRS model in both in-sample and out-of-sample periods. Our results also show that the introduction of after-hour trading sessions has provided valuable information for volatility forecasting in subsequent regular trading sessions, emphasizing the importance of considering diverse information flows across different trading and non-trading times. The PRS model effectively captures the dynamics of non-trading and trading sessions and the influence of unusual news arrivals and jumps on market volatility, contributing to investment and risk management strategies.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: