{"title":"椭圆分布多变量散射和定位的高效高分解估计器","authors":"Justin Fishbone, Lamine Mili","doi":"10.1002/cjs.11770","DOIUrl":null,"url":null,"abstract":"<p>High-breakdown-point estimators of multivariate location and shape matrices, such as the <span></span><math>\n <mrow>\n <mtext>MM</mtext>\n </mrow></math>-<i>estimator</i> with smoothed hard rejection and the Rocke <span></span><math>\n <mrow>\n <mi>S</mi>\n </mrow></math>-estimator, are generally designed to have high efficiency for Gaussian data. However, many phenomena are non-Gaussian, and these estimators can therefore have poor efficiency. This article proposes a new tunable <span></span><math>\n <mrow>\n <mi>S</mi>\n </mrow></math>-estimator, termed the <span></span><math>\n <mrow>\n <msub>\n <mrow>\n <mi>S</mi>\n </mrow>\n <mrow>\n <mi>q</mi>\n </mrow>\n </msub>\n </mrow></math>-estimator, for the general class of symmetric elliptical distributions, a class containing many common families such as the multivariate Gaussian, <span></span><math>\n <mrow>\n <mi>t</mi>\n </mrow></math>-, Cauchy, Laplace, hyperbolic, and normal inverse Gaussian distributions. Across this class, the <span></span><math>\n <mrow>\n <msub>\n <mrow>\n <mi>S</mi>\n </mrow>\n <mrow>\n <mi>q</mi>\n </mrow>\n </msub>\n </mrow></math>-estimator is shown to generally provide higher maximum efficiency than other leading high-breakdown estimators while maintaining the maximum breakdown point. Furthermore, the <span></span><math>\n <mrow>\n <msub>\n <mrow>\n <mi>S</mi>\n </mrow>\n <mrow>\n <mi>q</mi>\n </mrow>\n </msub>\n </mrow></math>-estimator is demonstrated to be distributionally robust, and its robustness to outliers is demonstrated to be on par with these leading estimators while also being more stable with respect to initial conditions. From a practical viewpoint, these properties make the <span></span><math>\n <mrow>\n <msub>\n <mrow>\n <mi>S</mi>\n </mrow>\n <mrow>\n <mi>q</mi>\n </mrow>\n </msub>\n </mrow></math>-estimator broadly applicable for practitioners. These advantages are demonstrated with an example application—the minimum-variance optimal allocation of financial portfolio investments.</p>","PeriodicalId":55281,"journal":{"name":"Canadian Journal of Statistics-Revue Canadienne De Statistique","volume":"52 2","pages":"437-460"},"PeriodicalIF":1.0000,"publicationDate":"2023-04-16","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/cjs.11770","citationCount":"0","resultStr":"{\"title\":\"New highly efficient high-breakdown estimator of multivariate scatter and location for elliptical distributions\",\"authors\":\"Justin Fishbone, Lamine Mili\",\"doi\":\"10.1002/cjs.11770\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>High-breakdown-point estimators of multivariate location and shape matrices, such as the <span></span><math>\\n <mrow>\\n <mtext>MM</mtext>\\n </mrow></math>-<i>estimator</i> with smoothed hard rejection and the Rocke <span></span><math>\\n <mrow>\\n <mi>S</mi>\\n </mrow></math>-estimator, are generally designed to have high efficiency for Gaussian data. However, many phenomena are non-Gaussian, and these estimators can therefore have poor efficiency. This article proposes a new tunable <span></span><math>\\n <mrow>\\n <mi>S</mi>\\n </mrow></math>-estimator, termed the <span></span><math>\\n <mrow>\\n <msub>\\n <mrow>\\n <mi>S</mi>\\n </mrow>\\n <mrow>\\n <mi>q</mi>\\n </mrow>\\n </msub>\\n </mrow></math>-estimator, for the general class of symmetric elliptical distributions, a class containing many common families such as the multivariate Gaussian, <span></span><math>\\n <mrow>\\n <mi>t</mi>\\n </mrow></math>-, Cauchy, Laplace, hyperbolic, and normal inverse Gaussian distributions. Across this class, the <span></span><math>\\n <mrow>\\n <msub>\\n <mrow>\\n <mi>S</mi>\\n </mrow>\\n <mrow>\\n <mi>q</mi>\\n </mrow>\\n </msub>\\n </mrow></math>-estimator is shown to generally provide higher maximum efficiency than other leading high-breakdown estimators while maintaining the maximum breakdown point. Furthermore, the <span></span><math>\\n <mrow>\\n <msub>\\n <mrow>\\n <mi>S</mi>\\n </mrow>\\n <mrow>\\n <mi>q</mi>\\n </mrow>\\n </msub>\\n </mrow></math>-estimator is demonstrated to be distributionally robust, and its robustness to outliers is demonstrated to be on par with these leading estimators while also being more stable with respect to initial conditions. From a practical viewpoint, these properties make the <span></span><math>\\n <mrow>\\n <msub>\\n <mrow>\\n <mi>S</mi>\\n </mrow>\\n <mrow>\\n <mi>q</mi>\\n </mrow>\\n </msub>\\n </mrow></math>-estimator broadly applicable for practitioners. These advantages are demonstrated with an example application—the minimum-variance optimal allocation of financial portfolio investments.</p>\",\"PeriodicalId\":55281,\"journal\":{\"name\":\"Canadian Journal of Statistics-Revue Canadienne De Statistique\",\"volume\":\"52 2\",\"pages\":\"437-460\"},\"PeriodicalIF\":1.0000,\"publicationDate\":\"2023-04-16\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/cjs.11770\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Canadian Journal of Statistics-Revue Canadienne De Statistique\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/cjs.11770\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"STATISTICS & PROBABILITY\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Canadian Journal of Statistics-Revue Canadienne De Statistique","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/cjs.11770","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"STATISTICS & PROBABILITY","Score":null,"Total":0}

New highly efficient high-breakdown estimator of multivariate scatter and location for elliptical distributions

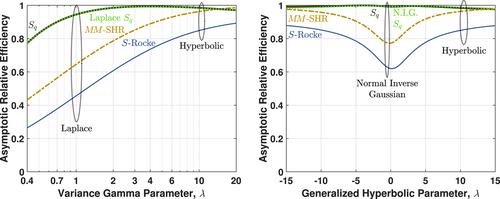

High-breakdown-point estimators of multivariate location and shape matrices, such as the -estimator with smoothed hard rejection and the Rocke -estimator, are generally designed to have high efficiency for Gaussian data. However, many phenomena are non-Gaussian, and these estimators can therefore have poor efficiency. This article proposes a new tunable -estimator, termed the -estimator, for the general class of symmetric elliptical distributions, a class containing many common families such as the multivariate Gaussian, -, Cauchy, Laplace, hyperbolic, and normal inverse Gaussian distributions. Across this class, the -estimator is shown to generally provide higher maximum efficiency than other leading high-breakdown estimators while maintaining the maximum breakdown point. Furthermore, the -estimator is demonstrated to be distributionally robust, and its robustness to outliers is demonstrated to be on par with these leading estimators while also being more stable with respect to initial conditions. From a practical viewpoint, these properties make the -estimator broadly applicable for practitioners. These advantages are demonstrated with an example application—the minimum-variance optimal allocation of financial portfolio investments.

期刊介绍:

The Canadian Journal of Statistics is the official journal of the Statistical Society of Canada. It has a reputation internationally as an excellent journal. The editorial board is comprised of statistical scientists with applied, computational, methodological, theoretical and probabilistic interests. Their role is to ensure that the journal continues to provide an international forum for the discipline of Statistics.

The journal seeks papers making broad points of interest to many readers, whereas papers making important points of more specific interest are better placed in more specialized journals. The levels of innovation and impact are key in the evaluation of submitted manuscripts.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: