{"title":"推荐对等贷款的投资组合,并额外考虑投标期","authors":"Ki Taek Park, Hyejeong Yang, So Young Sohn","doi":"10.1007/s10479-021-04300-z","DOIUrl":null,"url":null,"abstract":"<div><p>Peer-to-peer (P2P) lending has emerged as an alternative method of financing. Keeping pace with this development, many P2P lending studies have provided approaches to select investment portfolios for individual lenders. However, none of these approaches consider how long it takes for an individual loan to be fully funded so as to reduce the opportunity cost incurred due to delayed investment. In this paper, we propose a goal programming framework to develop an optimal P2P lending portfolio that considers not only the expected returns but also this opportunity cost for individual investors. First, for each loan proposal, a logistic regression model is used to predict the loan default probability while a Weibull regression is used to determine the opportunity cost incurred due to the time taken to obtain the loan. Next, goal programming is applied to construct a portfolio that minimizes the slack from the desired return on investment as well as the surplus from the preset opportunity cost due to a prolonged bidding period. The proposed approach is then applied to Prosper platform data and is expected to help investors’ portfolio decisions in the P2P lending market.\n</p></div>","PeriodicalId":8215,"journal":{"name":"Annals of Operations Research","volume":null,"pages":null},"PeriodicalIF":4.4000,"publicationDate":"2021-10-14","publicationTypes":"Journal Article","fieldsOfStudy":null,"isOpenAccess":false,"openAccessPdf":"","citationCount":"2","resultStr":"{\"title\":\"Recommendation of investment portfolio for peer-to-peer lending with additional consideration of bidding period\",\"authors\":\"Ki Taek Park, Hyejeong Yang, So Young Sohn\",\"doi\":\"10.1007/s10479-021-04300-z\",\"DOIUrl\":null,\"url\":null,\"abstract\":\"<div><p>Peer-to-peer (P2P) lending has emerged as an alternative method of financing. Keeping pace with this development, many P2P lending studies have provided approaches to select investment portfolios for individual lenders. However, none of these approaches consider how long it takes for an individual loan to be fully funded so as to reduce the opportunity cost incurred due to delayed investment. In this paper, we propose a goal programming framework to develop an optimal P2P lending portfolio that considers not only the expected returns but also this opportunity cost for individual investors. First, for each loan proposal, a logistic regression model is used to predict the loan default probability while a Weibull regression is used to determine the opportunity cost incurred due to the time taken to obtain the loan. Next, goal programming is applied to construct a portfolio that minimizes the slack from the desired return on investment as well as the surplus from the preset opportunity cost due to a prolonged bidding period. The proposed approach is then applied to Prosper platform data and is expected to help investors’ portfolio decisions in the P2P lending market.\\n</p></div>\",\"PeriodicalId\":8215,\"journal\":{\"name\":\"Annals of Operations Research\",\"volume\":null,\"pages\":null},\"PeriodicalIF\":4.4000,\"publicationDate\":\"2021-10-14\",\"publicationTypes\":\"Journal Article\",\"fieldsOfStudy\":null,\"isOpenAccess\":false,\"openAccessPdf\":\"\",\"citationCount\":\"2\",\"resultStr\":null,\"platform\":\"Semanticscholar\",\"paperid\":null,\"PeriodicalName\":\"Annals of Operations Research\",\"FirstCategoryId\":\"91\",\"ListUrlMain\":\"https://link.springer.com/article/10.1007/s10479-021-04300-z\",\"RegionNum\":3,\"RegionCategory\":\"管理学\",\"ArticlePicture\":[],\"TitleCN\":null,\"AbstractTextCN\":null,\"PMCID\":null,\"EPubDate\":\"\",\"PubModel\":\"\",\"JCR\":\"Q1\",\"JCRName\":\"OPERATIONS RESEARCH & MANAGEMENT SCIENCE\",\"Score\":null,\"Total\":0}","platform":"Semanticscholar","paperid":null,"PeriodicalName":"Annals of Operations Research","FirstCategoryId":"91","ListUrlMain":"https://link.springer.com/article/10.1007/s10479-021-04300-z","RegionNum":3,"RegionCategory":"管理学","ArticlePicture":[],"TitleCN":null,"AbstractTextCN":null,"PMCID":null,"EPubDate":"","PubModel":"","JCR":"Q1","JCRName":"OPERATIONS RESEARCH & MANAGEMENT SCIENCE","Score":null,"Total":0}

Recommendation of investment portfolio for peer-to-peer lending with additional consideration of bidding period

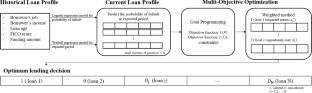

Peer-to-peer (P2P) lending has emerged as an alternative method of financing. Keeping pace with this development, many P2P lending studies have provided approaches to select investment portfolios for individual lenders. However, none of these approaches consider how long it takes for an individual loan to be fully funded so as to reduce the opportunity cost incurred due to delayed investment. In this paper, we propose a goal programming framework to develop an optimal P2P lending portfolio that considers not only the expected returns but also this opportunity cost for individual investors. First, for each loan proposal, a logistic regression model is used to predict the loan default probability while a Weibull regression is used to determine the opportunity cost incurred due to the time taken to obtain the loan. Next, goal programming is applied to construct a portfolio that minimizes the slack from the desired return on investment as well as the surplus from the preset opportunity cost due to a prolonged bidding period. The proposed approach is then applied to Prosper platform data and is expected to help investors’ portfolio decisions in the P2P lending market.

期刊介绍:

The Annals of Operations Research publishes peer-reviewed original articles dealing with key aspects of operations research, including theory, practice, and computation. The journal publishes full-length research articles, short notes, expositions and surveys, reports on computational studies, and case studies that present new and innovative practical applications.

In addition to regular issues, the journal publishes periodic special volumes that focus on defined fields of operations research, ranging from the highly theoretical to the algorithmic and the applied. These volumes have one or more Guest Editors who are responsible for collecting the papers and overseeing the refereeing process.

求助内容:

求助内容: 应助结果提醒方式:

应助结果提醒方式: