{"title":"基于PDE的股票价格信用风险CEV动力学的贝叶斯推断","authors":"Kensuke Kato, Nobuhiro Nakamura","doi":"10.1007/s10690-023-09420-z","DOIUrl":null,"url":null,"abstract":"<div><p>This study proposes a method to infer the parameters of the constant elasticity of variance (CEV) model from the market values of stock after the extension from the asset process of the Merton model in the structural credit risk model to that of the CEV model. The state space model is used, which consists of an asset process (system equation) and the call option pricing a stock value (observation equation), for the inference. However, it is usually difficult to apply the Markov chain Monte Carlo (MCMC) method to estimate the parameters of the CEV model because the observation equation of the state space model has no analytical formula. Our method solves this parameter estimation problem by applying the MCMC combined with a finite difference method of partial differential equations, where the stock value obtained as a CEV option price is numerically solved. This study estimates the parameters from the real stock values of the US financial institutions as an empirical analysis. Furthermore, we analyze the default probability and measure the credit risk of bank portfolios.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"31 2","pages":"389 - 421"},"PeriodicalIF":2.6000,"publicationDate":"2023-08-25","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"PDE-Based Bayesian Inference of CEV Dynamics for Credit Risk in Stock Prices\",\"authors\":\"Kensuke Kato, Nobuhiro Nakamura\",\"doi\":\"10.1007/s10690-023-09420-z\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>This study proposes a method to infer the parameters of the constant elasticity of variance (CEV) model from the market values of stock after the extension from the asset process of the Merton model in the structural credit risk model to that of the CEV model. The state space model is used, which consists of an asset process (system equation) and the call option pricing a stock value (observation equation), for the inference. However, it is usually difficult to apply the Markov chain Monte Carlo (MCMC) method to estimate the parameters of the CEV model because the observation equation of the state space model has no analytical formula. Our method solves this parameter estimation problem by applying the MCMC combined with a finite difference method of partial differential equations, where the stock value obtained as a CEV option price is numerically solved. This study estimates the parameters from the real stock values of the US financial institutions as an empirical analysis. Furthermore, we analyze the default probability and measure the credit risk of bank portfolios.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"31 2\",\"pages\":\"389 - 421\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-08-25\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-023-09420-z\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09420-z","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

PDE-Based Bayesian Inference of CEV Dynamics for Credit Risk in Stock Prices

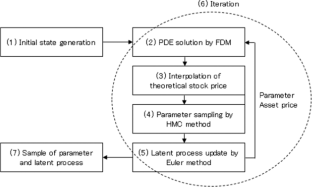

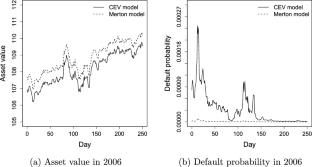

This study proposes a method to infer the parameters of the constant elasticity of variance (CEV) model from the market values of stock after the extension from the asset process of the Merton model in the structural credit risk model to that of the CEV model. The state space model is used, which consists of an asset process (system equation) and the call option pricing a stock value (observation equation), for the inference. However, it is usually difficult to apply the Markov chain Monte Carlo (MCMC) method to estimate the parameters of the CEV model because the observation equation of the state space model has no analytical formula. Our method solves this parameter estimation problem by applying the MCMC combined with a finite difference method of partial differential equations, where the stock value obtained as a CEV option price is numerically solved. This study estimates the parameters from the real stock values of the US financial institutions as an empirical analysis. Furthermore, we analyze the default probability and measure the credit risk of bank portfolios.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: