{"title":"基于随机利率模型的多期动态债券投资组合优化","authors":"Yoshiyuki Shimai, Naoki Makimoto","doi":"10.1007/s10690-023-09401-2","DOIUrl":null,"url":null,"abstract":"<div><p>Regardless of the asset class, applying multi-period dynamic portfolio optimization to real investment activity is challenging due to theoretical and structural complexities. In terms of a bond portfolio based on a stochastic interest rate model, some literature exists that focuses on theoretical aspects of multi-period dynamic bond portfolio optimization, such as deriving analytical solutions for optimal portfolios, to be sure, but no empirical studies analyzed the actual bond market. Additionally, a methodology that considers realistic investment constraints has not been developed thus far. In this paper, we propose a new framework for multi-period dynamic bond portfolio optimization. As bond return can be approximated by a linear combination of factors that constitute a stochastic interest rate model, we apply linear rebalancing rules that consider transaction costs, in addition to self-financing and short sales constraints. Then, as an empirical analysis, we conduct an investment backtest by analyzing discount bonds estimated from Japanese interest-bearing government bonds. The results indicate that multi-period optimization represents a relatively high performance compared to single-period optimization. Further, the performance improves as the investment horizon and investment utilization period are extended up to a certain point.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"30 4","pages":"817 - 844"},"PeriodicalIF":2.6000,"publicationDate":"2023-03-23","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Multi-period Dynamic Bond Portfolio Optimization Utilizing a Stochastic Interest Rate Model\",\"authors\":\"Yoshiyuki Shimai, Naoki Makimoto\",\"doi\":\"10.1007/s10690-023-09401-2\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Regardless of the asset class, applying multi-period dynamic portfolio optimization to real investment activity is challenging due to theoretical and structural complexities. In terms of a bond portfolio based on a stochastic interest rate model, some literature exists that focuses on theoretical aspects of multi-period dynamic bond portfolio optimization, such as deriving analytical solutions for optimal portfolios, to be sure, but no empirical studies analyzed the actual bond market. Additionally, a methodology that considers realistic investment constraints has not been developed thus far. In this paper, we propose a new framework for multi-period dynamic bond portfolio optimization. As bond return can be approximated by a linear combination of factors that constitute a stochastic interest rate model, we apply linear rebalancing rules that consider transaction costs, in addition to self-financing and short sales constraints. Then, as an empirical analysis, we conduct an investment backtest by analyzing discount bonds estimated from Japanese interest-bearing government bonds. The results indicate that multi-period optimization represents a relatively high performance compared to single-period optimization. Further, the performance improves as the investment horizon and investment utilization period are extended up to a certain point.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"30 4\",\"pages\":\"817 - 844\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2023-03-23\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-023-09401-2\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-023-09401-2","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Multi-period Dynamic Bond Portfolio Optimization Utilizing a Stochastic Interest Rate Model

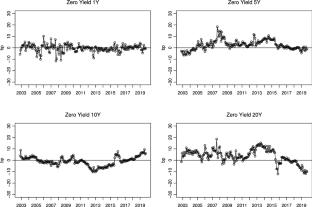

Regardless of the asset class, applying multi-period dynamic portfolio optimization to real investment activity is challenging due to theoretical and structural complexities. In terms of a bond portfolio based on a stochastic interest rate model, some literature exists that focuses on theoretical aspects of multi-period dynamic bond portfolio optimization, such as deriving analytical solutions for optimal portfolios, to be sure, but no empirical studies analyzed the actual bond market. Additionally, a methodology that considers realistic investment constraints has not been developed thus far. In this paper, we propose a new framework for multi-period dynamic bond portfolio optimization. As bond return can be approximated by a linear combination of factors that constitute a stochastic interest rate model, we apply linear rebalancing rules that consider transaction costs, in addition to self-financing and short sales constraints. Then, as an empirical analysis, we conduct an investment backtest by analyzing discount bonds estimated from Japanese interest-bearing government bonds. The results indicate that multi-period optimization represents a relatively high performance compared to single-period optimization. Further, the performance improves as the investment horizon and investment utilization period are extended up to a certain point.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: