Luca Di Persio, D. Mancinelli, Immacolata Oliva, K. Wallbaum

{"title":"结构化产品的时不变投资组合策略,保证最小的股权敞口","authors":"Luca Di Persio, D. Mancinelli, Immacolata Oliva, K. Wallbaum","doi":"10.1002/asmb.2805","DOIUrl":null,"url":null,"abstract":"<p>We introduce a new exotic option to be used within structured products to address a key disadvantage of standard time-invariant portfolio protection: the well-known <i>cash-lock risk.</i> Our approach suggests enriching the framework by including a threshold in the allocation mechanism so that a guaranteed minimum equity exposure (GMEE) is ensured at any point in time. To be able to offer such a solution still with hard capital protection, we apply an option-based structure with a dynamic allocation logic as underlying. We provide an in-depth analysis of the prices of such new exotic options, assuming a Heston–Vasicek-type financial market model, and compare our results with other options used within structured products. Our approach represents an interesting alternative for investors aiming at downsizing protection via time-invariant portfolio protection strategies, meanwhile being also afraid to experience a cash-lock event triggered by market turmoils.</p>","PeriodicalId":55495,"journal":{"name":"Applied Stochastic Models in Business and Industry","volume":null,"pages":null},"PeriodicalIF":1.3000,"publicationDate":"2023-07-30","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2805","citationCount":"0","resultStr":"{\"title\":\"Time-invariant portfolio strategies in structured products with guaranteed minimum equity exposure\",\"authors\":\"Luca Di Persio, D. Mancinelli, Immacolata Oliva, K. Wallbaum\",\"doi\":\"10.1002/asmb.2805\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<p>We introduce a new exotic option to be used within structured products to address a key disadvantage of standard time-invariant portfolio protection: the well-known <i>cash-lock risk.</i> Our approach suggests enriching the framework by including a threshold in the allocation mechanism so that a guaranteed minimum equity exposure (GMEE) is ensured at any point in time. To be able to offer such a solution still with hard capital protection, we apply an option-based structure with a dynamic allocation logic as underlying. We provide an in-depth analysis of the prices of such new exotic options, assuming a Heston–Vasicek-type financial market model, and compare our results with other options used within structured products. Our approach represents an interesting alternative for investors aiming at downsizing protection via time-invariant portfolio protection strategies, meanwhile being also afraid to experience a cash-lock event triggered by market turmoils.</p>\",\"PeriodicalId\":55495,\"journal\":{\"name\":\"Applied Stochastic Models in Business and Industry\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":1.3000,\"publicationDate\":\"2023-07-30\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"https://onlinelibrary.wiley.com/doi/epdf/10.1002/asmb.2805\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Applied Stochastic Models in Business and Industry\",\"FirstCategoryId\":\"100\",\"ListUrlMain\":\"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2805\",\"RegionNum\":4,\"RegionCategory\":\"数学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q3\",\"JCRName\":\"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Applied Stochastic Models in Business and Industry","FirstCategoryId":"100","ListUrlMain":"https://onlinelibrary.wiley.com/doi/10.1002/asmb.2805","RegionNum":4,"RegionCategory":"数学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q3","JCRName":"MATHEMATICS, INTERDISCIPLINARY APPLICATIONS","Score":null,"Total":0}

Time-invariant portfolio strategies in structured products with guaranteed minimum equity exposure

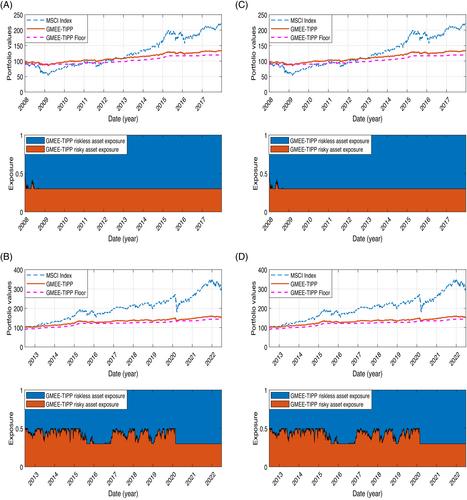

We introduce a new exotic option to be used within structured products to address a key disadvantage of standard time-invariant portfolio protection: the well-known cash-lock risk. Our approach suggests enriching the framework by including a threshold in the allocation mechanism so that a guaranteed minimum equity exposure (GMEE) is ensured at any point in time. To be able to offer such a solution still with hard capital protection, we apply an option-based structure with a dynamic allocation logic as underlying. We provide an in-depth analysis of the prices of such new exotic options, assuming a Heston–Vasicek-type financial market model, and compare our results with other options used within structured products. Our approach represents an interesting alternative for investors aiming at downsizing protection via time-invariant portfolio protection strategies, meanwhile being also afraid to experience a cash-lock event triggered by market turmoils.

期刊介绍:

ASMBI - Applied Stochastic Models in Business and Industry (formerly Applied Stochastic Models and Data Analysis) was first published in 1985, publishing contributions in the interface between stochastic modelling, data analysis and their applications in business, finance, insurance, management and production. In 2007 ASMBI became the official journal of the International Society for Business and Industrial Statistics (www.isbis.org). The main objective is to publish papers, both technical and practical, presenting new results which solve real-life problems or have great potential in doing so. Mathematical rigour, innovative stochastic modelling and sound applications are the key ingredients of papers to be published, after a very selective review process.

The journal is very open to new ideas, like Data Science and Big Data stemming from problems in business and industry or uncertainty quantification in engineering, as well as more traditional ones, like reliability, quality control, design of experiments, managerial processes, supply chains and inventories, insurance, econometrics, financial modelling (provided the papers are related to real problems). The journal is interested also in papers addressing the effects of business and industrial decisions on the environment, healthcare, social life. State-of-the art computational methods are very welcome as well, when combined with sound applications and innovative models.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: