{"title":"跨境投资中股票的包含与排除——以股票通为例","authors":"Kin Ming Wong, Kwok Ping Tsang","doi":"10.1007/s10690-022-09395-3","DOIUrl":null,"url":null,"abstract":"<div><p>How does the market react when more or fewer investors are allowed to trade certain stocks? Stock Connect, a cross-border investment channel between mainland China and Hong Kong, provides a natural testing ground. Investors are allowed to trade a list of qualified stocks from the stock market on the other side, and when a stock is removed from the list, investors can only sell but cannot buy that stock. We find that the inclusion of stocks is correlated with abnormal returns, implying downward-sloping demand curves for stocks. The effect weakens over time and disappears in about 40 trading days. There are no abnormal returns when stocks are removed from the list. On the other hand, when investors can only sell some stocks, they have a significantly higher propensity to sell. Their trading style becomes more contrarian for such stocks, and they tend to trade in small amounts. After 6 months, their investment behavior returns to that before the removal.</p></div>","PeriodicalId":54095,"journal":{"name":"Asia-Pacific Financial Markets","volume":"30 4","pages":"701 - 727"},"PeriodicalIF":2.6000,"publicationDate":"2022-11-29","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"0","resultStr":"{\"title\":\"Inclusions and Exclusions of Stocks in Cross-Border Investments: The Case of Stock Connect\",\"authors\":\"Kin Ming Wong, Kwok Ping Tsang\",\"doi\":\"10.1007/s10690-022-09395-3\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>How does the market react when more or fewer investors are allowed to trade certain stocks? Stock Connect, a cross-border investment channel between mainland China and Hong Kong, provides a natural testing ground. Investors are allowed to trade a list of qualified stocks from the stock market on the other side, and when a stock is removed from the list, investors can only sell but cannot buy that stock. We find that the inclusion of stocks is correlated with abnormal returns, implying downward-sloping demand curves for stocks. The effect weakens over time and disappears in about 40 trading days. There are no abnormal returns when stocks are removed from the list. On the other hand, when investors can only sell some stocks, they have a significantly higher propensity to sell. Their trading style becomes more contrarian for such stocks, and they tend to trade in small amounts. After 6 months, their investment behavior returns to that before the removal.</p></div>\",\"PeriodicalId\":54095,\"journal\":{\"name\":\"Asia-Pacific Financial Markets\",\"volume\":\"30 4\",\"pages\":\"701 - 727\"},\"PeriodicalIF\":2.6000,\"publicationDate\":\"2022-11-29\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"0\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Asia-Pacific Financial Markets\",\"FirstCategoryId\":\"1085\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10690-022-09395-3\",\"RegionNum\":0,\"RegionCategory\":null,\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q2\",\"JCRName\":\"ECONOMICS\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Asia-Pacific Financial Markets","FirstCategoryId":"1085","ListUrlMain":"https://link.springer.com/article/10.1007/s10690-022-09395-3","RegionNum":0,"RegionCategory":null,"ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q2","JCRName":"ECONOMICS","Score":null,"Total":0}

Inclusions and Exclusions of Stocks in Cross-Border Investments: The Case of Stock Connect

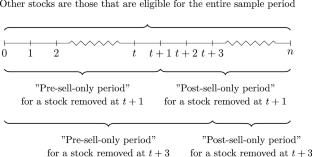

How does the market react when more or fewer investors are allowed to trade certain stocks? Stock Connect, a cross-border investment channel between mainland China and Hong Kong, provides a natural testing ground. Investors are allowed to trade a list of qualified stocks from the stock market on the other side, and when a stock is removed from the list, investors can only sell but cannot buy that stock. We find that the inclusion of stocks is correlated with abnormal returns, implying downward-sloping demand curves for stocks. The effect weakens over time and disappears in about 40 trading days. There are no abnormal returns when stocks are removed from the list. On the other hand, when investors can only sell some stocks, they have a significantly higher propensity to sell. Their trading style becomes more contrarian for such stocks, and they tend to trade in small amounts. After 6 months, their investment behavior returns to that before the removal.

期刊介绍:

The current remarkable growth in the Asia-Pacific financial markets is certain to continue. These markets are expected to play a further important role in the world capital markets for investment and risk management. In accordance with this development, Asia-Pacific Financial Markets (formerly Financial Engineering and the Japanese Markets), the official journal of the Japanese Association of Financial Econometrics and Engineering (JAFEE), is expected to provide an international forum for researchers and practitioners in academia, industry, and government, who engage in empirical and/or theoretical research into the financial markets. We invite submission of quality papers on all aspects of finance and financial engineering.

Here we interpret the term ''financial engineering'' broadly enough to cover such topics as financial time series, portfolio analysis, global asset allocation, trading strategy for investment, optimization methods, macro monetary economic analysis and pricing models for various financial assets including derivatives We stress that purely theoretical papers, as well as empirical studies that use Asia-Pacific market data, are welcome.

Officially cited as: Asia-Pac Financ Markets

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: